Ringmetall SE

Boring industry, great management and a 20%+ CAGR possibility!

Lately there have been a lot of chemical companies or chemical adjacent companies showing up on my screens and twitter feed. I decided to put them on a watch list and it has been sitting there for months and the number of names on that list kept on growing. I decided well I am supposed to be a generalist, a very curious one, so why not look into the chemical industry myself. I started out researching the entire industry and all the different type of chemical subindustries there are and if I tell you that the amount of things I read in 10 minutes which I did not understand and will probably never use or understand in my life; well it was more than I am willing to admit.

The second issue I found was that I was straying away from my core competency; small companies who are easily understood and who nobody cares to look at. Most of the chemical companies on my list were large conglomerates. The argument I often use is:

What do you as a tiny individual investor know, which the market, and therefore 10+ analysts are missing or do not know?

Most often people do not have an answer and if they do have an answer to it, it is a coin toss between either a non-argument or a very interesting investment thesis. I find that I must keep myself to this rule and ask myself the same question.

I came to the conclusion that this is not my ballpark, I will give you the tickers I had and then will continue with the stock of the day! Here are my tickers:

ASX:DGL

ACNT

EBR:AZE

AMS:IMCD

WSE:PRS

ETR:BNR

AMS:CRBN

As you can see I was very weighted towards European producers, mostly due to the fact that they are cheaper and a bit because I believe they are of higher quality. I am not long any of these, nor have I ever owned any of these stocks!

The company

The company I will be discussing in length today is Ringmetall SE, please do not think this is about Rheinmetall. Before I talk about what the company does, I believe management has laid it out very simple in their 2025 annual report:

“Ringmetall is a leading global specialty supplier to the packaging industry. Its product portfolio primarily consists of closure systems for industrial drums and inner liners for industrial packaging (so-called liners) in the chemical, pharmaceutical, and cosmetics industries, as well as for the food and beverage sector.”

Very simply said they make packaging materials, for us investors we will need a bit more nuance to understand the company fully!

Broadly said Ringmetall consists of two main business segments, Closure systems, which consists of industrial drum clamping rings, lids and seals and liner systems, which consists of industrial liners and bag in box systems.

In the image above we can see a split in the middle, the lefts side is the previously mentioned Closure systems, which are mostly done by Berger Global. The right side of the tree is the Liner system, which is operated under many different names and companies. On the right we can see Ringmetall services, that is just a group company which controls IT, Finance and other central tasks.

I will go more in depth, but this is a good general base of understanding for the company.

The history

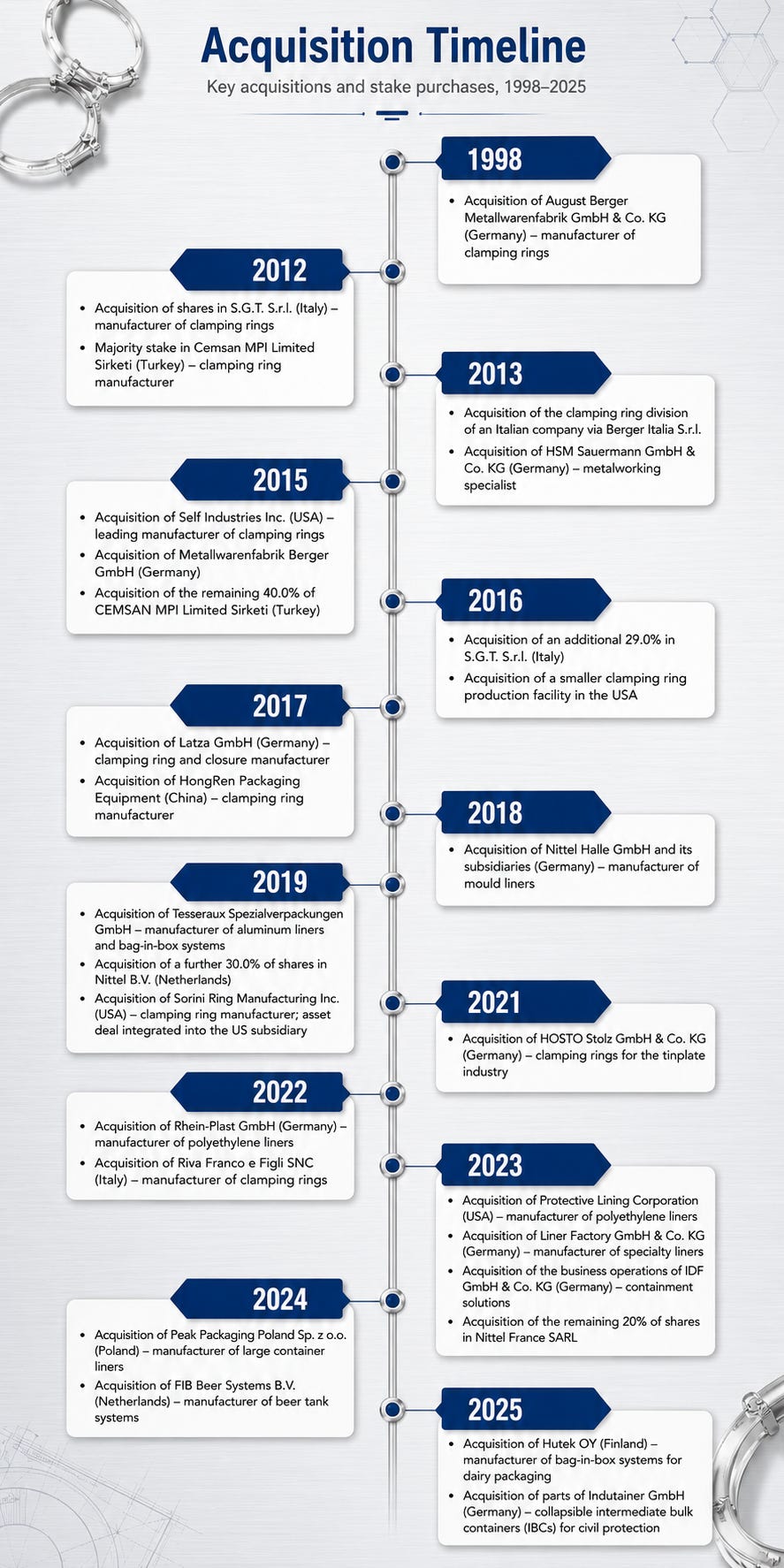

Normally I write up the history of the company, but I believe for a large part in previous write ups I have written too much and went away from the main goal of what I wanted to achieve in this part of my article. I have written the main points and asked ChatGPT to make an infographic out of my text, which can be seen below, I believe it is as valuable as what I could write, but it just reads better? I find reading a few hundred words for a company somebody is writing on quite boring, although useful.

Please let me know if you prefer this or the written piece! An answer could also be both; and go into more depth in the text!

Products

Most investors, myself included, do not spend their weekends thinking about industrial drums. Shocking, I know, but with Ringmetall you have to start there because it is the core of the business. This is not a company selling visible consumer products, so most of us investors do not know or recognise the company. It sells small, safety-critical components that sit on or inside industrial packaging. The customers relations are often deep and they have been buying these products for years (Source; my father-in-law sometimes buys similar products and hardly looks at competitors prices, just wants consistent and reliable products). These products are essential because the people buying them want to prevent leaking chemicals, contaminated food ingredients, and failed packaging tests.

I will be discussing Ringmetall through two divisions: Closure Systems and Liner.

Closure Systems is the old core: clamping rings, lids, gaskets, handles, closure units and other special components for industrial drums.

Liner is the newer growth platform: inner liners, drum liners, IBC liners (Intermediate Bulk container), container liners, protective covers, bag-in-box systems and beer tank liners.

Fun fact: The 2025 annual report says the group produces more than 2,500 clamping ring variants and more than 6,000 liner variants.

Clamping rings and closure systems

A clamping ring is the metal ring that closes an open-top industrial drum. This is often a steel, plastic or fibre drum with a removable lid. The lid sits on top of the drum, the clamping ring wraps around the lid and the drum rim, and then a lever, screw or fastener tightens the ring so the whole package seals properly.

These drums are used to transport chemicals, food ingredients, pharmaceuticals, powders, hazardous goods and other industrial materials. If the ring fails, the issue is not that someone has to order another €3 component. The issue is that the contents may spill, leak, contaminate, fail certification or become unusable. The ring is very cheap relative to the value of what it protects, but the failure cost can be very high. Ringmetall here competes both on price and reputation / quality, but the latter is of more importance!

The actual product they sell is most often the full closure system. Companies buy the ring, lid, gasket, handle, lever and closing unit to work smoothly together.

Management says Ringmetall is the global market leader in drum clamps, with a market share of well over 50%. It also says competitors in drum clamping rings are mainly regional suppliers with annual revenue in the single-digit millions.

I could talk as if I am really smart, but I am not so I googled what I should expect, consensus is that we should expect low to mid-single digit organic growth123. This number should not be taken as a fact, but I think it is generally correct. Drum clamps are a mature and niche business inside the broader drum market. Ringmetall’s 2018–2025 reported revenue growth in clamping rings/lids was only around 2% CAGR, and 2025 Closure Systems revenue actually fell 7.9% because of lower demand and currency effects.

Pipe / metal adjacencies

This is the less important part of Closure Systems. Ringmetall also makes pipe clamps, pipe hangers, pipe connections and wire or strip bent parts, mainly for automotive suppliers and household goods such as refrigerators and washing machines. This is a market which is very close to what Ringmetall already; has metal-forming know-how, machinery, engineering capability and production sites. So it can use some of that capacity and capabilities to produce adjacent products. This can be useful business, but it does not have the same obvious niche dominance as drum clamps. It is more exposed to general industrial production cycles in demand, which makes it less attractive.

I expected low growth here, probably around 0–3% organically. The focus is simply not on this product and it is on many different levels a different industry.

Industrial liners

A liner is the inner protective layer inside a drum, IBC or container. If the drum is the outer shell, the liner is the plastic inside shell. It stops the product from touching the container wall, which helps with: avoiding contamination, reduces cleaning needs, and makes it easier to reuse outer packaging.

Ringmetall’s Liner division includes moulded inliners, round-bottom bags, inner liners for drums, protective covers, IBC inner liners, container inner liners and mono- or multilayer films. All of the previous liners can be found on the Ringmetall website. The company also says recyclability is a key priority for the film packaging solutions.

The key difference versus clamping rings is that liners are more consumable. The drum or IBC can be reused, but the liner may and often must be replaced for hygiene, product purity, or contamination control. That makes the revenue more “recurring“ and less tied to new drum demand.

An example; a food manufacturer who can buy and use the same drum for multiple years, but needs to replace the liner each time the company ships new ingredients in their drum.

The market-share disclosure is also interesting. Management says Ringmetall has become the European market leader in inner liners for industrial drums and multi-component systems. It does not give an exact percentage, but it does say there are a few liner competitors of similar size. The issue I have here is that in my eyes this is a very low margin business, you simply make a plastic inside for a barrel or container. Yes, you need certain certification, but there is hardly a moat or a competitive advantage outside of price. Well that is what I believe….

Reported drum liner revenue grew from EUR 16.6m in 2019 to EUR 75.8m in 2025. Again, much of that came from acquisitions, but it shows the general direction of which the company is moving towards. Ringmetall has been buying its way into liners since 2019, including Nittel, Tesseraux, Rhein-Plast, Protective Lining Corporation, Liner Factory, IDF, Peak Packaging, Hutek and parts of Indutainer.

