Vistry Plc

Valuing Vistry; A cheap builder, a cleaner balance sheet, and more upside than the market seems willing to price

TLDR; Vistry is a stock that has been and is going through a transition, a balance-sheet repair, and hopefully an additional large buyback . At today’s roughly

5.6x P/E;

8.7x 2026 EV/EBIT, please continue reading it is more nuanced and probably cheaper!

The market seems to be pricing in a business with structurally weak returns, yet management is explicitly targeting stronger cash generation, lower debt and a move to net cash. If margins recover even modestly, and if some of that cash flow is used to repurchase shares, while liabilities come down, the equity value per share can move a lot. There is a lot of risk in this story, but it may be one where the market is still too anchored in the past to do the propper maths.

Introduction

I have previously mentioned a new possible “initiative“ that I wanted to start, where I publish my own critique and valuation report on “popular“ substack companies. I have no gain in trashing on companies so it will always be, at least in my opinion a fair valuation. I start this process open-minded since I want to value the company and perhaps profit from it in the future, I have no incentive to have a pre-defined opinion on the company.

It is surprising how many great articles one can find on a single stock on substack when you leave small cap land. Since the stock is well known, my questions would then be:

“Is there any alpha here?“

“Why would the market misprice something that is highly liquid and very well known?“

I guess we are going to find out

Good write‑ups on Vistry

To start my shameless copying (I do not truly believe I am copying), I will suggest my favorite and most informative articles. You must read these articles first, before continuing my article since I provide little background.

James Emanuel — “The Vistry Mystery”

It mostly focusses on the model comparison between Vistry and NVR, talking about what the capital light model really is. It also discusses differences between NVR and Vistry and some key assumptions and why they are possibly wrong.

Matt Newell — “A Classic Troubled Value Investment”: I really like Matt his writing style and I have read a lot of his articles, so I am quite sad that he is leaving the finance / investment substack. I do believe he will continue to do good in the world and that is something I admire him for.

Now lets continue his Vistry post…

This is the most disciplined of the Substack pieces on normalising earnings, then adjusting the “effective market cap” by discounting expected capital returns. Very clear and explicit assumptions (exceptionals, tax, discount rate) and a clear link between capital release and valuation, which I will also talk about.

Dr. Mischa Schmidt — “[Free] Vistry: Breaking the (Land)Bank”: Does a very good job of articulating the “capital release + buybacks” mechanism and explicitly tying returns to capital employed rather than just margins. It also evaluates what ROCE ranges would mean for the thesis (not binary).

Jaco Enslin — “Vistry Group PLC” (Balancier Capital / Substack): unusually good at constructing a simple model to test whether 40% ROCE is even possible given a 4‑year landbank, a 65/35 tenure split and a 12% margin. The article also highlights a key issue: why own so much land if most volume is partner funded.

Eli Courtney — “Vistry group” (a Warren of Ideas): a clear base/bear/bull per‑share valuation , mainly focussed on “owner earnings” as the key value driver.

I have read a fair few other Substack posts that mention Vistry, but deemed them less reliable or qualitatively less and these cover more than enough to gain a basic understanding of the stock.

Podcasts

Outside of great substack articles I would also recommend the two Yet Another Value Podcasts in which Adam Patinkin goes into great depth explain a lot of important assumptions but also misconceptions about the business!

07-01-2024:

04-04-2025:

Lastly, just as Matt Newell suggested I can really recommend this article / presentation to further understand partnership models and how this model will help deliver the homes that are needed in London and the rest of the United Kingdom!

Click the link: Housing Partnerships Delivering the homes that London needs

Important to know:

This research is from 2021;

Countryside was NOT part of Vistry at the time of developing the properties.

Short summary

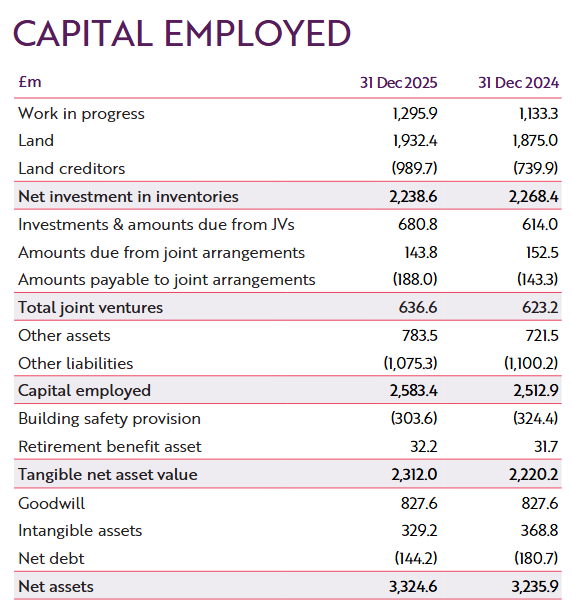

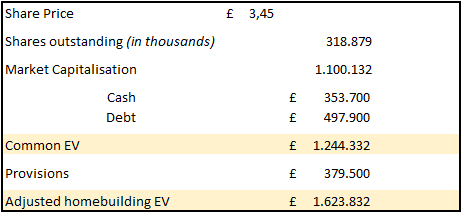

At the time of writing this the stock declined to 380p and has since declined further to a level of about 330p. Vistry today has multiple problems and is thus priced as a company with: impaired credibility, heavy working capital, and hardly a proven “capital‑light” ecomic model, despite a very large Partner Funded footprint. The share price implies an equity value of roughly £1.05bn, using the FY2025 year‑end share count of 320.8m ordinary shares in issue (330p × 320.8m ≈ £1.05bn).

On FY2025 reported figures, the market is valuing Vistry at about 0.33× IFRS book and 0.48× TNAV. Valuations below book often imply that investors or “the market“, that either some balance‑sheet value may not be realisable at anything like book, and/or the equity is not trusted to earn adequate returns on that capital. Either of these conclusions are not irrational when you see inventories of £3.23bn, land creditors of £0.99bn, and an average daily net debt of £733.7m in 2025 that management explicitly describes as “higher than targeted”.

