We Connect

Update on the annual report 2025; The profits are flowing due

TLDR; The company had great results. Acquisition is being intergrated faster than expected, management has improved the Exertis guidance. All this for a P/E of 6.9 and an EV/EBIT of 4.6!

If this is your first time reading about We.Connect, I would refer you to my first article, it provides a very good initial overview and is still very relevant:

A High-ROIC French distributor hiding in plain sight

Every so often you come across a company that looks almost too good to be true on paper, high returns on capital, steady growth, founder-led, aligned management.

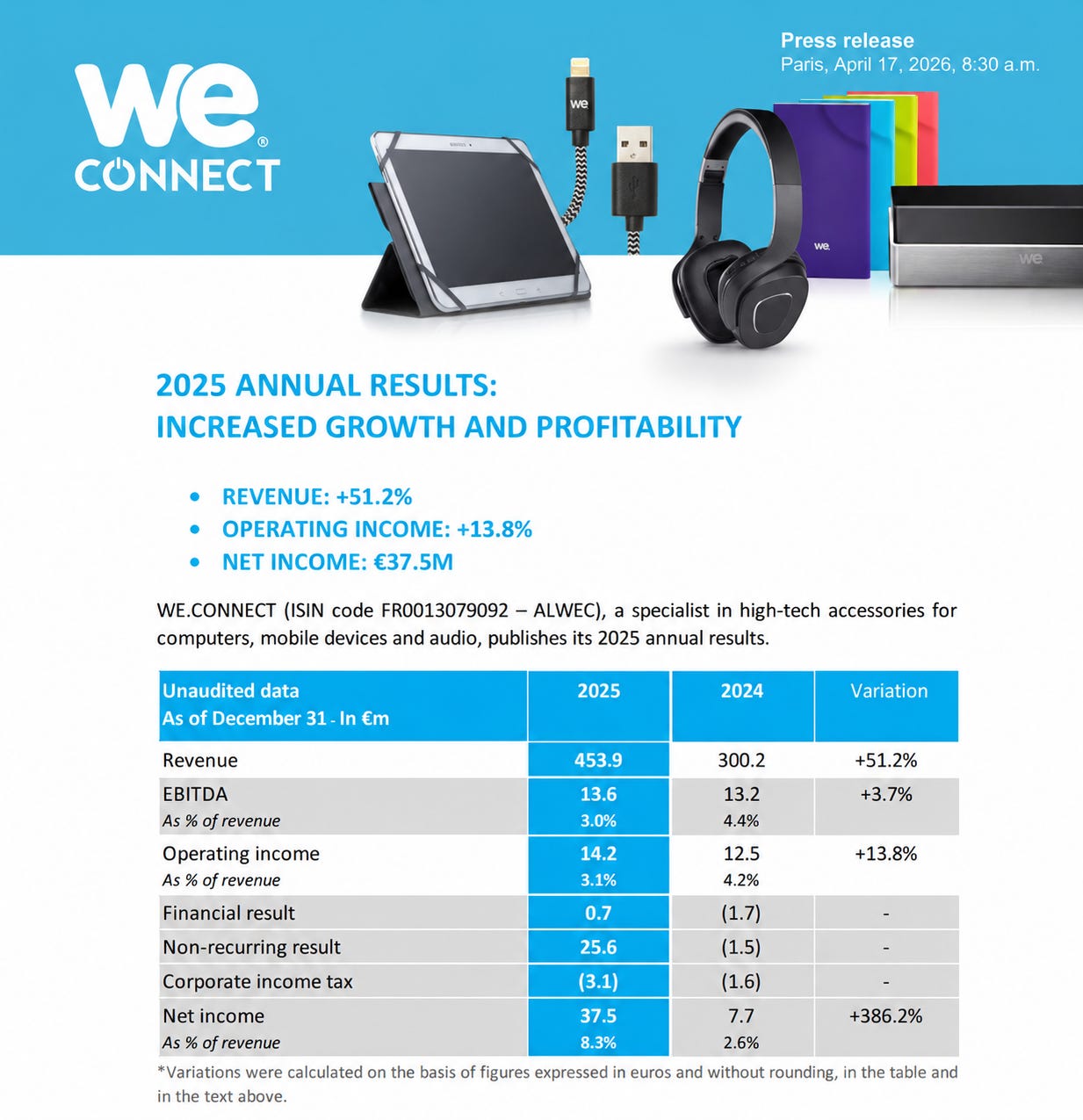

Above you can find the translated press release, which gives a very quick overview of the numbers. In this article I will be discussing the Exertis update management gave and compare it with what I previously expected, the KPIs which I track, and the updated valuation in similar format to last time.