Expected organic growth should be medium, perhaps 4–8%. With acquisitions, it can obviously be much higher, but for now I am simply interested in the organic growth. The drivers are hygiene, contamination control, pharma and food safety, reusable outer packaging, circularity and the shift away from cleaning-heavy processes. I would also expect more consolidation since that is their strategy and we have seen this before in the clamping rings market.

Liquid packaging

Bag-in-box

Bag-in-box is a flexible bag inside a box, big surprise. It is used for liquids and pastes: dairy, food ingredients, chemicals, and beverages. The bag protects the liquid, the outer box gives the package strength, and the system reduces waste and makes transport more efficient. Ringmetall’s Liner division includes bag-in-box systems with filling volumes from 1 to 8,000 litres.

Beer tank

Beer tank liners are a more specific version of a bag-in-box type of liner. These are liners used inside large beer tanks. Ringmetall says it has achieved market-leading positions in several different niches, including beer tank liners. Not only that but with FIB beer systems they also produce the entire beer tank which can also be custom made (size).

Ringmetall has stated that the liner beverage packaging is dominated by large global corporations and that Ringmetall is only a relatively small supplier in that broader market.

Specialist hygiene & pharma packaging

This bucket includes protective covers, drum lid discs, and transfer bags. Similar to the beer tank liners these products have a very small niche but that can make the market very attractive. Since these are all very small individual markets, I feel like explaining what each product is a waste of your time.

Just assume it is a plastic bag in a box in some way, shape or form.

Customers

Ringmetall generated around a quarter of group revenue in 2025 from its two largest Industrial Packaging customers, both major international drum manufacturers. The rest was spread across several hundreds of smaller customers.

Ringmetall does not disclose the names of its largest clients in its annual report, but my online search research and previous research from other investors come to the same conclusion, the the two major drum-manufacturer customers are likely to be Greif and Mauser Packaging Solutions.

But it is also part of the industry they operate in. If the largest drum manufacturers are global and Ringmetall is the largest drum clamp supplier, the relationship will naturally be very concentrated. The important question is whether the customer has a credible reason to switch. I feel like this has a low likelihood, but not zero, because the component is and has been cheap for decades. These manufacturers do not want to get the blame when their clams fail, it is a very simple way of being able to shift away the blame. I will continue on the stickiness of their product in the competitive advantage search!

The industry

I would be lying if I said I understand the chemical industry.

I might even understand it less than the renewable diesel market, which is a dangerous thing to admit given I actually own that. But I do not think the Ringmetall thesis requires me to become a petrochemical analyst. Ringmetall is not producing ethylene, solvents, additives, or coating.

Ringmetall sells into the industrial packaging part of the product.

Its products are used to close, protect and line industrial drums. These containers are used across chemicals, pharmaceuticals, food, beverage, cosmetics and other industrial applications. So the question is not whether I can forecast every chemical sub-segment. The core question is whether industrial customers are producing, filling, storing and transporting enough product to need more packaging components. I believe that is something I should be able to do.

For the mature Closure Systems business, the answer is heavily tied to the chemical and industrial production cycle. For the Liner business, the picture is more mixed: it still has industrial exposure, but it also benefits from hygiene, contamination control, reusable packaging and food / pharma demand.

Why it is cyclical

The chemical industry is cyclical because chemicals are mostly intermediate inputs. They go into cars, construction, agriculture, etc. When industrial customers slow production, they buy fewer chemicals. When chemical producers sell less product, they need fewer drums, liners and closure systems.

The American Chemistry Council puts this quite neatly:

More than 80% of basic and specialty chemicals are consumed by the industrial sector. So chemical demand is basically a leveraged bet on industrial production4.

For Ringmetall, the demand looks something like this:

Weaker industrial demand → Lower chemical production →

→ Fewer drums filled → Lower demand for their products

In the post-Covid period (2021-2022), many industrial customers over-ordered because supply chains were previously unreliable and the availability of raw material was terrible. This increased demand and prices and led to Ringmetall having their highest revenue and profit ever (2022).

Subsequently demand slowed, supply chains went back to normal, and customers realised they had too much inventory and they started to de-stock (Simply means use all stock before purchasing new products and often keeping less stock). Thus, what happened was that orders fell harder than the underlying consumption. If a chemical producer sells 5% less product but also cuts inventory, its suppliers may see order volumes fall more than 5%.

This slower growth is expected to continue, although some sources even expect no growth in 2026 and very little beyond 2026…

Germany’s chemicals sales and production are expected to have dropped year on year in 2025, with no recovery expected in 2026, according to trade body VCI.5

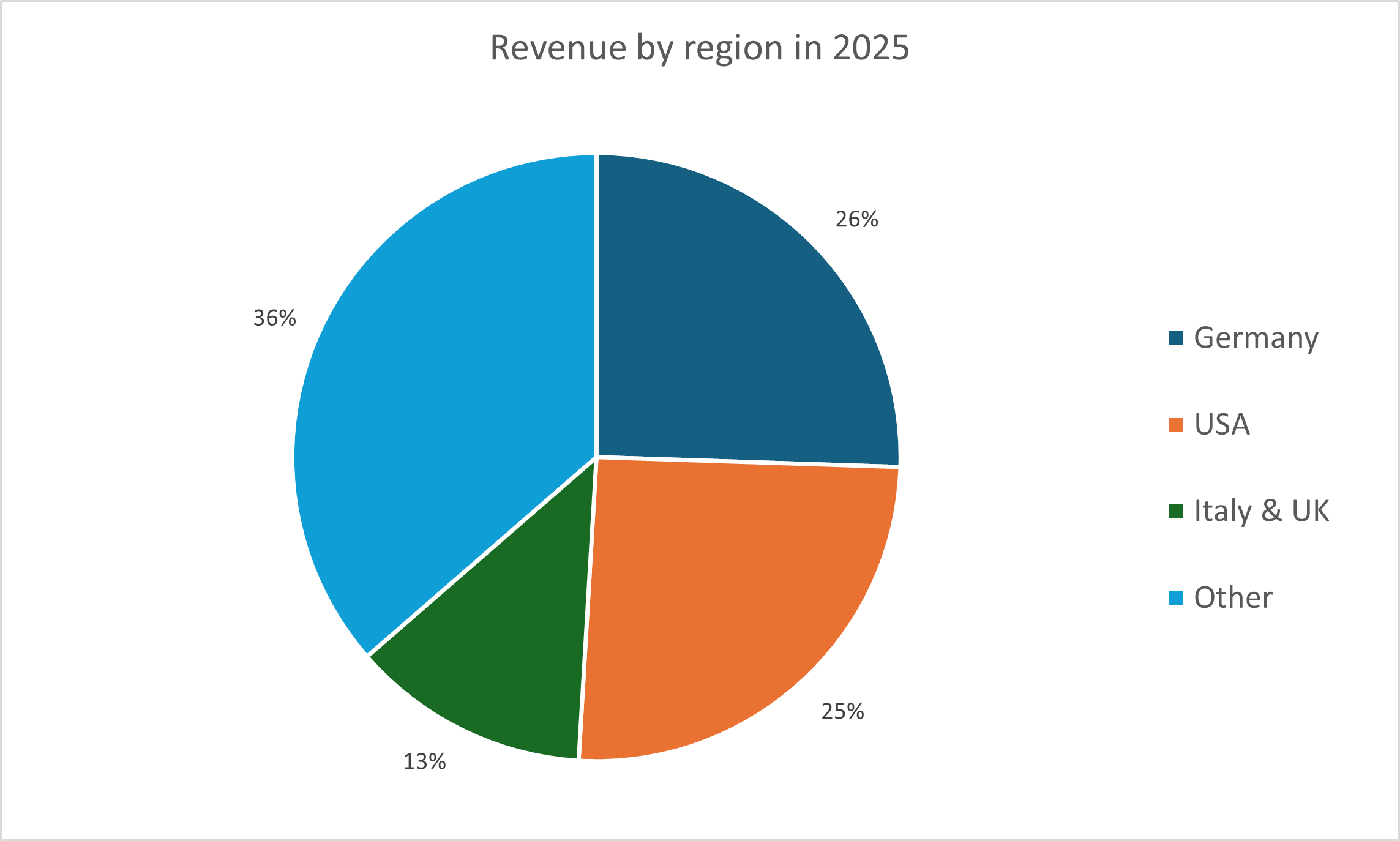

The positive news is that the company is diversified throughout the western world and not only tied to their home country of Germany:

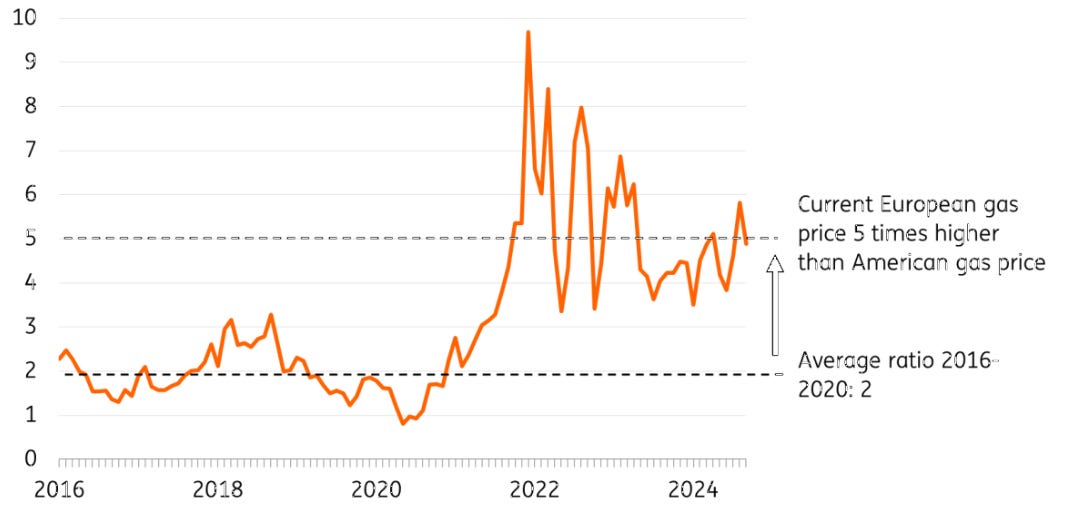

The longer-term issue is larger than just destocking, at this point Europe has a structural competitiveness problem. Cefic estimates Europe now has only 13% of the global chemical market versus China at 46%, while European gas prices remain around three times US levels. That means the recovery may be slower and more uneven than in a normal inventory cycle. For Ringmetall, that matters because the mature closure systems business is tied to chemical and industrial packaging volumes.6