If the Partnerships transition substantially succeeds by end‑FY2029, this would not guarantee a high multiple, due to “failings“ attributable to current management. If there is a re‑rating this should be driven by higher and more reliable EBIT, and a continuous lower capital intensity (inventory and average net debt down).

To reiterate; if you want to read about management, history, guidance, and accounting issues, I refer you back above to all the relevant and quoted substack articles and podcasts!

Partnership vs Traditional

I am not a life long shareholder, at all times I try to maximise my 3-5 year IRR adjusted for the amount of risk. Therefore I am curious what the best way to go is for Vistry, because might the traditional model with more revenue and better net profit margins be a better option? Why would shareholders sacrifice revenue and profits for a lower capital base with a higher ROCE (Return on Capital employed). The main question investors currently face is about how quickly profits turn into distributable cash, and whether Vistry can shrink the capital trapped in land and work‑in‑progress without destroying returns or risking liquidity.

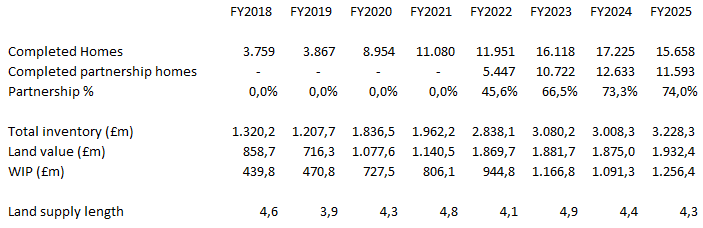

Vistry has already shifted towards Partner Funded delivery in unit terms, roughly 74% of total completions were partner funded1. Great that they use a lot of partnership deals, however, the company only becomes a partnership business when the balance sheet also represent it. I mean; inventories at FY2025 year‑end were £3.2bn and land creditors £1bn. Does not shout capital-light partnership at me…

In other words, Vistry is already operating like a Partnerships, but remains financially asset‑heavy. That mismatch is why mr market still prices it like a levered cyclically exposed builder rather than a asset light partnership, and why the most profitable path for current shareholders is as follows:

De‑risk and prove capital release (inventories and average net debt down; landbank more controlled; liquidity buffer maintained).

Exploit undervaluation via conditional buybacks/specials, because buybacks at a large discount to TNAV can be mechanically high‑IRR for existing shareholders—provided the “tangible” balance sheet is genuinely realisable and liquidity is not fragile.

Retain selective reinvestment capacity where returns are demonstrably high (high‑ROCE partner frameworks, controlled land, and standardised delivery), because the point is maximising per‑share IRR, not maximising near‑term payout.

If Vistry cannot demonstrate declining total inventory intensity and falling average debt within the next 12–24 months, the Partnerships thesis becomes far less compelling. At that point shareholders have a mixed model with the worst of both models: Declining revenue and margins and high capital intesity.

Business change vs Balance sheet change

When the business changes the balance sheet either slowly changes or takes a very big sudden hit. Examples are Microsoft their shift towards SaaS, which is a slow change and can be seen over the years between 2010-2015. A very sudden change would be a different holding of mine Calumet, where the change in RIN prices (renewable diesel) and the EPA ruling has changed the balance sheet within 6 months, from high liabilities and debt, to cash generative.

I believe it is very important to check on the balance sheet of a company I am looking; for the simple reason that it supplements the information of the P&L and what management is telling you better than anyone can. Management tells you that they are selling a lot of inventory; look at what the inventory does on the balance sheet. The P&L is telling you that the sales are through the rough; look at what AR and the cash are doing. However, be aware that this is the reality at one point in time, WIP could be sky high and the invoice could be send a day later and the WIP could be near 0.

Please point above where you can see the, in the balance sheet lines, where the capital light model started?

Some definitions to help:

Total inventory: the total balance sheet value of Vistry’s development housing stock. This is mainly land held for development plus work in progress. It is not plant or equipment.

Land value: the carrying value of land held for development on the balance sheet. Vistry records this at cost and this covers land in the course of development until the sale of the asset.

WIP (work in progress). This is money already spent on homes and sites that are still being developed and not yet completed/sold, including things such as build costs and site infrastructure spend.

Land supply length: the number of years of supply represented by Vistry’s land bank. The land bank is the total number of plots expected to be deliverable on land owned or controlled by the Group, including joint ventures, with planning consent. So land supply length is simply how many years that land bank should support delivery.

Vistry and people who are long the stock keep hammering the partnership percentage numbers and as the table above shows it is increasing! But bulls be aware, so is the land value and the total work in progress!!!!!

I have no issue with the work in progress increasing, since this would also be the case if they simply complete more partnership projects. The land bank is something I would expect decrease, the increasing number can only be explained by management buying more lots, since the value is held at cost and it not revalued over time.

What this tells me is that the company is changing but the balance sheet is simply not. This offers both an opportunity (do I smell alpha) as something to be very concerned about as a possible shareholder. I will talk more about this in the valuation part.

ROCE theory

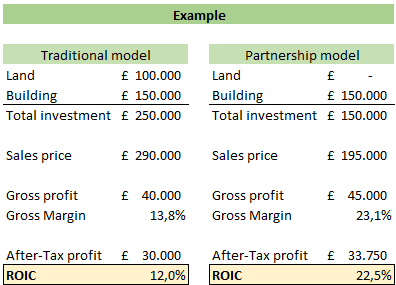

The whole point of switching to a partnership model is to reduce the amount of capital that is required to keep the business running, to make it more “lean“. The first question I have is why would I want my business to be lean? Does that create a moat or more profits? Short answer is that it creates more profits per invested pound into the business.

I have seen many estimates of how the two model differ and some really get to some rosy ROCE numbers. In the traditional model I assumed the selling price is: the building for 1.2x costs and the land for 1.1x costs, which are both fictional numbers. For the partnership model I used 1.3x building costs. The reason for this slightly higher sales price is the on average better margins Vistry achieves in Partnerships.

