CareCloud ($CCLD)

From manual services to automated services all for a cheaper price!

TLDR; CareCloud helps doctors and hospitals get paid, run workflows and automate admin. It has built that platform through a significant amount of acquisitions and has been increasing the amount of acquisitions in the past year; often at less than 1x revenue. CareCloud is now trying to turn it into a broader AI-enabled healthcare workflow business. The company is profitable, still acquisitive, and arguably better than the past years, however, the stock is still trading at roughly 8x EV/EBITDA....

What CareCloud is

CareCloud is a healthcare technology and services company that helps providers (mostly hospitals and other health centres) run the administrative side of their company. It supplies software and outsourced services that support documentation, practice operations, patient engagement, billing, coding, claims submission and collections. The tools it provides its customers sit in the core operations of their business: the workflows that determine whether a patient is scheduled, documented correctly, billed correctly and, ultimately, whether the provider gets paid.

Investors are often wrong about CareCloud, and so was I, I hated the company because it outsourced the work and was losing revenue excluding acquisitions. It was and is so easy to misclassify. It is not just a software vendor, and it is not merely a billing outsourcer. It is a hybrid healthcare IT platform with a mixture of software, services and increasingly automation (and of course AI). The company describes itself as:

We are the provider of technology-enabled services and AI-based solutions that redefine the healthcare revenue cycle.

CareCloud has operated within the Revenue Cycle Management (RCM) as its core business for over a decade. Within this RCM, as you can see in the image above, there is a very specific sequence of steps that must be performed before a patient visit gets turned into cash. That includes eligibility checks, claims submission, payment posting, denial management, collections and reporting. Currently, this is done by both software and manual, this is mostly the case for CareCloud their competitors, in the future I expect most of this work will be automated.

CareCloud does not just help providers get paid. It also sits across the wider business within this customer. It operates mainly within their office workflow: scheduling, patient registration, documentation, billing, follow-up and administration. In other words, it is trying to become part of the operating system that runs the entire non-clinical side of healthcare. This area, very similar to an ERP or CRM is incredibly sticky.

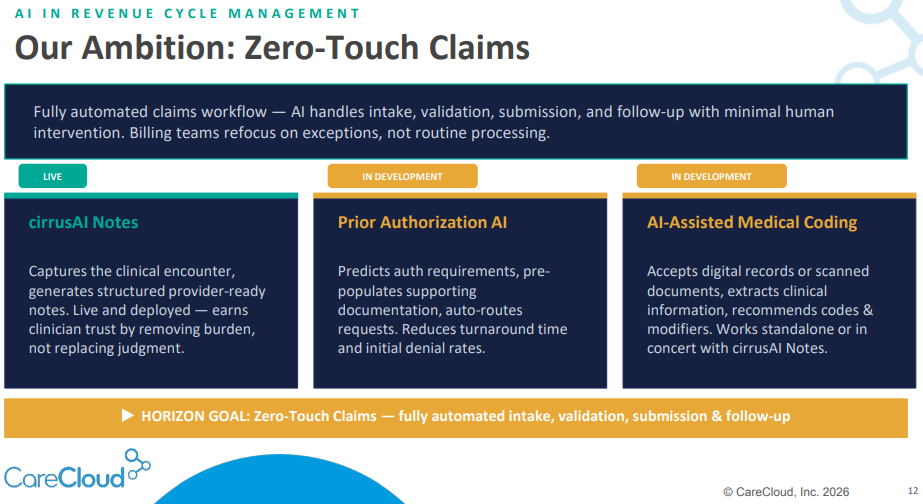

What makes the current CareCloud story different is that management is no longer only pitching software and outsourced services. It is pitching automation layered on top of the workflow they already provide, such service include: documentation, phone handling, coding, prior authorisation and eventually more autonomous claims processing. The ambition is to move from helping providers run the workflow to increasingly automating the same workflow they already provide.