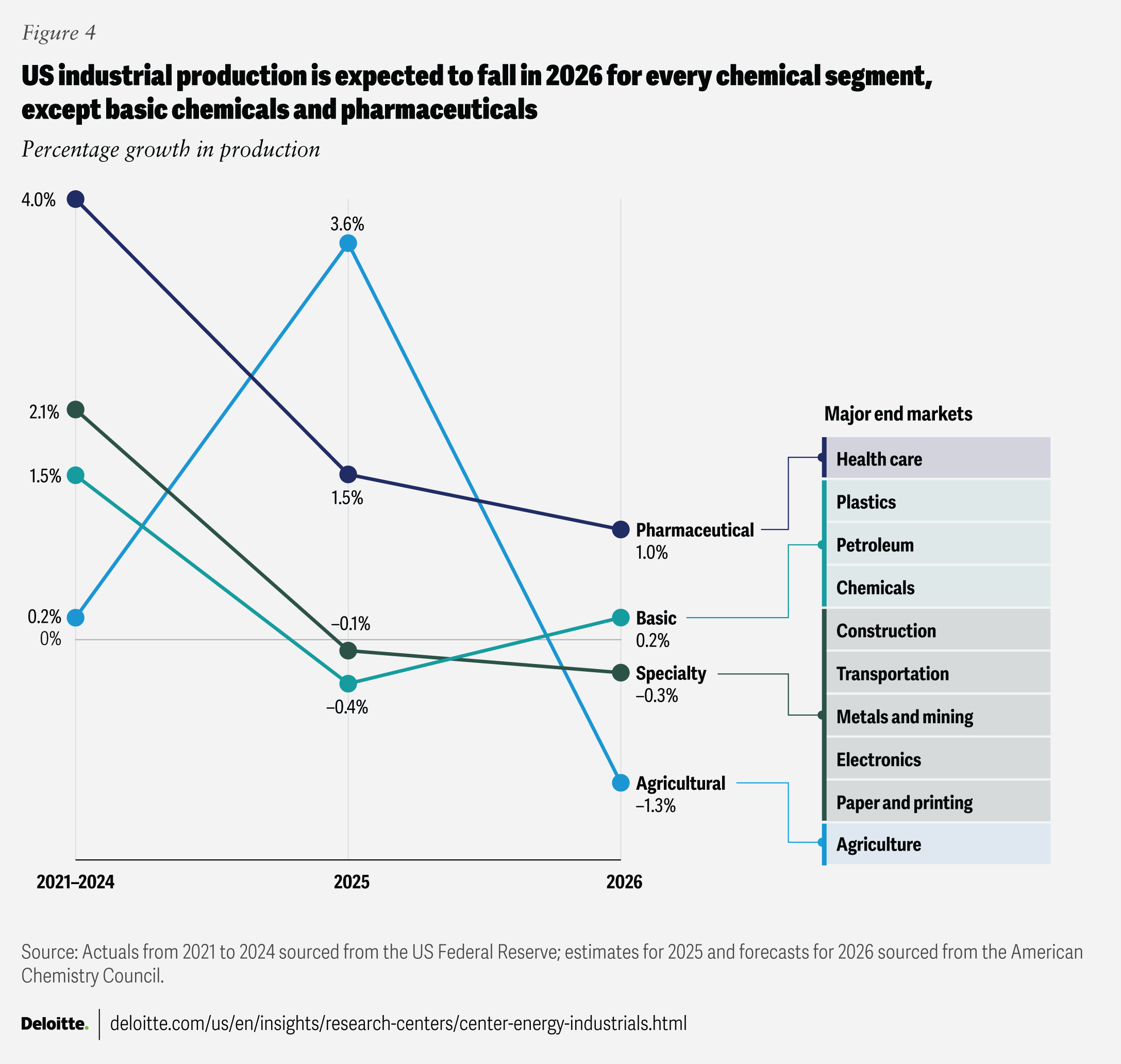

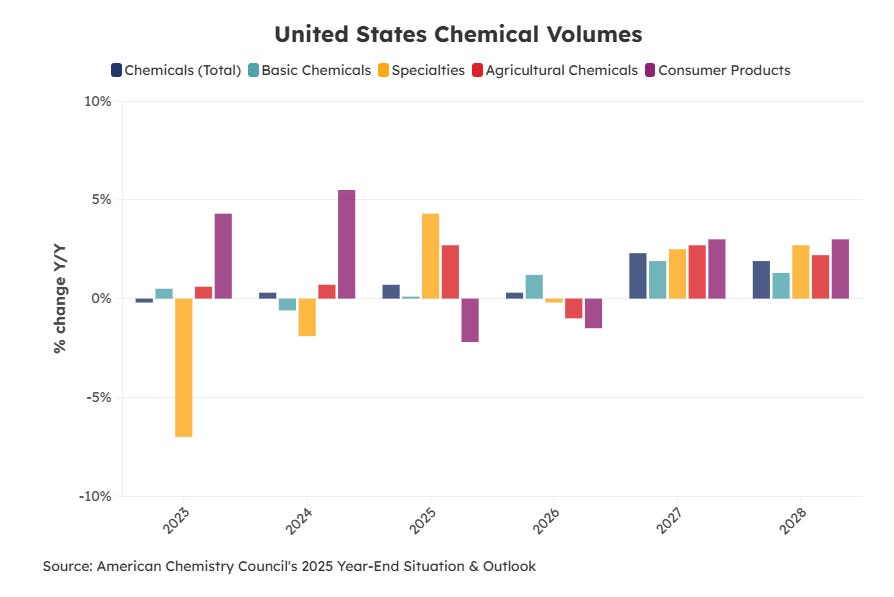

Positive news can be found for the North-American chemical segment which is expected to grow in 2026, I have included graphs and sources below:

To me it seems like the industry is probably late-cycle weak and not early-cycle strong, which some professionals do indicate78. Currently, I do not think the thesis should rely on a chemical recovery but it will be a slight tailwind in the coming 3 years.

As can be seen in the image from the ING analyst, the main reason for Europe becoming “un-competitive“, is the high relative gas price, which is a major input for chemical producers. This is relatively high both compared to US and Asian manufacturers, again since Ringmetall suplies most companies in the world this is not a large issue, but something to keep looking at.

What caused Ringmetall’s headwinds?

Ringmetall’s 2023–2025 headwinds came from several factors at the same time.

Chemical and industrial demand weakened, which reduced selling volumes.

Customers destocked, which reduced required volumes.

Raw material prices fell, which reduced prices. Ringmetall passes through raw material costs in parts of the business, so decreasing steel or input prices can reduce reported revenue.

Europe’s chemical industry is structurally weak. Europe has high energy costs, weak capacity utilisation, China competition, and a less attractive manufacturing base than it used to have.

Higher European natural gas prices since the invasion of Ukraine, which has caused input costs to go up in Europe, while similar US chemical producers did not experience this.

So to summarise this;

I believe we are currently in the late cycle down-turn, not in the early up-cycle;

Europe is still facing headwinds, expect zero or little growth;

The US chemical market is expected to grow about 3%.

M&A

Similar to the other parts, I have also included a time-line of all their historic acquisitions, again in an inphograpic. Below it I will discuss the significant and interesting acquisitions.

Ringmetall has roughly three different acquisition strategies;

Consolidation, buying companies in the same niche it already dominates or has large market share, usually clamping rings and closure systems, then integrating them into the existing platform.

Adjacent product expansion, buying products that are used in the same “transaction“ with their customers, such as lids, seals, and fasteners. Same customer, who needs someone else their product to complete their own product.

New platform, buying into a new but related product category. This is what management did with Liner, starting with Nittel in 2018 and then building around it. Examples of acquisitions are: Tesseraux, and Rhein-Plast.

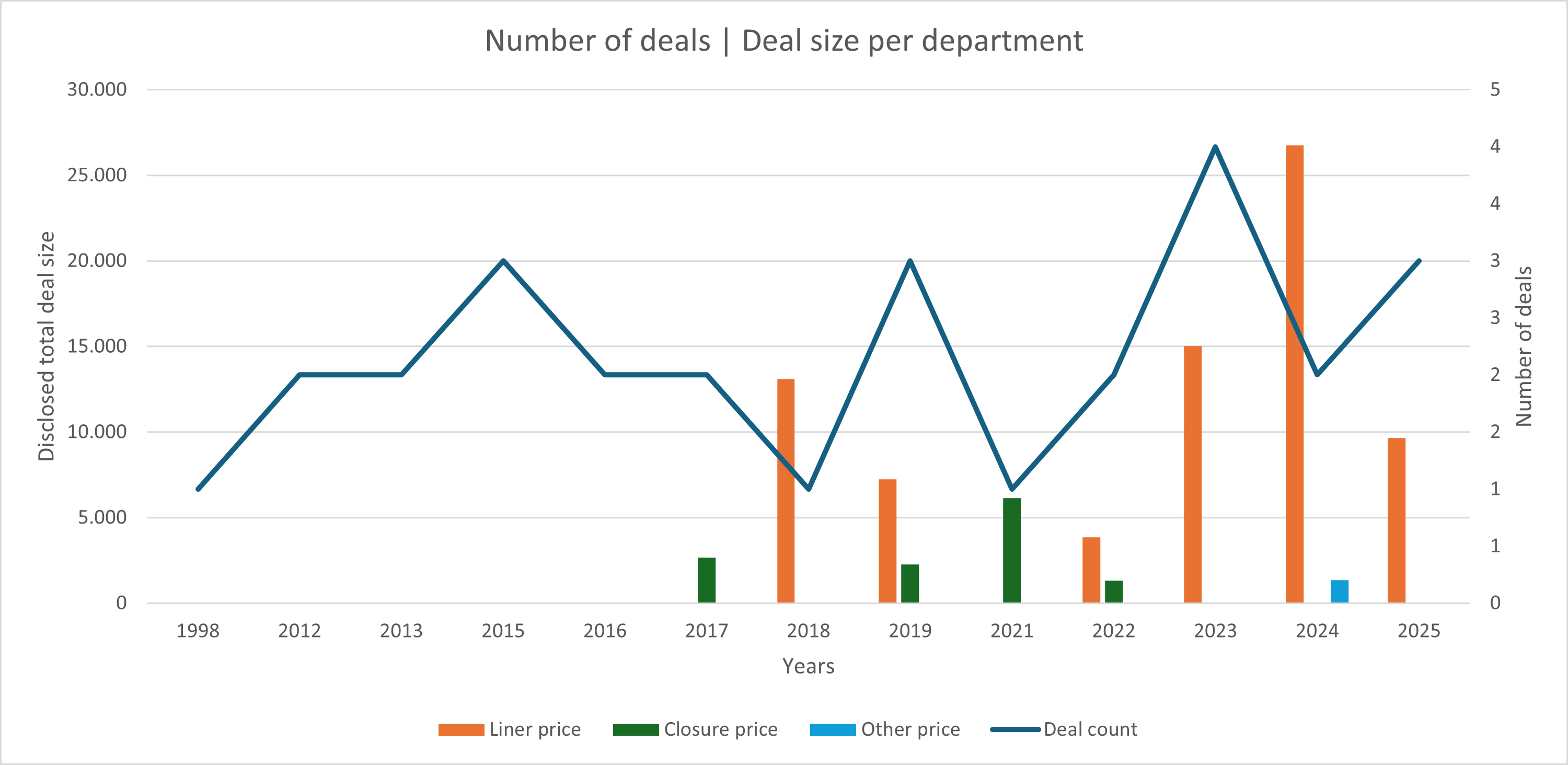

Below I have illustrated the total number of deal per year (line) and the total disclosed purchase price paid per division, which is significantly different compared to what they actually have spend, because they do not disclose what they have paid for all of their acquisitions!