I would love to know if any of you have found management interviews or even a conference call esque information session management has provided. I believe it would offer me great insight outside of the questions management is willing to already answer via e-mail.

Exertis update

In the earnings announcement management has adjusted my expectation for the Exertis acquisition. Previously management guided to a loss in 2026 and slight profitability in 2027 and maybe 2028, in their most recent announcement they adjusted this to a “low loss“ in 2026 and profitability now being likely in 2027.

No further comments or interviews were made on the Exertis acquisition by management.

Balance sheet & P&L changes due to Exertis

An acquisition this size changes certain things in your balance sheet and P&L and this will make the stock screen worse, but it is actually not that bad, for now.

Accounts Receivable (AR) has exploded, this is due tot he acquisition and my best guess is that Exertis has different payment plans in place, this should be smoothed out over the coming year(s) and I see no issue here.

Slightly lower gross margin 9.6%, about 40 bps below the 7 year average, again Exertis has lower margin products and for now I see no reason why this should not return to the mean of ~10%.

EBIT margin declined from 4.2% to 3.1%, this is attributable to both Exertis France (Ezratis) and Exertis Iberia (Iberica), both of the division had a lower margin than We.Connect when acquired. I believe once operated by We.Connect the margins of Exertis should go to ~3.2%, which should push the business margins back to the historic average of about 4%.