The problem it solves

Healthcare administration is most often structurally inefficient. Healthcare providers face denied claims, time consuming tasks, authorisation bottlenecks, front-office staffing shortages, general staffing shortages, fragmented patient communications, and large documentation burdens (most of which is required by law). Most healthcare organisations operate across outdated systems and rely on manual workarounds. CareCloud’s offering is designed to address those inefficiencies through a combination of workflow software, revenue cycle services, analytics, digital health tools and AI-based automation.

Providers can postpone buying a nicer website or a new analytics tool; they are much less likely to tolerate failure in billing, collections, coding or patient throughput. CareCloud’s relevance comes from being tied to functions that are operationally necessary and economically material. They come in, offer a smooth integration, a product that is most likely priced a bit below what they currently offer or use, but with the promise of higher efficiency and more reliability.

How the business model works

Something important to understand is that CareCloud is not a pure SaaS business. A meaningful portion of revenue comes from technology-enabled service arrangements, such as RCM. This type of revenue is less predictable and revenue is linked to collections performance rather than a fixed subscription fee. Additionally, the company also provides, implementations, consulting and staffing services. All of which are non-recurring in nature but can be if performed well enough.

That hybrid model has both advantages and disadvantages. On the positive side, it tends to make the customer relationship stickier, because CareCloud is embedded in processes that affects revenue collection and the day-to-day operations. On the negative side, for investors it makes revenue forecasting and profitability expectations harder to gauge. Valuation also becomes harder, this might be why this gap between what it is worth and what it is valued exists. Pure SaaS investors may dislike the services exposure, while services investors may undervalue the software and automation optionality.

Products

CareCloud today is broader than the legacy market perception of it. Historically, the company was predominantly an ambulatory healthcare IT and revenue cycle business focused on physician practices and medical groups. Over time it added consulting, staffing, analytics and digital health. The more recent step-change came in 2025, when the Medsphere and MAP App acquisitions extended the business further into inpatient and hospital workflows.

The business can now be thought of in four main buckets.

First, there is revenue cycle management. This includes medical billing, coding, credentialling, eligibility checks, claims clearinghouse functions, denial management and related analytics. This is the core economic engine of the business and the most obviously mission-critical part of the software stack.

Second, there is cloud software. This includes electronic health records, practice management, patient experience tools, business intelligence and customised interfaces. Following the Medsphere acquisition, it also includes hospital-oriented applications such as CareVue, Wellsoft, Marketware, HealthLine and RCM Cloud.

Third, there is digital health. That includes chronic care management, remote patient monitoring and telemedicine. These products are meant to extend CareCloud’s reach within the customer beyond core billing and workflow into adjacent recurring services tied to patient management.

Fourth, there is healthcare IT professional services and staffing. This covers implementations, workflow optimisation, consulting, interim management and workforce augmentation. In other words, the company also monetises the operational complexity that comes with installing, maintaining and improving healthcare systems.

Product markets

Revenue cycle management

RCM ensures the healthcare providers get paid. It includes billing, coding, claims submission, denial management, collections, eligibility checks and related analytics.

The important point, is that RCM is not one homogeneous industry. A large part of the RCM market is fragmented and covered by a large number of small billing firms. A lot of these businesses are small (high relative overhead costs), people-heavy and not profitable. They often compete on price, not on speciality. They heavily rely on labour rather than product, and are vulnerable to churn if they do not deliver collections.

Where CareCloud is trying to differentiate itself, is by combining RCM with software, automation and lower-cost offshore operations.

The RCM space is still a messy place full of subscale operators, and that is one reason why investors often discount companies exposed to it. The recent expansion to the hospital sector is a shift in the right direction, because hospital and inpatient RCM is a more attractive strategic category (read: more money to be made) than small-practice billing.

Cloud software

This is a different market entirely, here the company is selling software that helps providers run practices and clinical workflows: EHR, practice management, patient experience tools, and now selected inpatient hospital applications. This part of the business is more recognisable to software investors because it has recurring revenue, more obvious product differentiation and better operating leverage.

The distinction compared to RCM is simple:

RCM is about executing the admin and claims to get paid.

Cloud software is about running the software within the healthcare system in which that admin and clinical workflow happen.