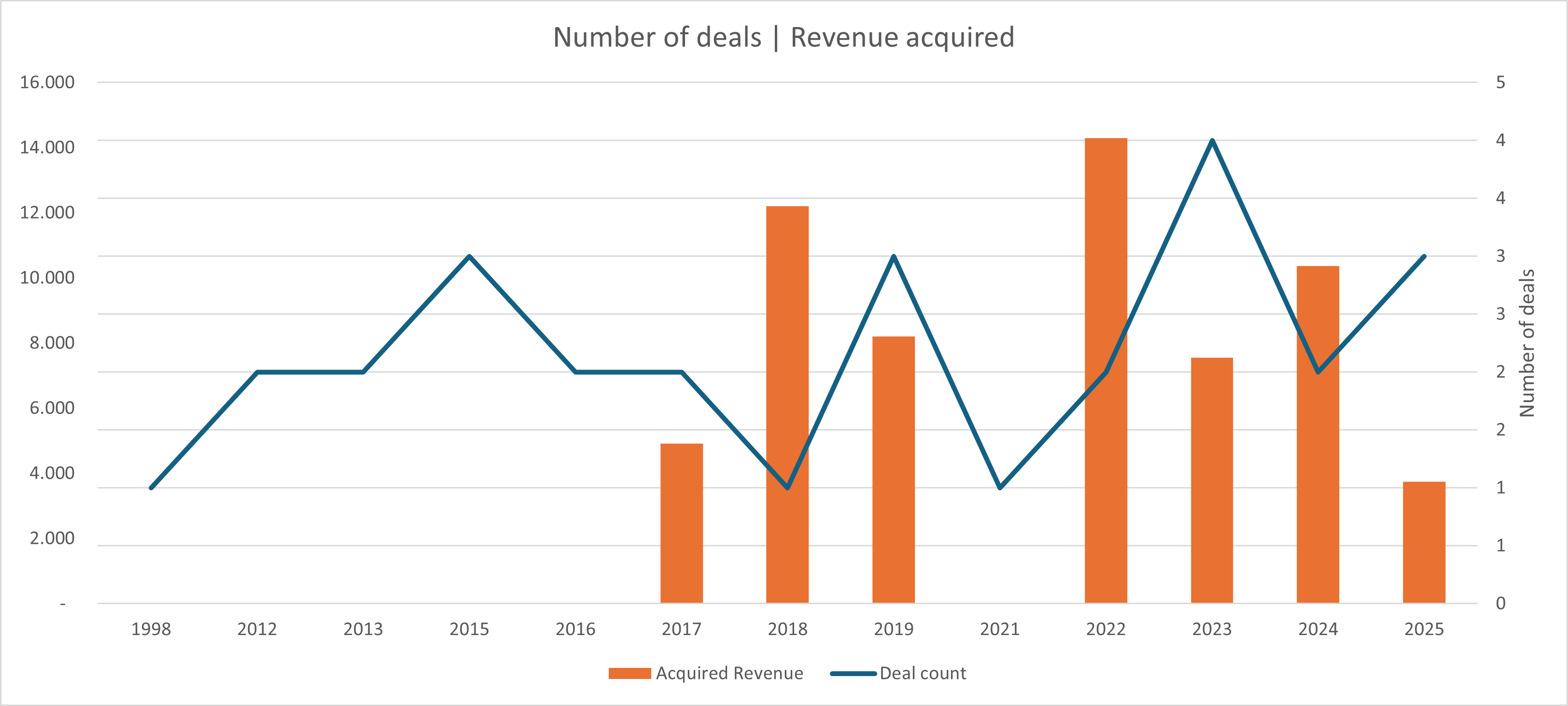

The total disclosed amount has mostly gone to the liner business, which is as I previously explained their growth engine. I hope they disclose more data in the coming periods, such as revenue, expected synergies and earnings. I do understand that in a cyclic market, where management does not have all the cards in thier hands, it can be hard to talk about the earnings instead of the revenue which most recently is often being disclosed, such as can be seen in the graph below:

I would like them to disclose an IRR or a different metric on which they base their acquisitions, but I have not found it. For now in 2026 they have bought two companies: Makplast9 and New England Plastics their Thermoforming division10. Both these companies are within the liner business and the companies generate mid and high single-digits amount of revenue, so I would assume in the €12m - €14m range!