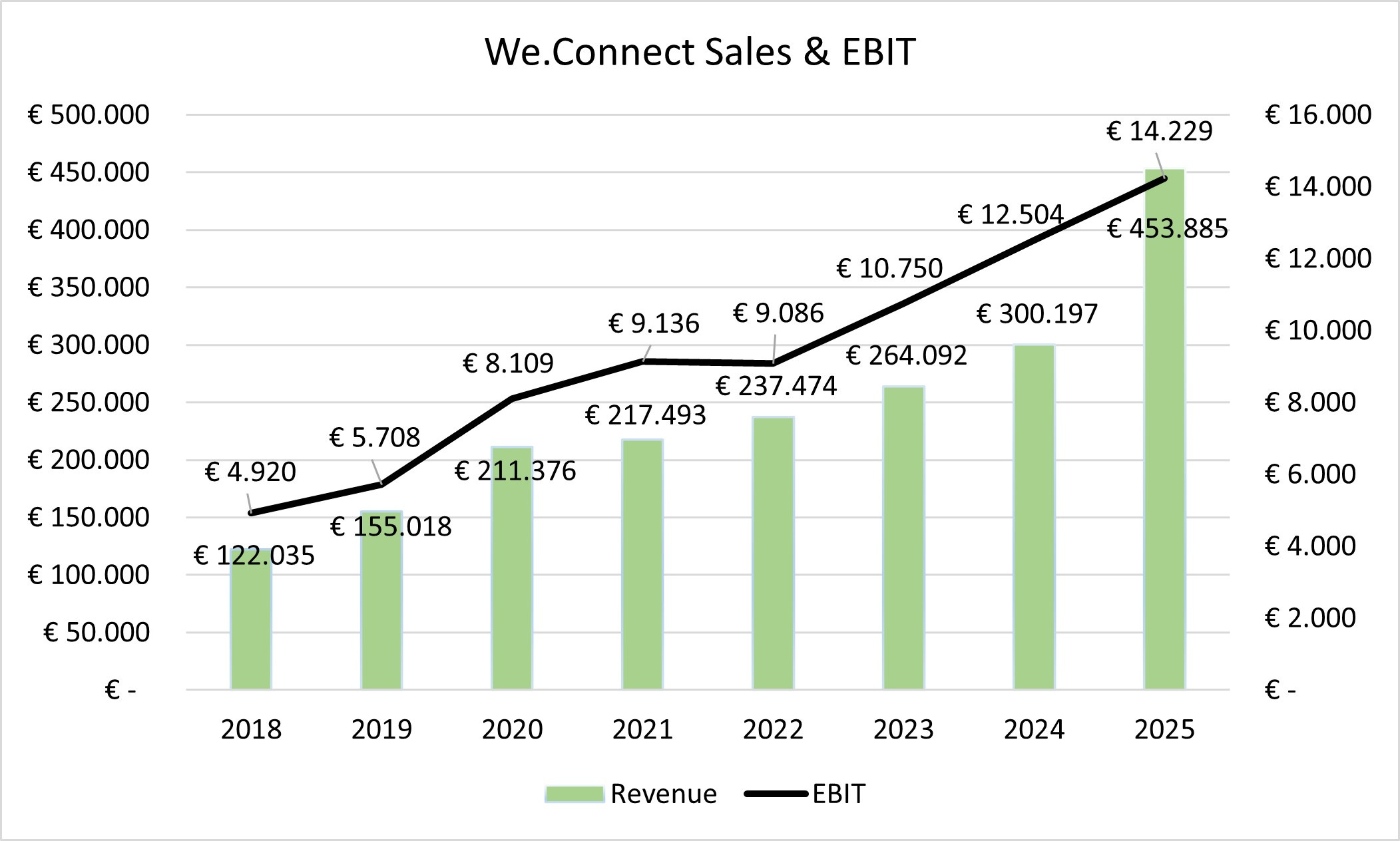

KPIs update

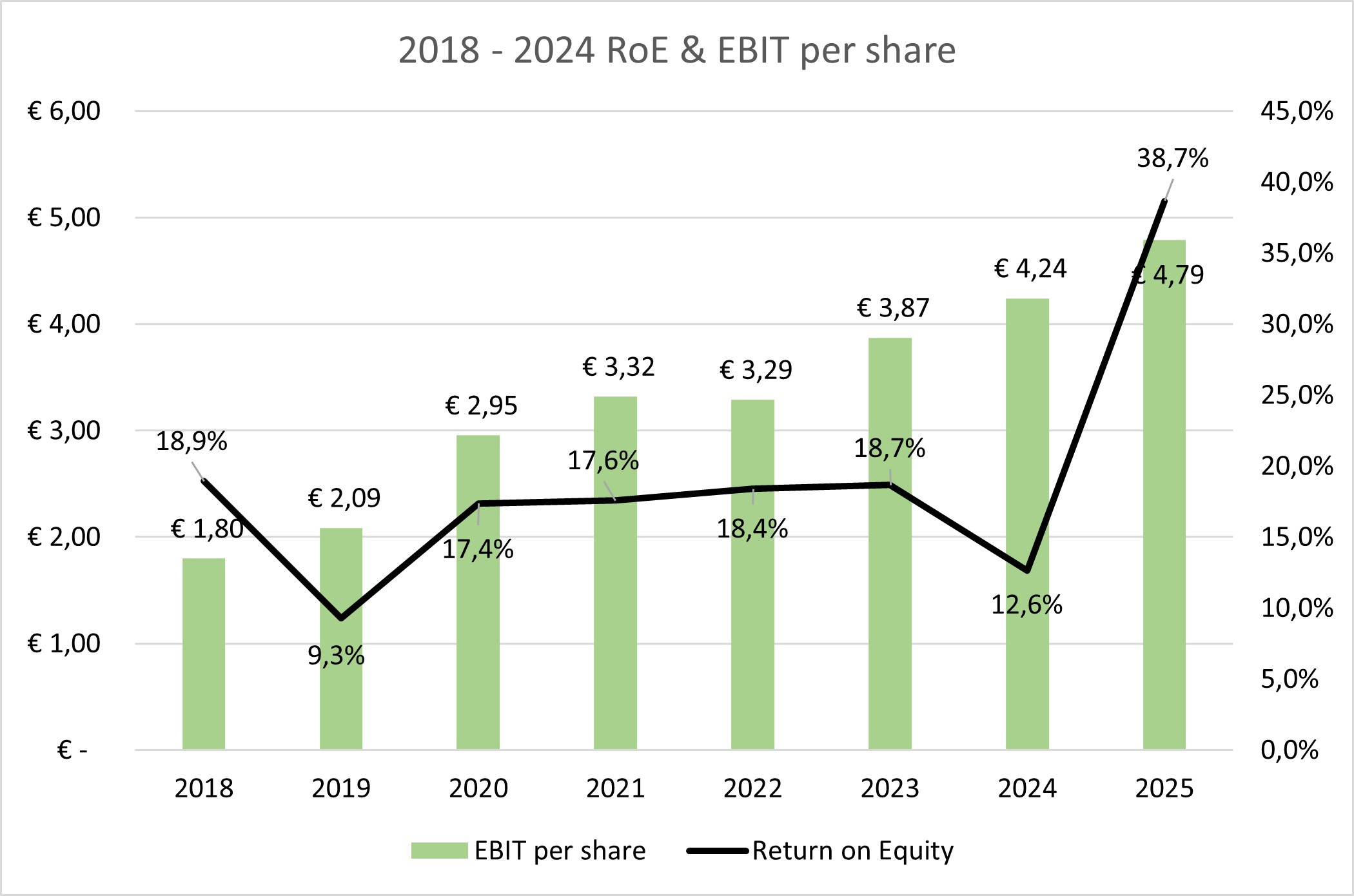

As always I will show my updated KPIs using the FY numbers. As a shareholder I am very happy with the results and the consistency in which the business is run!

As we can see in the graph above the EBIT per share has increased to €4.79, which is just under 13%. We Connect their ROE looks spectacular, but when we dive further into the net income numbers we find out why this is not the case. The company reported €37.5m of net income, which is heavily flattered by bargain purchase accounting.

What happened? Well the Exertis transaction was acquired on exceptional attractive terms. DCC (The seller of Exertis) recapitalised the assets after that was done, Exertis was acquired for €1. Subsequently because the purchase price was so cheap the accounting result was a large negative goodwill gain. Long story short, we should keep in mind that this was a one time benefit of €26.9m, and €10.5m is still on the balance sheet. Adjusting for this benefit the ROE would have been ~10.9%, which was below the historic trend but was expected due to the Exertis acquisition.

Especially since the one time gain from Exertis is not included in EBIT, this makes this specific measure even better. As we can see line go up to the right and that makes me very happy :)