The hospital additions in 2025 make this segment more interesting. CareVue, Wellsoft, Marketware, HealthLine and RCM Cloud push CareCloud beyond the old software niche into broader hospital workflow and inpatient finance software. That is a bigger and higher margin market.

Digital health

This is the adjacency bucket: chronic care management, remote patient monitoring and telemedicine. These products sit closer to patient engagement and value-based care rather than pure office administration.

Economically, digital health is different again. It is not just workflow software, and it is not just outsourced billing. It is more about helping providers deliver ongoing care and, in some cases, generate reimbursable activity tied to patient monitoring and chronic condition management. That can be attractive because it deepens the relationship with the provider and adds recurring revenue streams outside the core billing workflow.

The challenge is that digital health is also more prone to hype and reimbursement shifts, where a simple CMS change can destroy entire business segments. It can look exciting in presentations, but it hardly ever scale smoothly. I would not be surprised if they stopped operating this business unit or divested this.

Healthcare IT professional services and staffing

This segment covers implementation, workflow optimisation, advisory work, training, interim management and staffing support. In hospital and enterprise settings, these services are often necessary because healthcare organisations struggle to implement systems on their own. Sometimes after implementation the healthcare provider fails to find personnel to fulfil this role and they keep CareCloud on to keep the system running.

This segment is different from the others because it is more labour-intensive and usually lower margin compared to their software segment. That does not mean they should stop it, I would argue the opposite, it is in my opinion very useful. It helps the company get in the door, increases customer dependence, and can support larger software or RCM relationships.

Capital structure

One cannot look at CareCloud properly without acknowledging the capital structure. The preferred stock burden was one of the most obvious reasons the equity looked terrible. It consumed cash, complicated the share count and created a persistent overhang on the common shares.

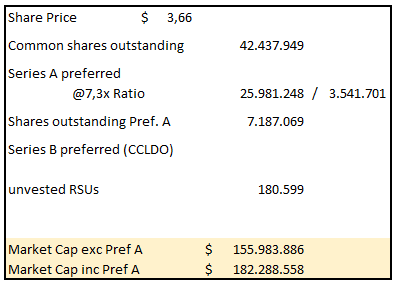

The most important recent event was the March 2025 conversion of most of the Series A preferred into common stock. In total, 3.54 million Series A preferred shares were converted into 25.98 million common shares at 7.3358 common shares per preferred share, including the amount of accumulated unpaid dividends. After that transaction, only 984,530 Series A shares remained outstanding.

Economically, this was both helpful and costly. It improved the company’s cash profile by reducing the preferred drag, but it also dramatically increased the common share count. In other words, the balance sheet became cleaner partly because existing common holders absorbed substantial dilution. That trade-off is central to understanding the stock today. The operating business may be improving, but per-share economics still need to be assessed with care.

My confession

I am going to be very honest, for some reason after this point I did not feel the urge to a very deep dive. Which is quite strange because I am a very curious person personality wise. I like to learn new things, see opportunities in everything, like to get to know new people and what drives them. Like I said, I am curious in nature but the amount of attention on FinTwit (Financial Twitter or X) and the nature of the business simply put me off. It has nothing to do with the company because on a lot of metrics this company does look very cheap, but simply not for me. It did not put me off on valuing the company but on simply looking into the quality of the products or management like I normally do.

I do not believe I can justify an investment in a company I do not even know their product quality or history of so I will not be buying it. I will put it on my watch list based on the valuation I made below but please forgive me if you expected the usual in-depth / quality, there are some amazing companies that I am currently working on.

Below I will continue with why the opportunity exists, the CEO and valuation.

Why does the opportunity exist?

The opportunity exists largely because CareCloud is an awkward business, it has a long acquisition history, a messy capital structure, and a business model that is both based on services and software.