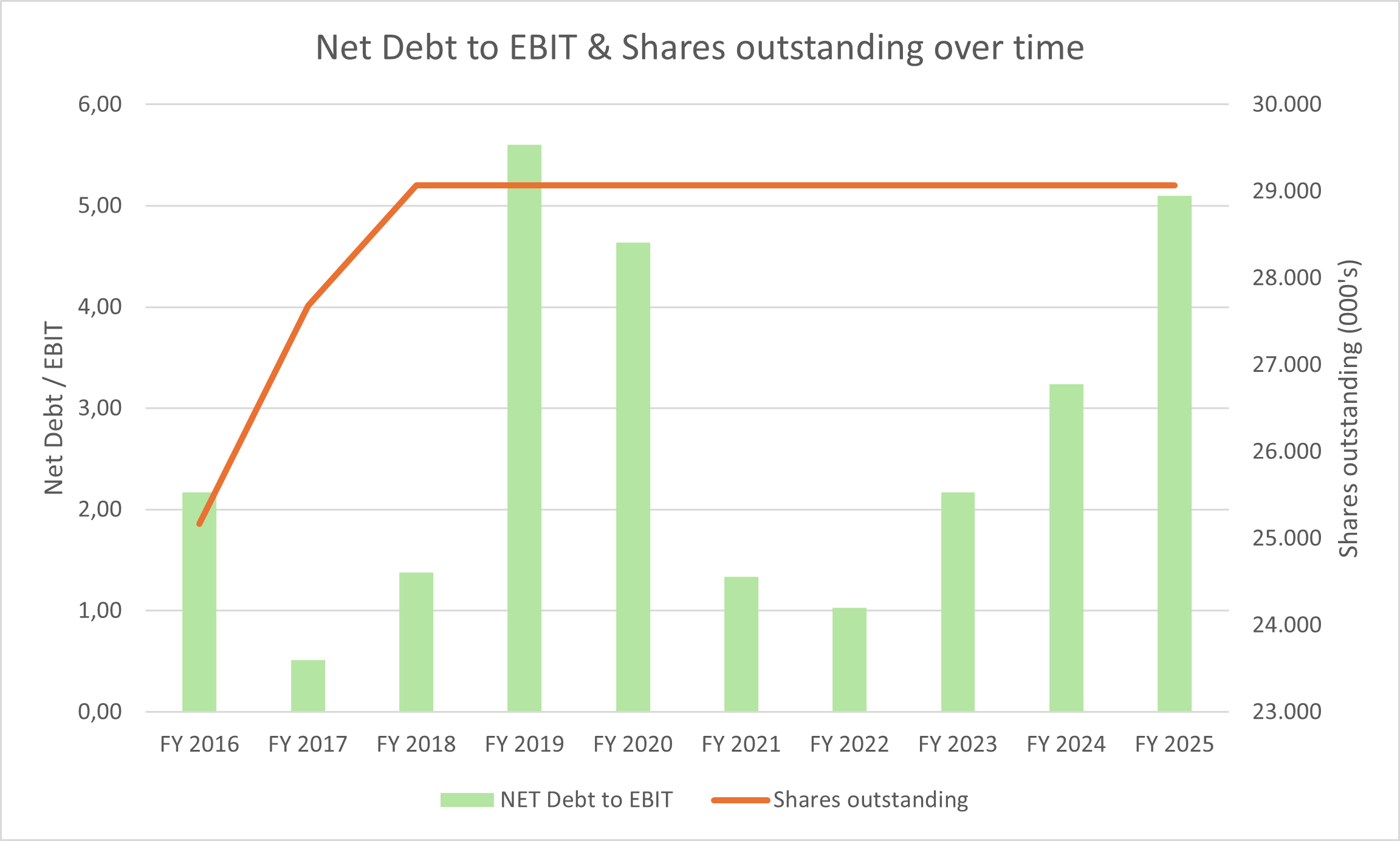

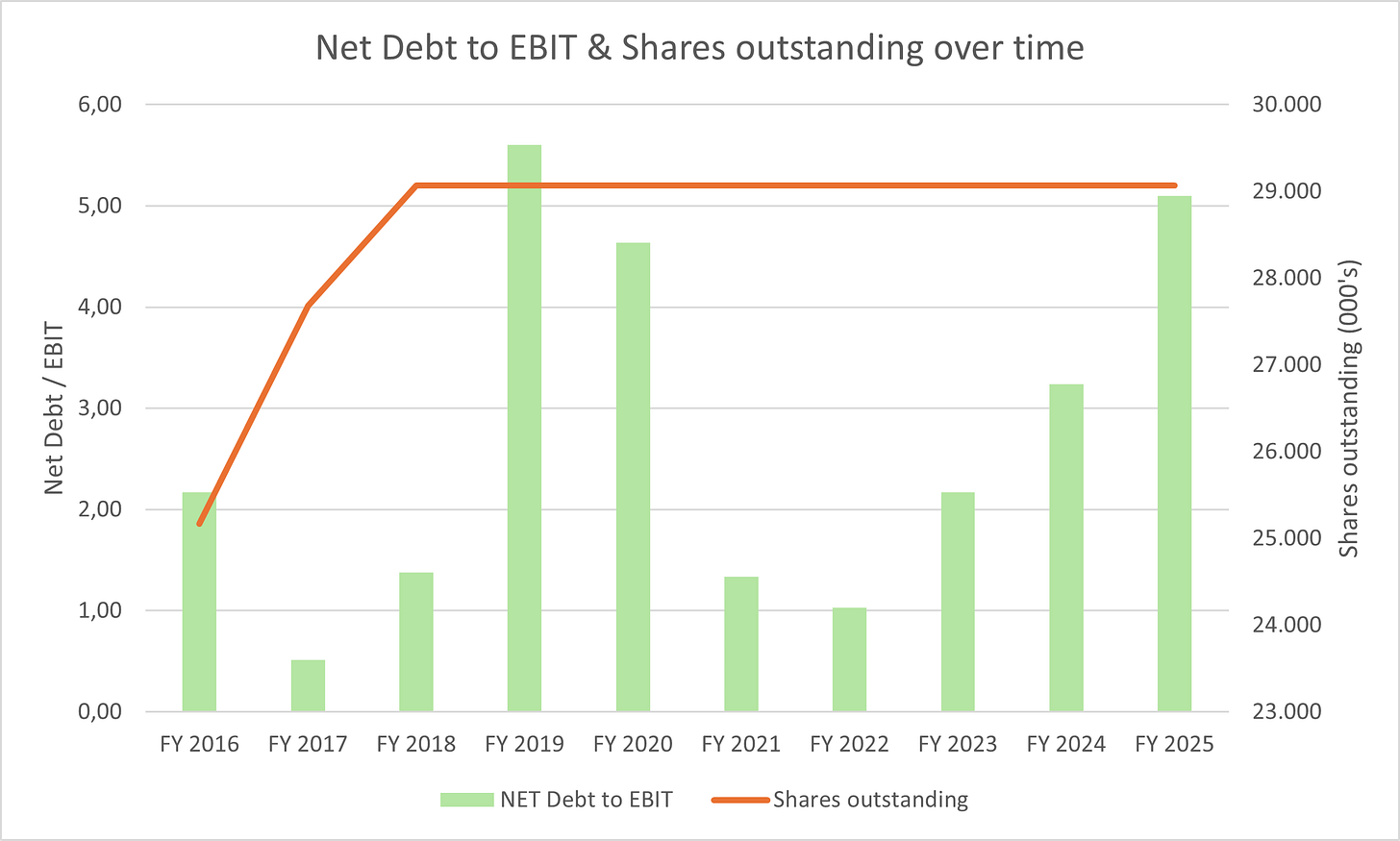

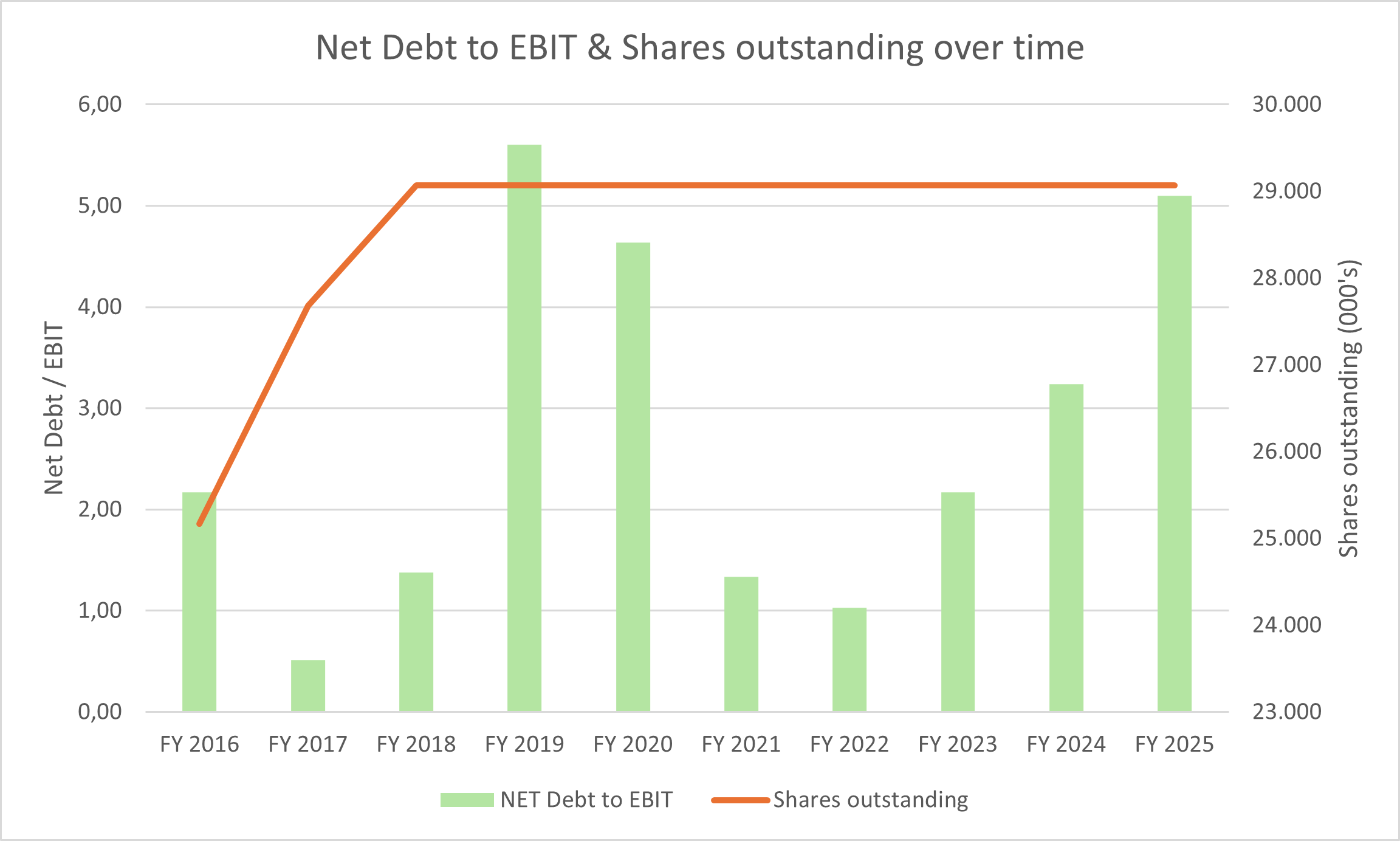

What we can see over time is the change in shares outstanding and the Net Debt they have compared to their EBIT.

Management

In the previous chapters I have discussed how Ringmetall operates in a very hard and competitive cyclical industry, which in Europe is facing a lot of hardships. Ringmetall also does quite a lot of M&A, where we are not able to see what the returns are.

Question: So how do we mitigate this principal-agent problem?

Management can always tell you acquisitions are strategic and/or synergistic, which we investors should always treat with a grain of salt. Since, these are usually the same words used right before goodwill gets impaired three years later.

Answer: By having reliable and trustworthy management!

For Ringmetall, the answer is management alignment and their lofty track record.

The company has a two-person Management Board: Christoph Petri and Konstantin Winterstein. There is no separate CFO in the normal Anglo-Saxon sense. Petri is the CEO / Spokesman and also responsible for finance, investor relations, strategy, sales and marketing. Winterstein is the operational / technical counterpart, responsible for production, technology, HR, IT and operational investment management.

CEO - Christoph Petri

I believe Christoph is the man responsible for the capital allocation.

He studied business administration at the University of Nuremberg and the University of Sydney, graduating in 2006. He then started his career at a consulting and investment company focused on mid-sized businesses. He joined Ringmetall’s Management Board in 2011 and is now responsible for strategic investment management, finance, investor relations, sales and marketing.11

This means he has overseen the acquisition of the industrial packaging divisions, the acquisition-driven build-out of Closure Systems, the entry into Liners, and the sale of Industrial Handling. I would like to write that these have all been brilliant acquisitions and great capital allocation decisions, I simply cannot. What I can say is that they have all been value accretive and revenue has mostly grown through acquisitions, while share count has stayed at the same level for the past years. Relative debt has increased but again there we can see the cyclicality!

A 2018 MainFirst stock initiation report described Petri as having experience in corporate consulting and private equity. They also noted that he had previously been an M&A adviser to H.P.I. Holding (previous Ringmetall company), where he built know-how about the industrial packaging market.

CFO - Konstantin Winterstein

Konstantin Winterstein is the “manager“ operations, who focusses more on the day-to-day operations of the business.

He studied mechanical engineering at TU Darmstadt and TU Berlin, graduated in 1996, and later received an MBA from INSEAD. From 1997 to 2014 he held various roles at BMW Group. He joined Ringmetall’s Management Board in 2014 and is responsible for operational investment management, HR, IT, technology and production.12

The company’s advantage is not just buying small businesses, it is also very much production know-how and expertise, knowing how to do it is one thing but perfecting the craft is something else! Winterstein’s background at both BMW and his study are industrial and operational.

The same MainFirst report described Winterstein as responsible for technology, production and operational investment management, and said he brought many years of experience from the automotive and automotive supply industries.

Ownership and pay

Ringmetall does not disclose a the number of shares held per individual management board member. What we do know is this that in the 2025 annual report is stated that each Management Board member holds more than 10% of the voting rights, and since total shares outstanding are 29,069,040, both the CEO and CFO own or control at least 2.91m shares. Even better news is from the 2022 annual report where Ringmetall stated that the management board held 59,0% of the voting shares13.

I have tried to make a decent estimate based on the number of shares they had in 2022, but it was not clear how much was done by related parties or who owned what amount of shares. What I do know is that Petri has bought nearly half a million worth of shares (Twice his base salary) in 2025Q4, at a share price of €2.80.

Numeration

The numeration is build up out of a few things;

Base salary, in 2024, there was no detailed split in 2025, each management board member received a base salary of €310k. I assume this is either inflation adjusted or slightly above this for 2026.

Short Term Incentive (STI), is as the name says a short term bonus plan, which is paid after year end. This is based on both EBITDA and Revenue targets, which the company sets but does not disclose. The divide between EBITDA and Revenue is 50/50. In 2024 the total amount paid per person was €113k, this is paid in cash not shares!

Long Term Incentive (LTI), very similar to the STI, but over a 3-year period on which the targets are based. These targets are based on both EPS-growth and ROCE, I will show ROCE development in a later stage of the write-up! In 2024 the total amount paid per person was €225k, this is paid in cash not shares!

In total management received a total pay in 2024 of €648k and in 2025 the total pay was €614k. But there is a 4th way they get paid… Dividends, since they own quite a few shares management also receives quite a bit of cash in dividends.

Dividend per share has remained stable over the past 7 years. Since management owns at least 60% of the outstanding shares and we simply assume that this is split 50/50. The management board receives 4x their annual salary in dividends; €872k.

External thoughts

MainFirst first initiated a stock report on Ringmetall in 2018 with an Outperform rating and called it a “hidden champion”. MainFirst focused on the same two things I care about: management ownership and their M&A execution. The report said M&A was central to Ringmetall’s growth strategy, which I agree with and that management had built a strong M&A track record, and that Ringmetall’s reputation made it a preferred partner for family-owned mid-sized companies looking to sell.

To the point, I no longer believe MainFirst exists and has not covered Ringmetall in a while. I have seen no evidence that they changed their opinion on either the company or management,

Management interview

The best interview I found is an older 2018 Nebenwerte Journal interview14 with Petri and Winterstein. It is useful because it shows how long the M&A mindset has been in place within management and how they think about certain topics such as: competitive advantage and their product lines / vision. I have added a few pieces of the interview throughout the write-up, but please if you are interested in the company please go read it!

The Supervisory Board

The Supervisory Board is unusually relevant here because Ringmetall is acquisition-heavy. People who have little to do with M&A might not know but nearly all acquisitions have to go past the supervisory board, to have an independent group of experts judge the acquisition. I want people operating the M&A who understand M&A, similarly how CSU and Topicus have their own supervisory board who approve and question each and every acquisition!

The board is made up out of the following people;

Klaus Jaenecke, who is chairman and has a background in business administration, investment banking and M&A. He worked at Kleinwort Benson and Goldman Sachs, then set up his own M&A advisory business in Munich in 1991.

Markus Wenner, who is deputy chairman and is a lawyer by profession. He started at Clifford Chance in M&A and corporate finance, then worked as an investment manager for GSM Industries. Today he is managing partner of GCI Management Consulting, focused on consulting and investing in mid-sized businesses.

Ralph Heuwing is probably the most impressive board CV. He studied mechanical engineering at RWTH Aachen and MIT, earned an MBA from INSEAD, became a partner at BCG, then CFO of Dürr, then CFO of Knorr-Bremse, where he was involved in one of Europe’s largest IPOs in 2018. Since 2020 he has been Partner and Head of DACH at PAI Partners.

Monika Dussen adds turnaround and transformation experience. She studied industrial engineering and has worked on transformation processes in German SMEs, later supporting restructuring and realignment projects both as adviser and interim C-level executive. She is now a partner at Struktur Management Partner, a turnaround-management consultancy.

The board also seems active enough. In 2025, the Supervisory Board held four regular meetings, all members attended, and the board visited US locations in Chicago, Birmingham and New York together with management. It also discussed acquisition strategy, organisational structure, risk management, the 2026 budget and medium-term plans for the company.

That is an excellent board for this Ringmetall, especially for the size (Market cap). Although I do not know them, their CV and experience is something we can only admire. However, this does not guarantee good governance, but it does suggests that the board is not asleep at the wheel.

Conclusion

Konstantin is 57 years old and Petri is either 44 or 45. That means they most likely have a decade together running the company. I feel alignment is possibly the most important point in these smaller companies and management owns a large chunk and has been buying shares!

I am comfortable with both Ringmetall their management board as well as their supervisory board. Petri and Winterstein seem aligned, are very experienced, and seem highly consistent. They are not perfect, and the lack of acquisition-level return disclosure means we still have to trust them more than I would ideally like. But the track record, ownership, board quality and strategic consistency suggest they are good stewards of capital.