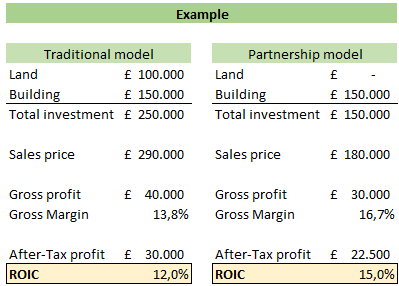

So my assumption would be that the total sales would decrease, but due to the slightly higher margin of sales, the ROIC nearly doubles. Even if the sales margins are not better in the partnership model, the ROIC is still higher! The total after-tax profit would significantly decrease, however, since partnerships already make up over 74% of total completions impact will be minimal.

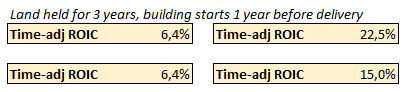

The image above does not account for the fact that Vistry holds the land for multiple years before building on the land. If you assume that Vistry holds the land for 3 years and building the house takes about a year, the following happens to your ROIC:

To me it is clear now they want to change the model, not to increase revenue (at least not per house), but to increase the incremental return per project.

For non UK based investors the ROCE might be an unknown metric, it is actually quite common in the UK and is quite similar to ROIC. Below I have summed up the two easiest ways to calculate the ROCE:

The formula above is quite hard to calculate for shareholders, below is an easier approach which also might feel more intuitive for investors who usually use ROIC

Managements medium-term ROCE target is approximately 40%, is this even possible for Vistry?2

Yes, but let me explain a lot of conditions that will need to be met to achieve this. I believe this will be achievable at the partnership segment level, but only after the balance sheet has been fully reshaped away from legacy land-heavy inventory and towards a predominantly pre-sold, partner-funded balance sheet. In other words, 40% is plausible but requires a large shift.

The key point is that ROCE is a function of the operating margin × capital turns. If a partnership homebuilder is targeting a 12%+ operating margin and a 40% ROCE, same source can be used for both these numbers as the previous source, then it needs revenue to run at roughly 3.3x average capital employed.3

This tells us that for every £100m Vistry has in capital, they need to generate about £330m in revenue. As an outsider this is quite hard to judge since I have no idea how much capital will need to be in the business when it is finally lean. There is “evidence“ that 40% is possible. Vistry stated in 2023 that, excluding the former Housebuilding business, its Partnerships business maintained a ROCE of ~40%.

Timber

Vistry’s three timber-frame factories are described as core to its operational strategy; in 2023 the group said those facilities had capacity for ~8,000 units, with output planned to rise from 2,500 units in 2023 to over 4,000 in 2024. The strategic logic is that if Vistry can standardise the houses, have central procurement, and therefore build the houses faster this is easier than without the timber-frame factories.

That said, even if the partnership segment can do 40%, the group may not. Vistry’s reported group ROCE was 21.3% in 2023, 14.6% in 2024 and 13.9% in 2025, well below the medium-term target. The reason is not that the partnership thesis is wrong; it is that the consolidated balance sheet still carries too much capital in land, work in progress and slower-turning legacy assets (traditional home builder assets). Management itself has said the roll-off of the former Housebuilding land bank and the release of capital from inventory are key drivers of future ROCE improvement. But as I will state further on this has taken a while…

Further explanation on ROCE…

I started reading the transcripts for an additional part of the article and the CFO explained the long term capital employed they want to achieve:

So in terms of capital employed, this is not where we wanted to be yet. We’ve said a couple of years ago, our rough target is to get to capital employed of around GBP 2 billion, and we’re significantly above that.

Assuming this £2B capital employed, this implies an EBIT of £800m which was stated as their previous goal. For some reason I completely forgot that medium term EBIT target was this £800m.

Looking at this overview, my first thought is: “They want to decrease it by £500m, how will they do this by freeing up as little cash“. This can either be great and £500m in cash can be released to buyback shares or they can be write-downs and impairments and no cash will be released.

Joint venture (JV’s)

For Vistry, a joint venture simply means it does not always buy the land, fund the scheme and take all the risk on its own. Instead, it often sets up a jointly owned project company with another party, puts in some equity and loans, and then shares the costs, profits and risk with that partner. The JV line on the balance sheet is Vistry’s share of money tied up in those jointly owned developments. It is not one single JV either, Vistry uses this structure with housing associations and their development arms, government-backed bodies, regeneration partners and sometimes other housebuilders4.

What are they building? Mostly large residential communities and regeneration schemes. These are usually mixed-tenure developments, so a blend of private sale homes, affordable housing, shared ownership and sometimes private rented homes.

Sherford is a good example: Vistry and Latimer are delivering another 1,200 homes there as part of a much larger new-town scheme near Plymouth. Hestia, the new JV with Homes England, is meant to bring forward large sites across England and deliver communities of roughly 400 to 3,000 homes each.

So the simple way to think about Vistry’s JV business is that it is a way of doing bigger, more capital-heavy schemes with partners, instead of carrying the whole burden itself.

The government (as an ally this time)

The labour government won the last general election in the UK and in Europe left wing governments are often bad for companies and good for poor people. The issue that is prevalent in most of the Western world is the building housing shortage. This is in my opinion the current largest issue facing the west and I believe the labour government is with me on this. They have announced a few very extensive measures which will help Vistry build more, faster, and perhaps even cheaper.

The first step the labour government made was to improve land release5 and planning throughput6. The December 2024 revision to the National Planning Policy Framework brought back mandatory housing targets for councils, kept the brownfield-first bias7, and made clear that authorities should review Green Belt boundaries where housing need cannot otherwise be met. Vistry its model is heavily exposed to larger, mixed-tenure partnership sites, which are often in the aforementioned places.

The second policy shift is arguably even more relevant to Vistry: the government has put money behind affordable housing and improved the financial visibility of housing associations and local authority partners. In March 2025 the labour government added a further £2B to the Affordable Homes Programme as a bridge to the next funding cycle, and it has since launched the new 10-year £39B Social and Affordable Homes Programme for 2026 to 2036. Alongside that, the government confirmed a 10-year rent settlement allowing social housing rents to rise by up to CPI+1% each year from April 2026.

For Vistry this is amazing news because it is a partnerships-led affordable housing delivery business. This is due to the fact that Vistry is the largest affordable home provider and hasdelivered one in seven of the country’s affordable homes in 20258 and even better one in six in 20249.