There is also the usual scepticism that comes with acquisition-led businesses. Reported growth can appear healthier than the underlying organic trajectory, particularly when portfolio changes obscure what is happening in the base business. Investors therefore have to work harder to separate genuine operational improvement from the benefits of acquisitions, something which retail investors, including myself, are often not willing to

The same issue applies to the current AI narrative. The logic is credible enough: CareCloud already sits inside administrative and financial workflows that are labour-intensive and well suited to automation. However, parts of that story are still in the scaling phase rather than the monetisation phase. Several of the most interesting products and use cases look promising, but they have not yet fully translated into mature, clearly visible earnings streams. The market is therefore being asked to underwrite future operating leverage that still needs to be proven.

In short, the opportunity exists because the business has become more interesting than its reputation, but not yet simple enough for the market to give it full credit.

Management and the board

Let me be clear, I have not spoken to management. I prefer to always speak to management even if it is only via the e-mail.

Chief Executive Officer

The current CEO is Stephen Snyder, he has been with the company since 2005 and became sole CEO on 1 January 2026, after serving as Co-CEO through 2025. At this point the way CareCloud is heading, is being an AI front runner, highly acquisitive, remain profitable, and at the same time increasing the profitability. This is business simply needs focus and nothing else.

The current strategy is to layer AI into workflows the company already owns, particularly around documentation, phone handling, coding, prior authorisation and revenue cycle. For that to work, management needs to understand the workflow itself and where the touchpoints are and how to commercialise them without disrupting the base business. Snyder’s long history inside the company makes him better suited to understand that.

The same applies to acquisitions. CareCloud is still acquisitive, but the recent deals have been more strategic than the older small billing tuck-ins. Medsphere expanded the company into inpatient and hospital workflows, while MAP App added a hospital benchmarking wedge. The investment case now depends in part on whether these assets can be integrated cleanly and used to widen the platform without damaging profitability.

Most importantly, the company is trying to grow without falling back into the old pattern (unprofitable but and declining core). In 2025 revenue, adjusted EBITDA and cash flow all improved, and management guided to further growth in 2026. I believe he can keep the people within the business disciplined while expanding the product set, why would I think this? He has shown us in the past year he can cut costs or expand team if and when he deems it fit.

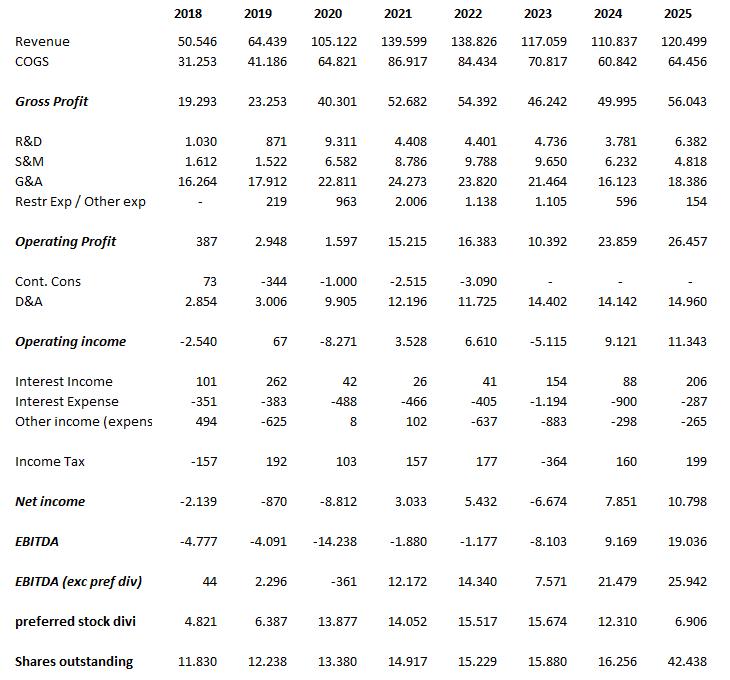

Financials and Forecast

You might be surprised why I came to the conclusion that I did not like the company and I still try to forecast and value it. I keep a list of all stocks I have looked at and I either discard them or put them on the watchlist with a target price, to always keep myself accountable for previous decisions.