Competitive advantage

A good question to ask yourself when investing in a company is: Why would a competitor not take over Ringmetall their current markets or outcompete their entire product range?

Well I believe their competitive advantage to be five-fold:

Product variation; Ringmetall makes thousands of different clamping ring variants. Different drum materials, sizes, lid profiles, wall thicknesses, and also different customer requirements. Since they have a number of very large customers, they need to be able to to this at significant scale.

Regulation and certification; Industrial packaging often has to meet safety and transport requirements, especially for hazardous or sensitive goods. Once a drum system is certified, the change of components come with extra costs and down time, both of which are terrible for the customer.

Machinery; Ringmetall says production relies heavily on in-house or highly customised machinery. The company has also been rolling out a newer generation of clamping ring machines to improve changeover times, speed, accuracy and waste. Which allows them to be cheaper and more efficient compared to the competition, if there is any.

Knowledge; Due to the operating time horizon, which is nearly 30 years, Ringmetall can be assumed to have a very large and knowledgeable employee base which has a lot of experience. This has been discussed previously.

Logistics; Customers want short lead times and consistent quality. This sector is very cyclical and being a large drum manufacturer, the supplier who can deliver across regions, with the right certificates, on time is worth something.

This is all together is the competitive advantage the company has.

Managements view

Petri: Of course the product looks very simple. In reality, however, there is much more technical know-how behind it than one might assume at first glance. There is no single standard clamping ring. We manufacture more than 2,000 different variants, starting from batch size one all the way to mass products.

Winterstein: Suppose the chemical group BASF wants to transport a liquid product in a drum that must not leak under any circumstances, even if dropped from a height of two meters, because the liquid is classified as hazardous goods.

With this requirement, BASF turns to its drum manufacturer, and that manufacturer in turn comes to us when it comes to the closure system. In such a case, we develop an individual solution together with the drum manufacturer for its customer.

After that, no third party can easily push us aside with a cheaper offer. The drum and closure system form one packaging unit approved by the customer, BASF. This means that a new clamping ring would first have to be UN-certified. That is in neither the drum manufacturer’s interest nor its customer’s interest.

Why do drum manufacturers not produce clamping rings themselves?

Petri: They used to do so. However, because of the relatively low value, production was outsourced to suppliers. These suppliers are our target companies, which we want to acquire or already have acquired.

This also explains why the business is rather regional. Not least because of transport costs in relation to product value, suppliers have located themselves close to drum manufacturers. The German centre is in Berg near Karlsruhe. That is not far from Ludwigshafen, where BASF is based.

I think the commentary management gave in the article I have quoted above, although dated, is still highly relevant and portrays confidence.

Fun intermezzo

I was looking up the stock graph in Google finance since I quite like the way the graphs look and I found the following:

Which is a very decent high-over view of the company. I might use this more often for a quick scan!