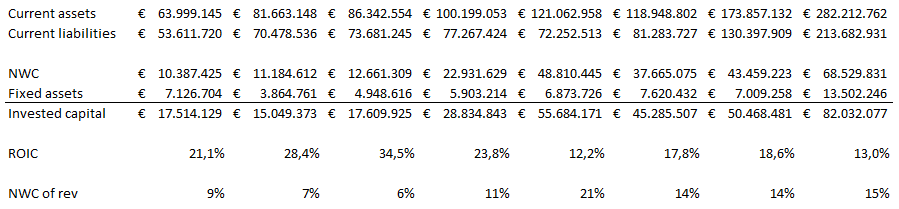

Even with the acquisition and the added liabilities to the balance sheet We.Connect inherited from Exertis, their balance sheet and working capital still are in good shape. Although ROIC and NWC as a % of revenue declined, I am still very pleased with the moderate decline. Buying a business which has not been operated properly since for ever, which has more revenue, is loss making, and working capital was not optimised. This is a good accomplishment and I am looking forward to improved metrics in 2026!

Valuation update

My previous valuation can be found in my previous article, which I will link once more since I will be referring to a few changes I have made!

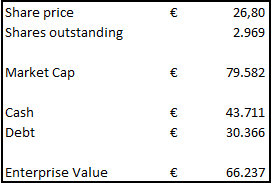

Based on the current share price the company has a market capitalisation of about €79.5m, compared to an EV of just over €66m, which is due to the current net cash position the company holds.

If we divide this by the current €14.2m in EBIT the company made, the company is trading at 4.6x EV/EBIT. Which is slightly cheaper than the 4.8x EV/EBIT it was traded at when I first pitched the stock, when the share price was 25% lower….