This segment will mostly consist of screenshots that I have gathered to support my research. Yes I could use Fiscal.AI for this, however, I do not have a subscription nor do I feel like it helps me understand the company compared to going through each report. Yes one might call me old fashioned.

Above you can see the market capitalisation assuming the series A preferred shares are converted and when they are not converted. I have not done the same for series B since management has expressed no urgency to convert the preferred shares and at the moment rather pay the dividends (Which they also receive themselves due to being partial owners of the preferred B stock).

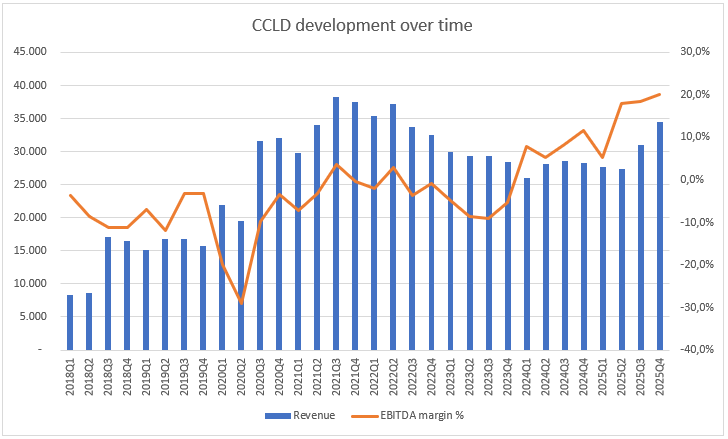

Above you can see the EBITDA margin as a % compared to the total revenue the company has amassed per quarter.

The image above is quite simple and I trust that you can figure it our yourself. ;)

So what has happened? The company has exited the phase where it bought declining businesses and where the core business also declined and has entered the phase of prolonged margin expansion and revenue growth. I believe the now CEO has played a very important role in changing the mindset of both the people working at the company as for the thought behind acquisitions.

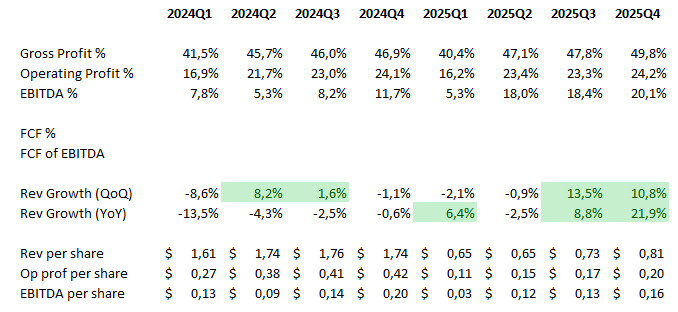

You can also see the devastating effect on the per share Rev / EBITDA the dilution (due to the conversion of the class A prefs) had on shareholders, that is not something anyone wants to see again.

Currently the company is trading at about 8x EV/EBITDA which implies that the EV/FCF is slightly higher due to taxes and interest. You can have two very different opinions here:

This is cheap, if you believe that they will keep growing their revenue at a >10% CAGR for the coming 3 to 5 years (including acquisitions) and will see margin expansion, which the CEO has guided too.

This is fairly priced, organic growth will subside and it will only grow through acquisitions and margin expansion is something that will be more cyclical

I do not believe a lot of people will say or believe this is an expensive stock, I believe people are more likely to say: I find it very hard to understand and forecast the business so this might not be something I would want to invest in.

My assumptions

Organic business will keep declining although slower over time due to better revenue mix; more diverse and sticky products, with more focus on software services.

Margins will increase; however, these will not go to the levels most investors assume, around 25% will be the highest I will confidently assume.

Current preferred structure will remain unchanged, until they will use debt or cash flow to redeem and clear up the structure.

All in all this is not something that is attractive enough to me, I believe with the assumptions above the business is worth 10x EV/EBITDA and maybe 12 to 13 EV/EBITDA if it can acquire businesses consistently and improve the revenue mix. If that is the case I will update yous!

I/we have no beneficial long position in the shares of CareCloud ($CCLD). I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.