The Planning and Infrastructure Act received Royal Assent in December 2025 with the aim of cutting delays and speeding up housing and infrastructure decisions, while the new local plan-making system came into force in March 2026 with a 30-month timetable and at least £14.1 million of implementation support for councils in 2025/26. Vistry obviously benefits most when councils can get plans adopted and can fund affordable housing.

But is it so great? Adding £39B over a 10-year period is roughly £4B a year, which would translate to growth of about 10% in absolute terms for the enitre sector. The question I have is whether this really drives a meaningful uplift in Vistry’s affordable housing revenue, or whether a good part of it simply stabilises a stressed system.

Vistry tells us that the annual affordable housing delivery should rise from roughly 59,000 to 70,000 homes, which is quite a bit but we can hardly call it explosive,. This increase still has to work through planning delays, partner capacity, cost inflation etc etc. Given Vistry already delivered 8,752 affordable homes in 2025, or one in seven nationally, I think that this looks more like a decent medium-term tailwind than a massive change in earnings power.

Management

I feel no urge to discuss management in depth, mostly because I feel that I know most information pieces I would want to know from the previous articles. I would again refer all the readers to the other great articles.

The current CEO is Greg Fitzgerald. The company’s describes him as the “driving force” behind the group, his planned retirement would mean losing a driving force, which is quite the issue. The Board has already said the Chair and CEO roles will be separated, with Greg stepping down as Chair in May 2026 and remaining CEO for up to 12 months while a successor is found.

On Greg specifically, the experience is hard to argue with. He was appointed to the Board in April 2017. Before that he was Chief Executive of Galliford Try from 2005 to 2015, having run its housebuilding division from 2003, and before that he founded Midas Homes. I find it less useful to discuss Greg in length and I would rather spend my time on other parts of the analysis since he will be leaving soon. My general take away is that Greg knows this industry by hearth, this is what analysts have talked about. He knows how to operate and cut costs, the new model might be a bit harder for him and I think a new CEO might be very well suited. My take away from the conference calls and other investor interactions is that Greg trusts Tim (CFO) completely. CEOs often like to be in the shine, Greg has these tendencies too, but he lets Tim shine where Tim is good at: The numbers!

Tim Lawlor is a different type of operator, and that is a good thing, you need ying and yang on the board. He joined the Board in November 2022 as part of the Countryside deal, having been CFO of Countryside, and before that spent seven years as CFO of Wincanton. He looks more like a broadly experienced listed-company finance executive who has then dropped into housing.

In terms of actual accomplishments, Tim’s biggest contribution so far is the clean up after the 2024 South Division mess, subsequently tighten controls, managing the sticky working-capital position and keep the lenders at ease while the company was in slight turmoil. In July 2025 Vistry refinanced its £500m revolving credit facility and £400m term loan out to April 2028 on existing terms with the same eight lenders, which is quite important in my eyes. It is not exciting, but it is a real vote of confidence from the banks after a messy period.

What I like about Tim from the conference calls is that he sounds like a CFO, I have met a few. He says things such as:

“the capital and the balance sheet is proving to be too sticky”

“we need to get the sales going”

Which is the truth and all shareholders can see, but very few are willing to accept. He is also unusually clear on the ugly side of the current business:

Daily debt vs month-end debt;

Land creditor discount unwind;

Finished stock;

Deferred income;

JV cash movements;

and the fact that lower margins may be acceptable if they release cash. That does not make him an exciting CFO, but it does make him credible.

A CEO Change

I finished writing the article, with exception of the valuation, and Vistry came with an announcement informing investors they internally found a new CEO. The new man for the job is Adam Daniels. A name I have not heard before….

My read, which is very uninformed, on Adam Daniels is that Vistry has promoted a partnerships operator who has come up through the company. He started in housebuilding at Bloor Homes in 2009, moved to Galliford Try Partnerships, then joined Countryside Partnerships in 2016, where he helped establish the West Midlands division. From there he moved through managing director and divisional managing director roles across the West Midlands, East Midlands and South West, and Vistry says those regions contributed more than £50m of EBITDA under his leadership. After the Countryside deal, he became divisional chair of Yorkshire, North Midlands & West, one of Vistry’s two largest operating divisions.

After searching and struggling I found some articles where Daniel Adams was mentioned. I do not think any articles here give information which is useful to an investor since they are very simple PR phrases. The articles do show the constructive and positive relationship the Vistry / countryside business has with their Counties / Councils / JV partners. The articles can be found in the footnotes10

Also please take the boards commentary with a grain of salt, of course they are going to say that they like the guy, the hired him…

Some words for management

The issue I have is that management seems untrustworthy and not because they are terrible operators, the contrary, I believe Greg and Tim are good at their Job. I take issue to the fact that they still claim 40% ROCE without a clear target, they still claim 12% operating margins without explaining how they will get there, they still claim they are having significant cost advantages while I cannot see it when I compare them to peers, and lastly I hate how they let investors believe they are anything close to NVR. When you work with mostly poor or bankrupt housing commissions or councils you will never be anything close to NVR and it is YOUR job to communicate this to shareholders!

Capital allocation

I will get to the valuation shortly, but first the capital allocation strategy. I believe sound capital allocation might be more important than their revenue growth over the next 3 years. I believe if management is prudent with their cash, the company should be able to buy a significant number of shares outstanding.

I hope that I do not need to explain my highly educated readers what the reason is that I want them to buy back shares (Hint: Higher EBIT per share).

I expect management to be able to generate several £100 millions of pounds to buy back these shares or repay debt, my preference is to decrease the amount of shares first. I do understand the debt reduction for financial agility if the opportunity arises, although the sector is no stranger to moderate debt levels. I expect the cash from balance sheet improvements, no operational cash flows, to come from the following improvements:

Finishing their traditional housebuilding WIP and selling finished housing;

Greg said: I demanded that each business unit go forth and double their sales rate

Tim said: we need to get the sales going. We recognize that, that may have some margin implications, but it will give us good momentum. And crucially, it will generate cash and reduce our WIP.

Selling non-strategic plots;

Decreasing their land bank size;

The overall size of the land bank coming down, we probably expect a similar sort of level next year. So we’ll continue to wind down to have a land bank of somewhere around 3.5 years of coverage in the land bank.