Valuation

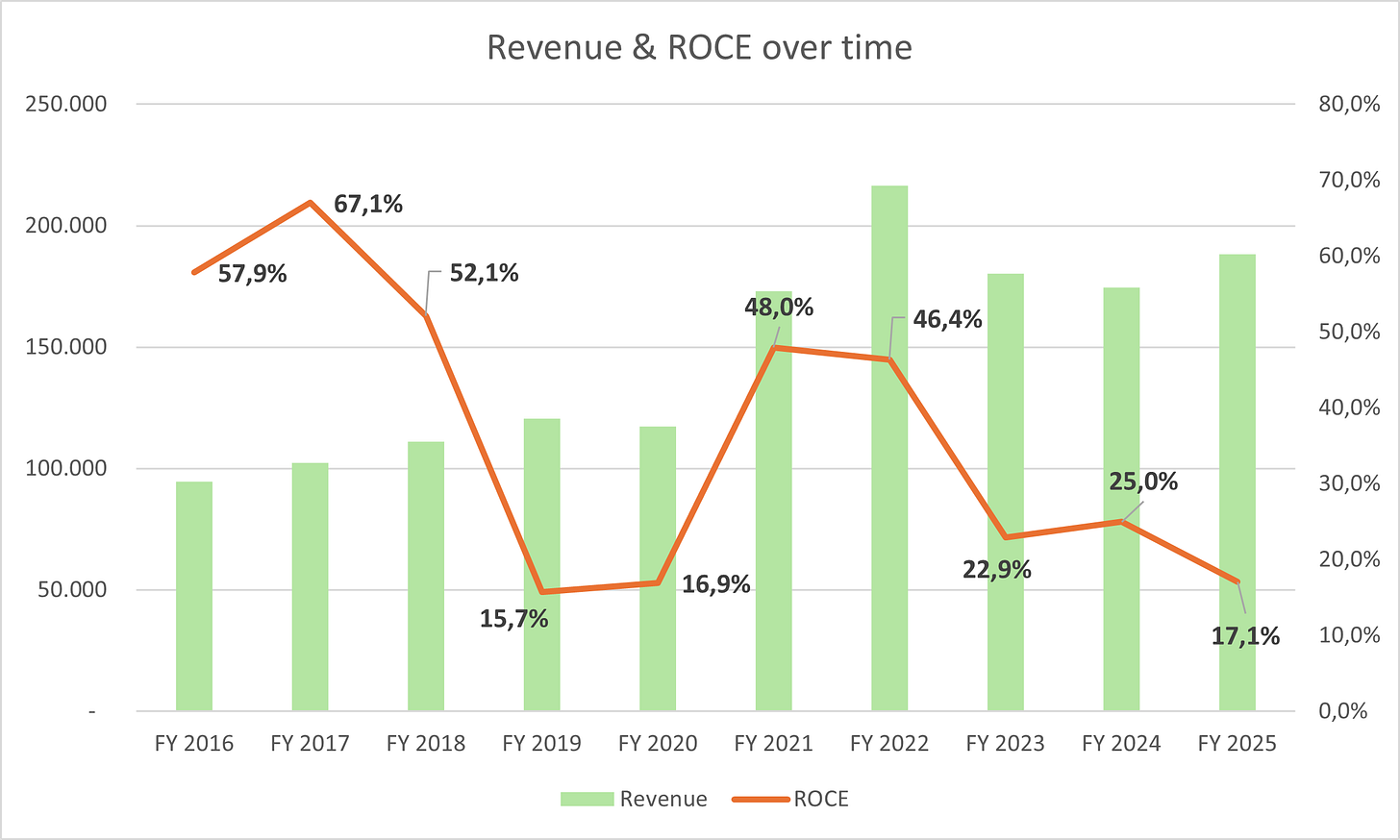

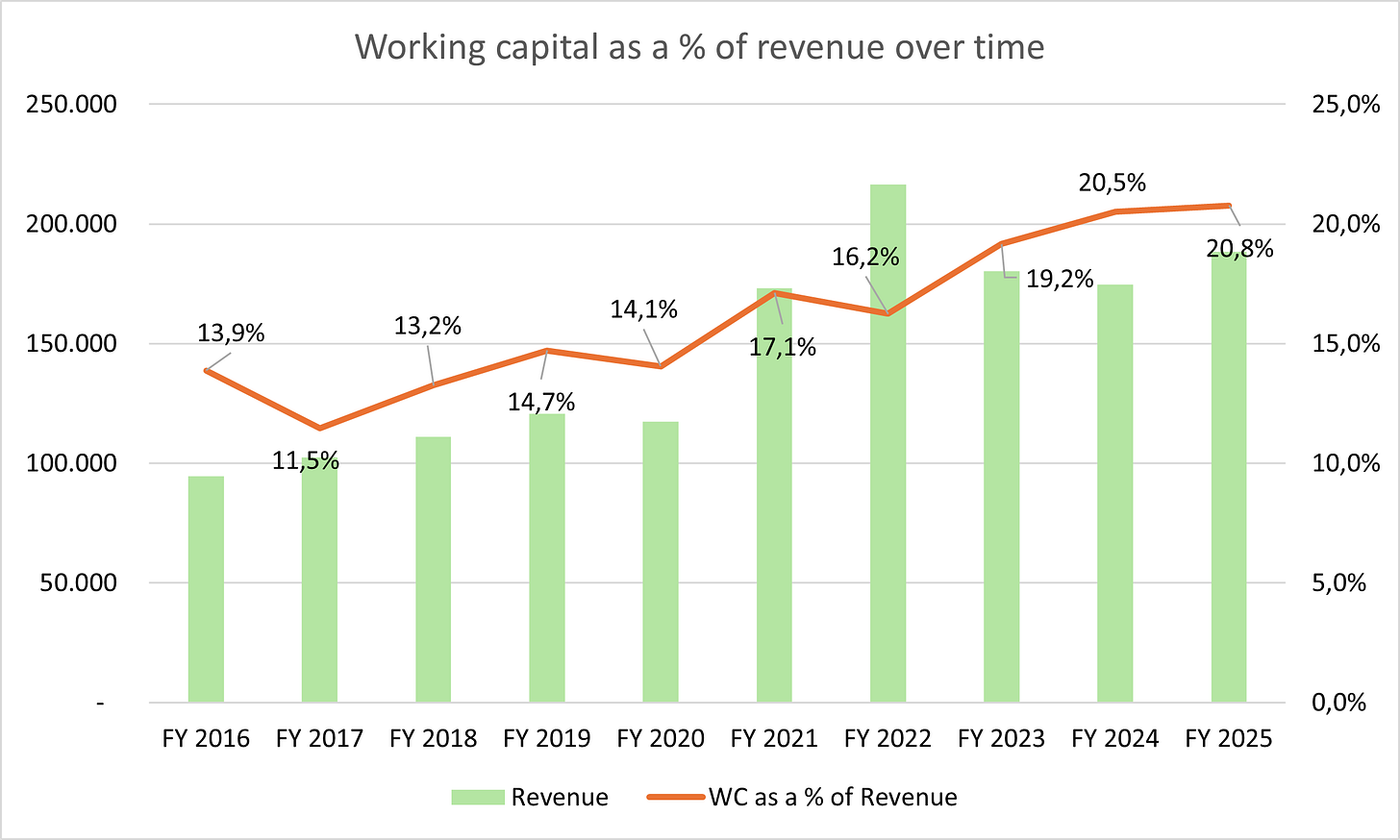

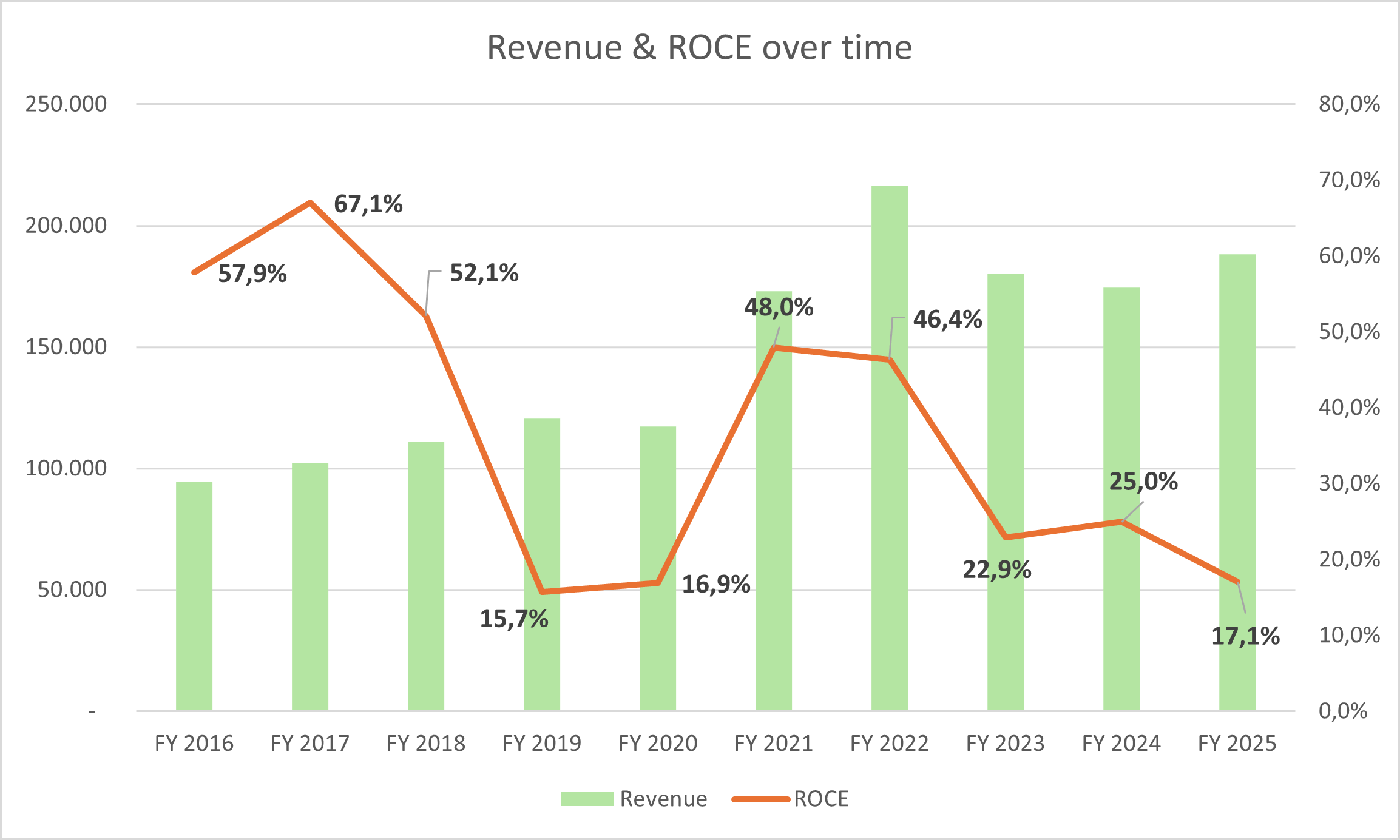

Before I value the company I want to ensure that I have the right KPIs to track the performance of the business. As probably previously explained, tracking these KPIs each half year is a quick way of gauging how the business has performed. These KPIs can also be backward looking, by first determining the KPIs and then seeing how the business performed in certain years on those KPIs we can even make a certain cyclical prediction for Ringmetall…

KPIs

ROCE measures how much EBIT Ringmetall generates on the operating capital tied up in the business. Ringmetall’s own definition is:

EBIT / (PPE + trade receivables − trade payables)

Net Debt to EBIT which measures balance sheet risk versus operating profit. I calculate it as financial liabilities including leases minus cash, divided by EBIT..

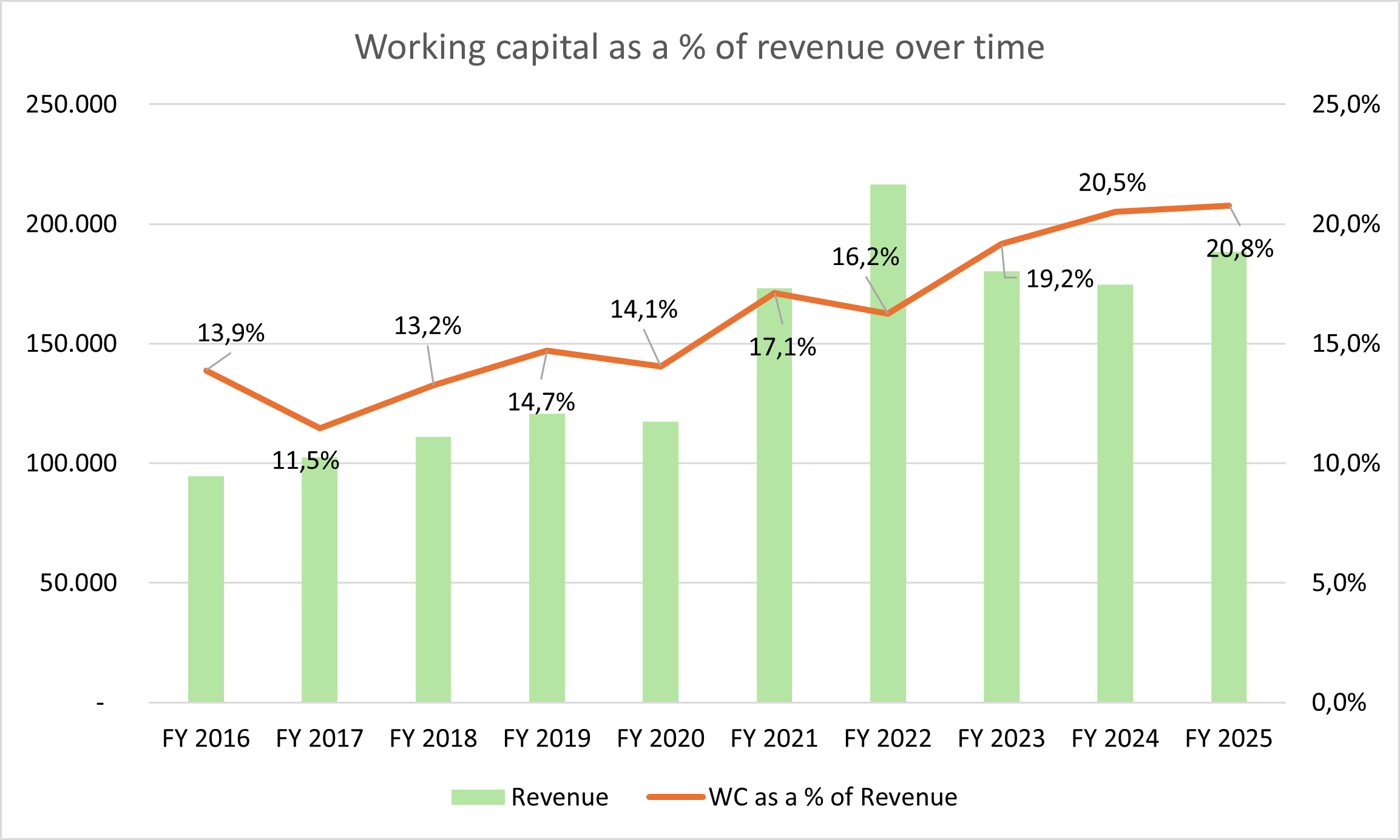

Working capital as a % of revenue measures how much cash is tied up in the business. I find this important since Ringmetall has a lot of money tied up in inventory, receivables and payables.

Operating working capital = inventories + trade receivables + contract assets + other current assets − trade payables − other current liabilities

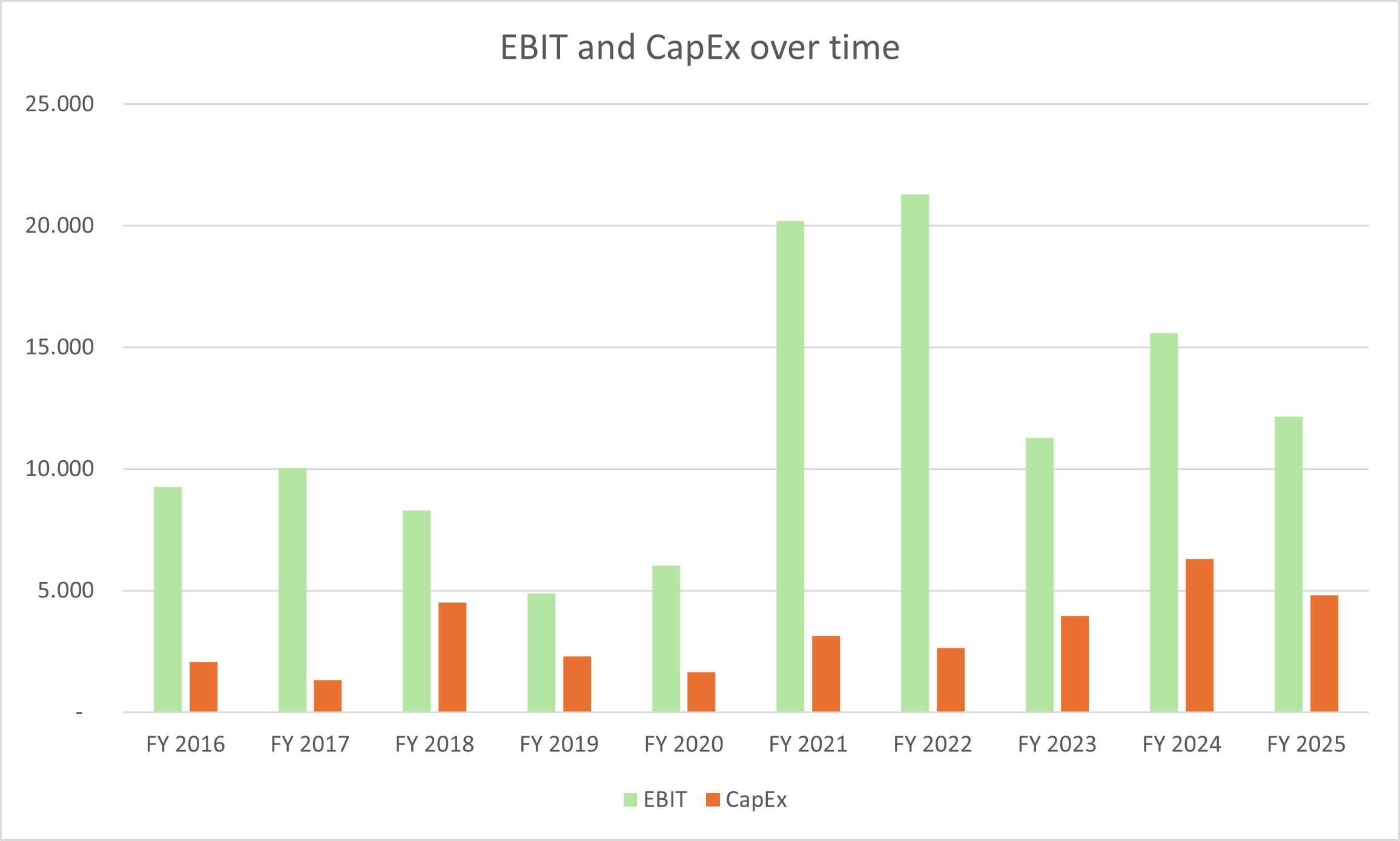

Free Cash Flow before acquisitions this shows the cash generation of the existing business before M&A spend. Calculated as operating cash flow (EBIT) minus maintenance CapEx, before acquisition cash outflows.

KPI conclusion

The ROCE graph and the Net Debt to EBIT both show that EBIT is lower, similar to the FCF before acquisitions. This is either due to the moment in the cycle which we are in or that the business is declining, I think it is the former and due to the length of data I have provided we can all see that this has happened before and better times are ahead! The only concern I have is the ever increasing working capital which is tied up within the business, perhaps something to keep looking at!