If we adjust the net income for the one off, it is currently trading at a P/E of 6.9, both the metrics are looking back but I see no reason for a worse business tomorrow compared to yesterday!

Some people I have spoken to have said that the entire thesis is banking on Exertis, currently I believe this is not reflected in the stock price, but I also think the core business is undervalued. So what does the future look like?

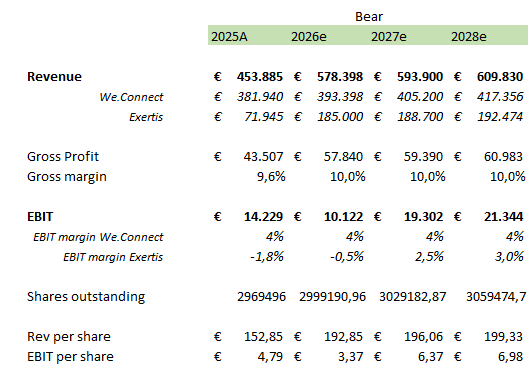

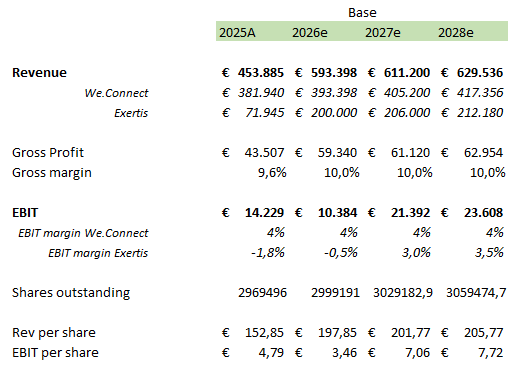

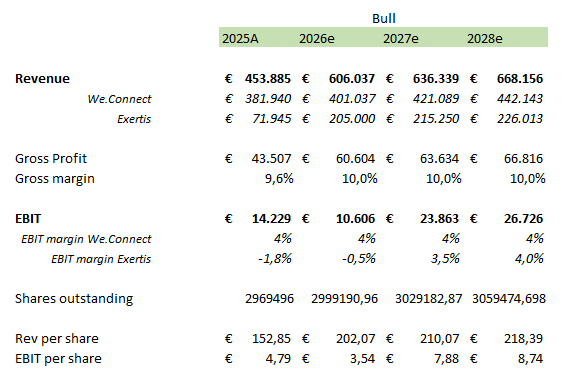

If Substack had a decent zoom function this would have looked better for you guys but it does not, so I believe this is the only proper way to show you my napkin math.

Compared to my previous valuation, I have increased the expected Exertis revenue contribution for 2026 and beyond. The annual report showed that Exertis generated roughly €72m of revenue in the four months after acquisition, which annualises to more than €200m. I do not want to extrapolate that number, as Q4 is seasonally strong in electronics sales, but it does suggest that Exertis has lost less revenue compared to my expectations (which were very conservative)

In all three, the legacy We.Connect business continues to grow at a modest rate, while Exertis gradually improves from loss-making to a positive EBIT margin by 2027. The main difference between the cases is how much revenue Exertis can retain and how quickly management can repair margins.

The important point is that this is not a revenue problem. We.Connect has clearly bought scale. The question is whether that scale can earn the historic margins.

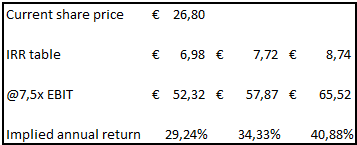

The table below shows the valuation impact. At the current share price of €26.80, applying a 7.5x EBIT multiple to my 2028 EBIT-per-share estimates gives implied values of €52, €58, and €66 across the bear, base and bull cases.

So the market is still pricing this as if the Exertis integration is highly uncertain, which is fair enough. If We.Connect can turn Exertis into even a modestly profitable distributor, I believe I will be looking at quite the return!

Disclosure

I/we have a beneficial long position in the shares of We Connect ($ALWEC.PA) I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.

I am also likely to purchase additional shares in this security!