The quotes I have placed are from the most recent conference call and offer insights in management their plans. I have no opinion on each of the specific parts, I do believe that the total immediate cash flow benefit should be about £200m in 2026. I believe this entire amount SHOULD be used in share buybacks, since management should reach their net debt goal (they want to be net cash), by simply using operational cash and this should be achievable with £200m in operational cashflows.

In terms of capital allocation, so we've got GBP 30 million to go on our share buyback… and we'll complete that in the year. I think previously, we said we'd completed it by the AGM. It may now be slightly slower than that.

And then come the half year, we will, as a Board, look at where we are with the progress we've made on sales, the progress we made on debt reduction and determine if there will be an interim distribution announcement.

This does not seem like a lot, but they will buy back 3% of their shares before the half year mark. As can be read above management will decide on expanding the buybacks at the AGM, which will be the 13th of May. At that point management should be nearly certain of what this year will look like due to the predictability of their business, revenue can be slightly off due to completions. I sincerely hope they announce a 20% buy back and perhaps even update regarding revenue and profitability.

Maybe the most important question: Shares could have been bought back in the previous year(s) why would this thesis now hold?

The reason buybacks make more sense now is not that they suddenly become magical, but that the set-up is better. The stock is cheaper (my opinion), the business is still standing, and the share count has decreased11. Decreasing the shares outstanding has already created value: adjusted profit after tax rose only 3% in 2025, but adjusted EPS rose 6%, with the annual report explicitly saying that was “supported by fewer shares being in issue as a result of the ongoing buyback programme”. The same logic applies to operating profit per share as well.

Vistry is buying back stock in a market environment that has sold off for their sector and their specific stock. In that sort of environment, if management believes the shares are undervalued, buybacks are the best method to signal confidence and increase future returns. The downside is that they slightly reduce liquidity, but they also put a steady bid under the stock when sentiment is poor and other buyers disappear. The best thing management can do is stay solvent, stay operationally stable, and keep retiring shares at these lower prices. Then, when volumes, margins or sentiment eventually lift, the recovery is spread over a smaller number of shares, which improves the rate of return for shareholders.

That is my short answer to why I believe management should buy shares and why I believe this is still the best decision.

A little extra

The worst thing about being a slow writer and someone who likes to research a company while he slowly writes, is how often I come across articles, papers or videos which are on the topic I am researching which just warrant attention. Of course, this happened again with Vistry with the following Podcast / Interview:

I actually wanted it slightly smaller, but I have no clue how to adjust this, I guess free advertising to my 50 readers!

Disclaimer, I only read the transcript from where he started to talk about Vistry.

First of all if the transcript is as good as the podcast I can imagine this a hard podcast to listen too. It seems like he has a lot of knowledge but he is sending a lot of it my way, even via a transcript.

Below I will highlight his main points and will loop back on each of them, some of which I completely agree with…

Execution and integration risk: Vistry was trying to integrate three acquired housebuilders across a very wide UK footprint in a short period, and that hitting ambitious volume targets while doing so would be very difficult.

Completely agree, although I believe the main issue was underestimating the countryside acquisition, not all the acquisitions. Most acquisitions destroy value, short term this has destroyed value, and I hope for current shareholders they will stick to their current business and not acquire anything new the the foreseable future.

Volume assumptions looked too aggressive: The company’s target to move from roughly 17,000 homes a year to at least 25,000 relied on growth that had been very hard to achieve historically, and he did not think government funding or planning reform would be enough to move the needle quickly.

Completely agree, I think this growth will be very hard to realise. This is the reason they used it as a medium-term (no specific date) target so they could simply postpone it. I think getting to about 22.000 is possible with moderate growth assumptions in 2029.

Margin assumptions in the partnerships model looked too optimistic: he said the model was not “cost-plus”, because Vistry locked in selling prices on long-dated projects while still bearing labour and materials risk, so if build cost inflation ran ahead of house price inflation, margins would disappoint.

I believe, anybody correct me if I am wrong, that Vistry can retain a certain amount when prices shoot-up but indeed they carry a large part of the risk. Depending on the contract they can increase prices or surcharge the client.

Control and culture concerns from the profit warnings: The sequence of profit warnings are a sign that management did not initially know the full extent of the problem, which is linked to weak systems, difficult post-merger integration and underlying cultural issues in a geographically dispersed organisation.

The South division has been part of Vistry since before the acquisitions, I believe it was started in 2021 as part of the legacy housebuilding business. So not this has very little to do with the acquisitions. Yes, the control, culture and checks were not in place and this might be due to the focus on partnerships, this is a lazy excuse. I believe management has now implemented both checks and control, I hope the culture will change over time.

Leverage and liability concerns: Headline net debt understated the true balance-sheet burden because investors also needed to include land creditor debt and provisions, especially building-safety related provisions, which in his view were real liabilities that should be counted when thinking about enterprise value and financial risk.

I will get back to this in the valuation part, but yes again I have to agree.

All of the above points are very good points and the main issue in all of these points is not that it is a bad business or even a terrible sector to be in. It is all management, the targets: the leverage, the culture and checks and lastly the terrible communication. I really hope the new CEO is willing to communicate and talk with shareholders and not just the large institutions, engage with smaller shareholders they can help management more than they often think.

Valuation

I am not an above average investor, although my historic returns do indicate there is something going on in my brain. I want a very simple thesis and I want to invest in very simple companies, or easy to understand companies who perform difficult tasks. I believe making intricate DCF’s is extremely insightful to understand and dive deeper into specifics of the company. I also believe that my best investments are based on a future catalyst(s) with the general indication that the stock is cheaply valued, examples:

NewPrinces

Calumet

Again I chose only to mention companies I have written on the substack, so if you want you can go back and read about the companies. I hope you realise both my writing and my investment knowledge and skills have both improved. Both companies I knew were cheap on a current and future base and there was a significant catalyst going to happen.

Back to Vistry…

Debt

Vistry finished 2025 with £497.9m of gross borrowings and £353.7m of cash and thus net debt of £144.2m. A slight improvement in the was better than the £180.7m reported at the end of 2024, but still not where management wants the business to be. The issue is that the year-end figure “improves“ the underlying strain on the balance sheet, because average daily net debt during 2025 was still £733.7m. A lot more debt was actually used and tied up through the year in land, WIP and delayed payments. Management said the following during the January conference call:

Greg: Your point about net debt, we would still expect to be net cash year end

Tim: But absolutely going into that, our target is to say how -- what do we need to do to get to net cash at the end of this year.

