CareCloud v2

A very important update

TLDR; This is so short, just read the entire thing!

I contemplated for a short time whether to write about this in a simple note or write a post with updated valuation numbers. I chose the latter since it was little more work since I would have already made the adjusted forecast anyway.

Since my previous write-up on CareCloud, link below:

CareCloud ($CCLD)

TLDR; CareCloud helps doctors and hospitals get paid, run workflows and automate admin. It has built that platform through a significant amount of acquisitions and has been increasing the amount of acquisitions in the past year; often at less than 1x revenue. CareCloud is now trying to turn it into a broader AI-enabled healthcare workflow business. The …

What has changed

Management is trying to remove and has removed a large part of the thesis that kept scaring investors (include me) off. A preferred series (both series A and B), which decreased the amount of cashflow to common shareholders and increases the risk that common shareholders would be diluted. Below I have broken down the three most important recent press releases:

Preferred A is now mostly yesterday’s problem1

The March 2025 Preferred A conversion issued roughly 26 million common shares, taking the share count from about 16 million to about 42 million. Currently (around March 2026), CareCloud said only three substantial Preferred A holders remained, and the stock was still trading around levels seen during the conversion period (last year march). Management has not stated what the current conversion rate is, so I will make the assumption that it is equal to the previous dilution.

Series B is the more important clean-up2

On 14 April, CareCloud announced a US$50 million credit facility with Citizens and Provident and said it would redeem 100% of the outstanding Series B preferred on 15 May 2026. That covers 1,511,372 shares at a total redemption price of US$27.52 per share including accrued dividends. Management said this should remove roughly $3.2 million of annual preferred dividend cash outflow and replace expensive preferred capital with lower-cost institutional debt. In my opinion, management did a great thing here!

Management is now asking for a rerating3

On April 16th management reaffirmed guidance after getting the financing done and framed this as the end of a decade-long balance-sheet repair job. Snyder (CEO) said the company has gone from roughly $23m of revenue and negative EBITDA in late 2015 to about $130m of revenue and roughly $30m of annualised adjusted EBITDA today, therefore reaffirming previous guidance.

Snyder also disclosed that the board rejected an unsolicited 2024 indication of interest at $5.00 per common share because it did not produce the right outcome across the wider shareholder base, including preferred holders.

Whether one agrees with that decision is another question, but the point management is making is obvious. They believe the common share was worth more when there were preferred shares and is worth even more now that the preferred stack is being taken out of the picture.

Valuation

My valuation has changed a bit, completely due to the higher valuation I attribute to the overall business which should be mostly free of preferred shares soon. Previously, I had to carry a slight discount for preferred overhang and possible future dilution risk. Series B is being fully redeemed with non-dilutive bank financing, and management has reaffirmed guidance after closing the facility.

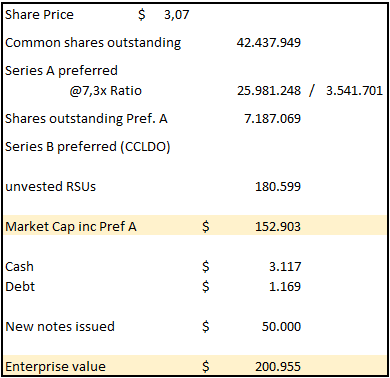

Below the enterprise and market capitalisation estimation can be found:

Cash and debt are retrieved from the latest 10-K and the notes are assumed to be exactly $50m, which is most likely not the case due to transaction costs etc, we just use this as my best estimate.

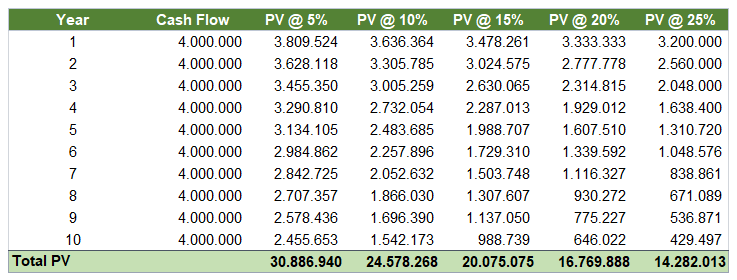

I do not use a DCF, there are to many assumptions that are 3-5 years out where I would simply be dead wrong. I do find it interesting to often show how a change in future cashflow could affect a business I like to value it to the present time. Say the company now saves about $4m a year due to redeeming the preferred compared to the interest they will pay on the $50m, that would result in an increase between 14 to 40m USD.

Above was a simple thought exercise, since the reality is that it is most likely cash flow neutral. Why? Well because the debt carries a similar interest rate as the preferred do. So what does this do? The real benefit of the change in capital structure is that it removes the clearest part of the bear case: dilution risk, preferred dividend leakage (cash outflow), and the constant fear that even if the business performed reasonably well, common shareholders would still not properly see the benefit.

I regularly assume that the market is willing to pay more for a simple business compared to a business with a very intricate capital structure. Hence why you hardly see me write about a story where other people say: “The stock is undervalued because investors are overlooking the fact that this is the real marketcap“.

Keep in mind that I am assuming the following; the old business will decline by low single digit percentage points, as we have seen in the past few years. I do believe their new software or AI solutions will grow at least mid-double digits, which allows the business to grow high single digits!

Game time: “What would you pay for a business growing high single digits“

You could buy a more mature software company or a construction company with excess capacity. Either of these companies should be valued differently due to their cash flow conversion and the moat they have but there is always a fair comparison to make which most people forget.

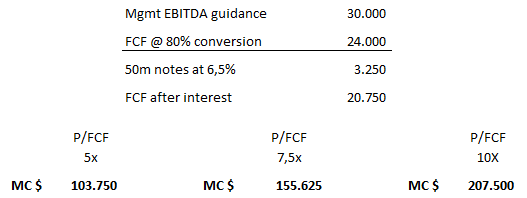

What I would pay is about 5x FCF, I believe it is worth about 10x FCF, this is indeed a higher amount compared to the previous mostly due to the removal of the series A and B which gives me more certainty. If in the future management will split software, AI software and services revenue, this would allow me to make an even better valuation model. For now the simple model below must suffice…

At this point about 80% of EBITDA converts to FCF, assuming no payments to the preferred shares, this will decrease in the future due to the interest payments which will take quite a bit of a bite out of their FCF. Below I have illustrated what current fair value would look like at different multiples.

My current conclusion is that it is approximately fairly valued and would need to fall to about the $2.15 range to pique my interest again. I have a very high hurdle rate but it ensures that I keep disciplined.

I/we have no beneficial long position in the shares of CareCloud ($CCLD). I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.