Management is explicitly saying the goal is not merely to lower net debt, but a move to net cash by the end of 2026. If they achieve that, it would mark a change in balance-sheet quality and give investors much more confidence that Vistry’s profits are being converted into cash rather than staying trapped in inventory and working capital.

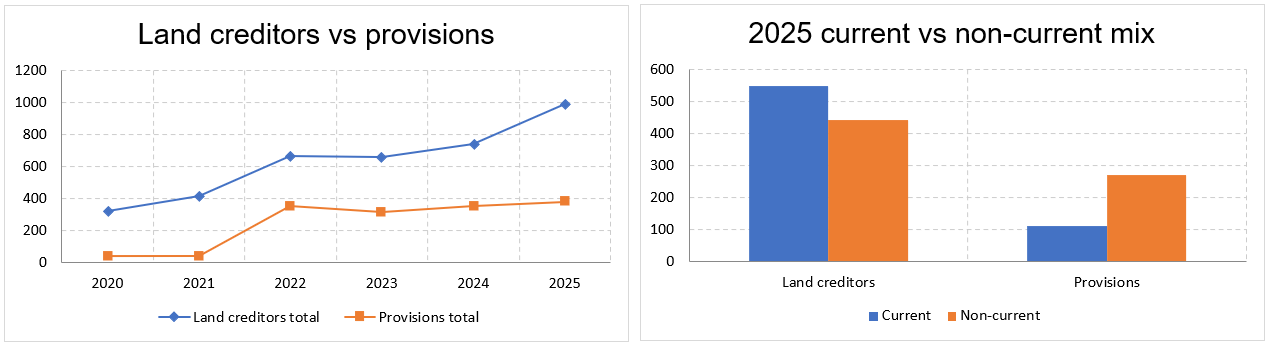

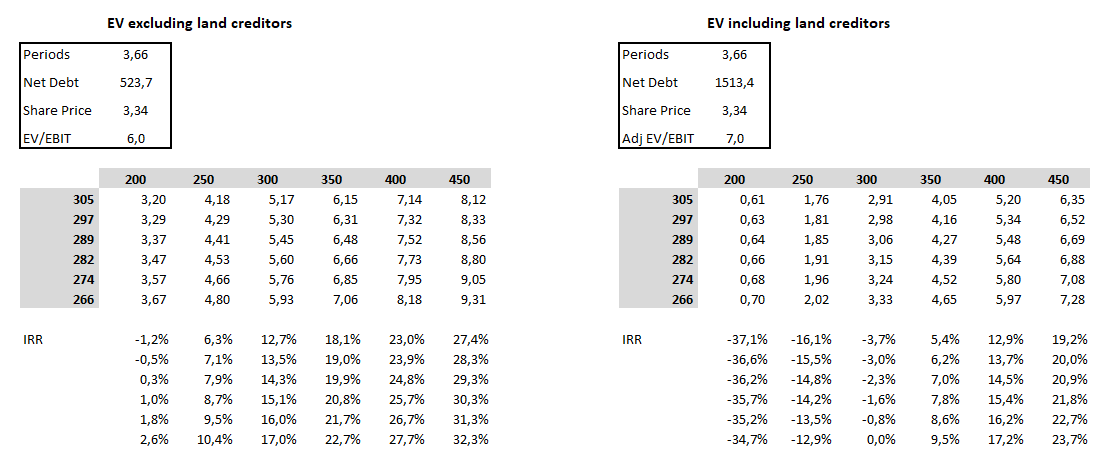

Most write-ups mis two essential parts of their debt stack, which are or could result into future liabilities and most important to me: future cash outflows. Land creditors, which are future payments to land owners which Vistry has taken control of and provisions especially for fire safety. Some people might not agree, but what is the reason that we add debt to create the EV? To reflect possible future payments that arise due to choices that have been made today and have possibly increase todays earnings. The exact same thing holds for both provisions and land creditors, although the latter could be argued due to the fact that Vistry pays the land owner as soon as they start developing.

Below I have illustrated the massive increase in liabilities which are often excluded in the EV:

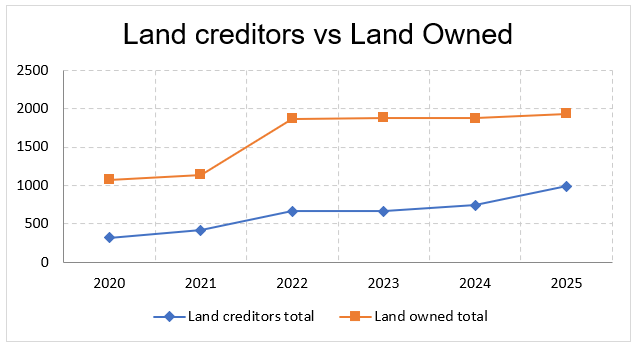

I am not against using land creditors, for the asset-light model this even makes a lot of sense. Vistry “reserves“ the land in exchange for payment once the permits have been approved and the building will shortly commence. At that point in the partnership model, Vistry will often have received a partial payment for the land. The problem lies with the fact that while the total amount of creditors has increase, the total amount of owned land has not decreased over time, as can be seen below:

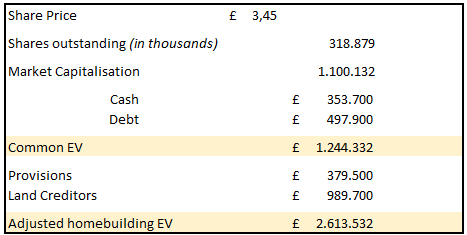

If we include the most recent numbers for debt, other financial liabilities, cash and shares outstanding we get the following share structure:

I always doubt my valuations, because I simply make errors in life. The main doubt in my valuation here is whether to include land creditors. On the one hand I believe if they sell the land on the asset side they will receive no cash since they have to pay the creditors, which makes land creditors feel very debt-like to me and something I should include in a more conservative EV.

On the other hand, I also know that the land is already recognised gross on the balance sheet, so if I add the full land asset and then also add the full land creditor balance as if it were completely separate, I may be double counting the same assets. The liability is real, but it is also funding an asset that is already there. So I end up torn between using standard net debt, which probably understates the true financing burden, and using an adjusted EV including land creditors, which may overstate it unless I also think carefully about what value I am assigning to the land itself.

I think the best way to frame it is to look at both: standard EV for comparability, and then a more conservative, EV that includes land creditors, while being explicit that the truth probably sits somewhere in between.

Revenue & Earnings

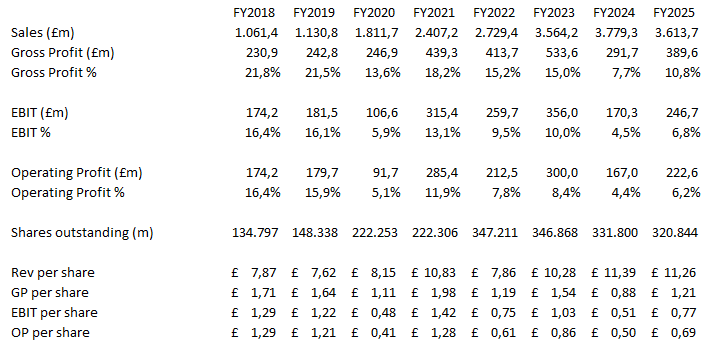

I have pasted a portion of the P&L overview I have made above, I will refer back to this multiple times!

I will not make my life harder than it must be and I will assume the revenue of Vistry will grow by about 3% - 5% in the coming years. I believe homebuilders in a normal market should grow at inflation, since the market they operate in hardly every expands. Bulls would argue that their affordable housing division will grow fast in the coming years, I would argue they should expect slower building in their private renting business, feel free to tackle this point in the comments! I do recognise that there is expansion possible in the affordable sector and will take this into consideration for the growth / sensitivity table.

That was quick lets go to earnings power!

On the previous conference call the CFO said the following:

So I think -- the full year margin for this year ended up at 8.4% for ‘25 and ‘26, which is actually this year, for ‘26, we’d expect to see some margin progression, perhaps not to the extent that we saw in the second half of the year, but we’ll be edging up from 8.4% this year because some of those lower-margin legacy sites will start rolling out.

If you guys paid attention, there is a difference between the margin the CFO is talking about and my operating margin. He is using the adjusted operating margin, which strips out certain items and uses adjusted revenue, while my number is the real IFRS number. I think my number is cleaner and allows for less earnings management, therefore, I will continue using and referring to this number.

What metric to use?

For a homebuilder, and especially for Vistry, EBIT is in my opinion the closest proxy for free cash flow because the business is not held back by a big recurring fixed-asset burden in the way a factory business, airline or utility would be. The real cash swing within the company comes from land, work in progress, receivables and creditor timing12.

I try to think steady-state cash earning power, EBIT is usually more useful than EBITDA because it already partially includes replacement costs over time for the operating asset base, while avoiding the massive noise that comes from annual working-capital swings. Management’s medium-term targets included an EBIT target, partly because of how good it is. In the March 2026 call Tim Lawlor said that the cash-flow bridge was really about inventory, receivables, deferred income and JV funding rather than any large capital expenditure burden. Even the capex he highlighted was mainly incremental spend on Vistry Works machinery.

Conclusion

The reason most investors like the company is because screens optically cheap and has had a large decline, human nature likes that. Vistry currently trades at a PE of ~5.6, like a lot of debt heavy companies, a PE valuation is not the best way forward.

I want a company to be cheap at this point in time, not in the future. I want to buy a dollar at ten cents. SO what is Vistry currently traded for?

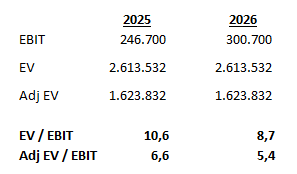

Depending on your view of the land creditors, Vistry is trading at an EV/EBIT of 5.4 to 8.7x 2026 expected earnings and 6.6x to 10.6x 2025 earnings. The average valuation for US home builders EV / EBIT was 9.4x13. I would say that is close to what I think it would be on average across the cycle.

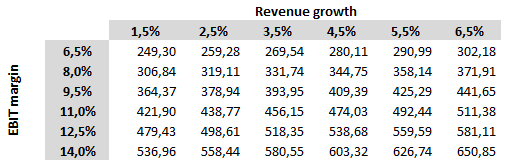

I often find it useful for young or high-growth companies to make a revenue growth split per year and what the margins will do. This is also the way to go when a business is highly diversified or has a lot of different growth per division. This is not the case for Vistry, this is a mature company where I believe we can expect steady revenue growth with an increase EBIT level up until 2029. The model below illustrates what the EBIT could reach until 2029.

The growth table above should be read as, if over the period 2026 - 2027, Vistry has an average revenue growth of 3.5% and an EBIT margin of 8% at the end of 2029. The total EBIT would be £319m.

I believe the fair estimate would be revenue growth of about 3.5% and an EBIT margin of 9%, this would be below the historic post-covid average. This would result into the company achieving a total EBIT of ~£400m.

I will assume they generate about ~£600m of FCF from operations between now and 2029 and they will mostly buy back debt and reduce liabilities with that cash, to increase the future ROCE.

Shares outstanding should decrease by about 15% in a moderate repurchasing scenario, one might think this is some made up number, and because I do not have management commentary of course it is. I believe they should be able to double the amount they repurchased in the last two years14

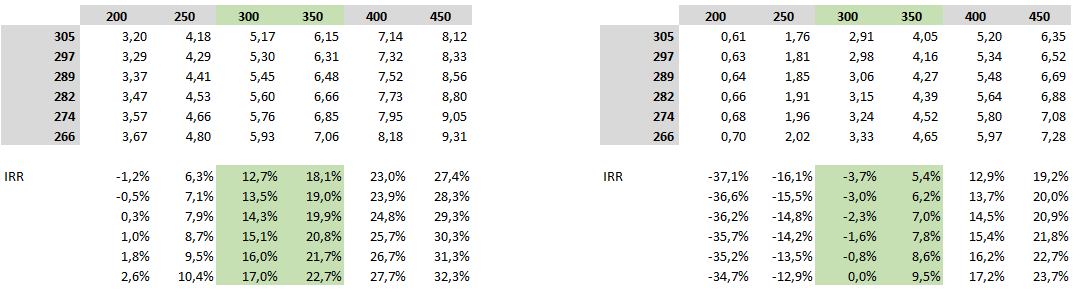

The valuation sensitivity tables can be found in the screenshot above, the difference between the IRR sheets is simply the difference the EV calculation. The differences is indicated above the graph and the explanation can be found in a previous chapter.

I try to widen my confidence interval not tighten it in general. I want to have a large range of outcomes and see what happens in each of those scenario’s and what my returns would look like in each of those scenario’s!

I assumed in both scenario’s that over the period from now up until 2029 the company would reduce its EV by £300m.

At this point I think the EBIT is with high certainty going to be above £300m and very likely to be around the £300m to £350m mark. At that point I believe the IRR if the company provides decent share repurchases and rerates slightly higher to achieve an IRR of -3.7% to 22.7%, with the highest likely hood to be around the 10% mark due to the lower share repurchases.

Catalysts

The most obvious future catalyst is the one that has not really shown up in the numbers yet; the actual conversion of the new affordable housing “laws“ into orders, starts and revenue. There will be a point where SAHP allocations are confirmed and their partners will get proper funding visibility, and Vistry starts to see that translate into a genuine lift in Partner Funded activity through the second half of 2026 and into 2027.

The second catalyst is balance-sheet proof. If Vistry can actually get inventory down, reduce average debt and hit the net cash year-end target management keeps talking about, that would be a much more important signal than another housing-policy information from the government. Management has little influence on the economy or the government policy but can optimise the company to perform better.

On the external side, yes, a better UK economy, lower mortgage rates and a less miserable open-market backdrop would obviously help, but I do not think there is one giant future external event here that suddenly changes everything. I believe the coming years will be a period where the catalysts are slow and incremental.

Risks

The main risk here is that the business itself does not change enough. Vistry has already had the warning shot; the former South division issues exposed forecasting problems, and weak controls. Management says the control enhancements are now embedded and that the business has been simplified and reorganised, but the real risk is that the underlying habits do not change as management suggests.

That is the point I would hammer: does Vistry become a more boring, more disciplined, more predictable operator, or does it remain a company that keeps talking about cash release, margin expansion, and balance-sheet improvements while the actual numbers stay sticky? In that sense, the biggest risk to Vistry is not external at all. It is whether the new leadership team actually steps up and fixes things.

Cash generation keeps disappointing;

Vistry has been very clear that reducing inventory, lowering average debt and getting to net cash are top priorities for 2026. If inventory stays sticky and cash does not come through, then the market will start to question whether the Partnerships model is actually as capital-light in practice as it looks on paper.Partner-funded growth arrives slower than hoped;

Margins prove lower than the model implies;

Open market stays weak for longer;

Lower or no material share repurchases;

Debt-like liabilities remain more stubborn than bulls expect;

Even if year-end net debt improves, Vistry still has significant land creditors and provisions sitting in the background. If those do not come down, then the balance-sheet repair is far away, and the equity will probably continue to trade with a trust discount.

Conclusion

For now even with the relatively cheap valuation I cannot justify a position. I need to be more sure of (new) management to really be able to narrow down the future; this includes both share count and what new management plans to do with the release of assets and liabilities. If I buy a position in the future, I will be as transparent as possible and inform my readers of this!

I have tried to e-mail the CEO but a similar e-mail address of Greg bounced multiple times for Daniël. If I manage to speak to the CEO I will update all my readers with the relevant information. For now I will send the people from IR some additional questions, but as always I assume they will provide very little information which is not already public.

I think there is little downside due to valuation and more due to uncertainty, sector wide issues, and the general stock market downturn. To preserve wealth we investors must always minimise the downside!

Disclaimer!

I/we have no beneficial long position in the shares of Vistry Plc ($VTY.L). I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.

FY2025: 11,593 Partner Funded completions out of 15,658 total;

11,593/15,658 ≈ 74%.

Management has announced this 40% ROCE in more than one place, I linked the first official article that I could find: Link

Since ROCE = Operating profit / Average capital employed

Operating profit = revenue * operating margin

Capital turns = Revenue / average capital invested

In its 2024 annual report, Vistry highlights material JVs with L&Q at Beaulieu Park in Chelmsford, Taylor Wimpey at Greenwich Millennium Village in London, Riverside at Stanton Cross in Wellingborough, Metropolitan at Clapham Park in London, and Acton Gardens with L&Q. More recently, it formed a second JV with Latimer, Clarion’s development arm, at Sherford, and also launched the Hestia JV with Homes England.

(Where are companies allowed to build houses)

(How fast does the plan to build houses get approved)

(Build homes on previously developed land; such as industrial sights)

https://www.vistry.co.uk/media/press-releases/2026/vistry-group-plc-announces-its-full-year-results-year-ended-31

https://www.vistry.co.uk/~/media/Files/V/vistry-group-v1/results-and-presentations/2025/ara-2024-25-all-spreads-v1.pdf

https://www.insidermedia.com/news/midlands/partnership-brings-forward-more-than-150-rental-homes

https://www.insidermedia.com/news/midlands/partners-hail-progress-on-kenilworth-scheme

https://www.insidermedia.com/news/midlands/joint-venture-formed-to-create-2000-warwickshire-homes

346.9m shares in issue at the start of 2024

331.8m at the start of 2025 and

320.8m at 31 December 2025;

by year-end it had bought back 13.98m shares under the September 2024 programme, and the weighted average share count fell from 338.1m to 326.9m.

You can see that in Vistry’s own balance-sheet commentary:

2025 the company said average daily net debt was higher than it wanted because of delayed Partner Funded deals and slower inventory reduction;

2026 priorities were explicitly to reduce inventory, reduce average daily debt and get back to net cash. The debate is about how much cash is stuck in working capital and land at any point in time.

Shares outstanding went from 346.8m to 320.8m in a two-year time frame.