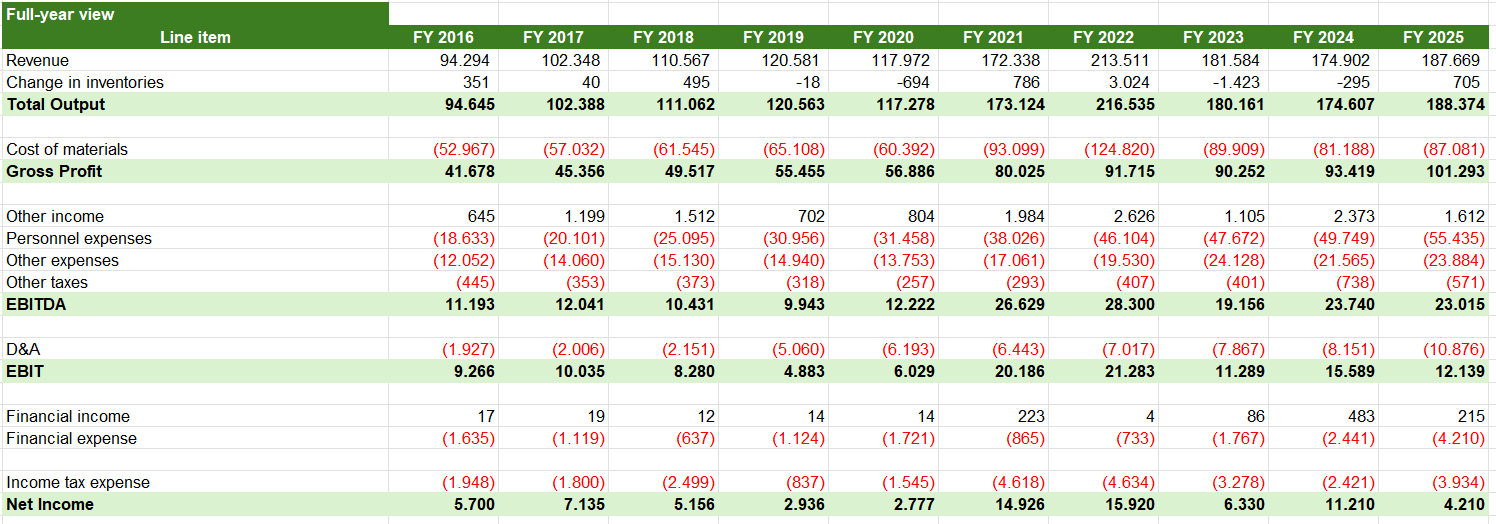

P&L and balance sheet overview

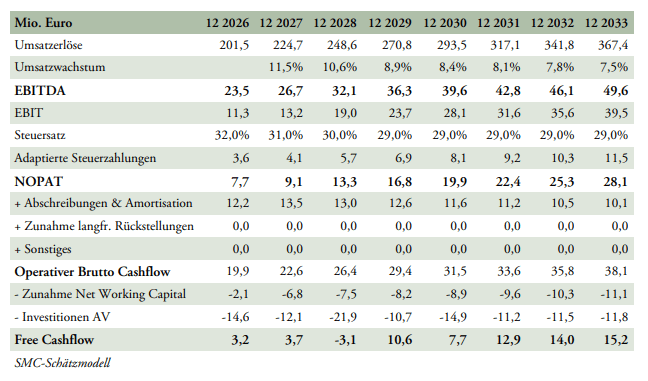

Below you can find the P&L per year:

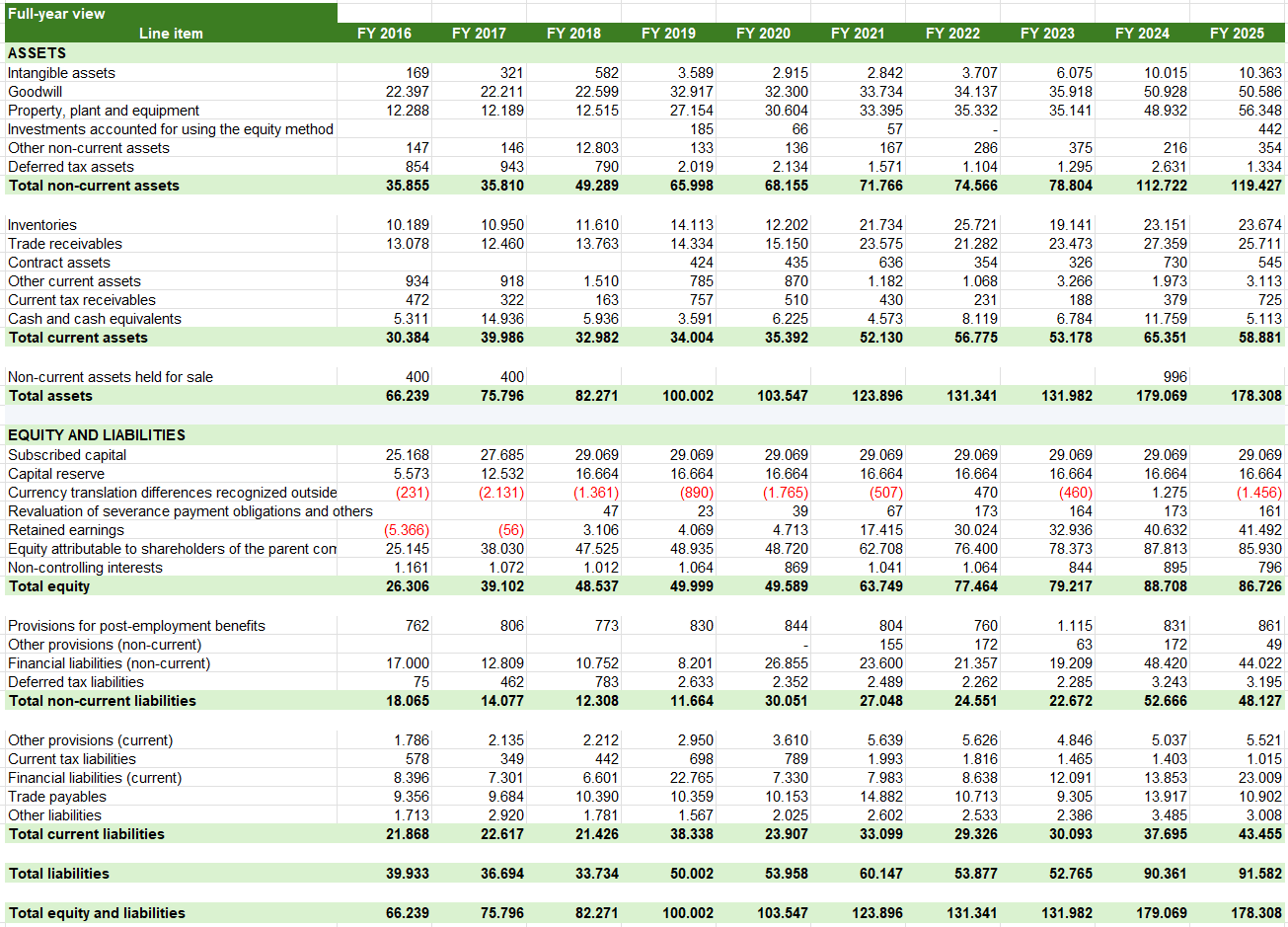

Below here you can find the balance sheet, I know most of you do not even care about the balance sheet and that is a mistake:

Valuation

Cycle companies are often hard to value especially companies in the mining space or memory chips (I might get a few angry people in the comments), but once a value investor always a value investor. Similarly as hard are the chemical players, because as I previously discussed they also have cycles. So how should should we value these companies? Mid-cycle earnings and mid-cycle valuation.

Normally I make 3 scenario’s and share those with yous, but for now I will only make one. My base case will be the average of everything which I would expect and, therefore, I see little value in adding any terminal value risk in the bear case or a chemical super cycle possibilities in the bull case.

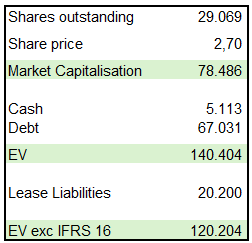

At €2.70 per share, Ringmetall has a market cap of ~€78.5m. Including debt and cash, I get to an enterprise value of €140.4m, or €120.2m if I exclude IFRS 16 lease liabilities.

For Ringmetall I prefer the EV number which includes leases for the valuation. Leases in this case are a substitute for owning the asset outright and should be expected to continue in the future unless they acquire the building.

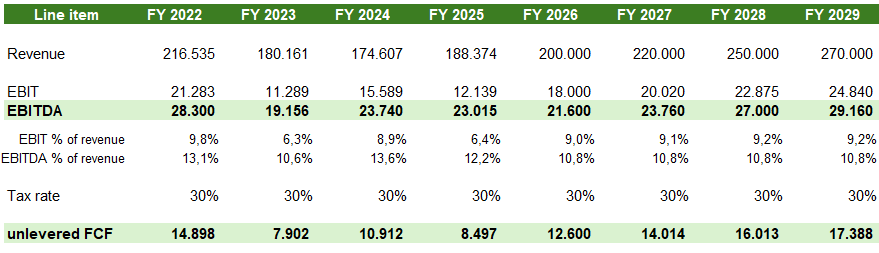

Forecast

I could forecast a lot of different variables, but I have a decent estimate on what revenue will grow like, I have a decent estimate on what I expect mid-cycle EBIT should be, why make it more complicated than it really is?

As all of you who have read more than 1 of my articles, you all know it is all about the cash flow in my models. For Ringmetall the best proxy for cash flow is EBIT minus tax, this is the unlevered FCF and EBIT minus tax and interest, is the levered FCF. I will be including both of these measures since I will also provide you with both the EV as well as the market capitalisation.

Mid-cycle multiple

Normally I like using FCF because it is harder to fake than EBITDA. EBITDA is useful, but it conveniently forgets about working capital, capex, leases, interest and the other not so boring little things that turn accounting profit into actual money. This difference is quite significant for Ringmetall since the company is acquisitive, working capital moves quite a bit, although mostly up, and D&A has increased as the group has grown.

There is no direct list as far as I know that tells me what should a packaging company be valued at, which is why I have tried to find multiple relevant sources to pin point the valuation into the right direction.

The most relevant sector datapoint is Proventis’ Packaging M&A Facts for H2 202415. It shows packaging listed multiples around 9.1x EBITDA and transaction multiples around 9.6x EBITDA. This comes close to Ringmetall since it is a niche packaging consolidator. It does not give us FCF directly, but it suggests that a good packaging business should probably not be valued below high-single-digit EBITDA.

Damodaran’s packaging and container dataset16 gives a similar message. His US Packaging & Container group trades at around 9.5x EV/EBITDA, 15.8x EV/EBIT and 19.9x EV/EBIT after tax. Again I would not use these numbers directly for Ringmetall but it gives a very good direction of where to look.

Public comps are a useful check but there are very little comparitive companies in the market. Most other packaging companies are either enormous and highly liquid or absolute shitco’s.

I find it quite hard to use the EBITDA numbers, but I also find it very hard to turn it into a FCF number. Therefore I will be slightly deviating from my previous path and provide us with 2 valuation types; one based on FCF and one based on EBITDA!

For my valuation I would use:

On an unlevered basis, I will use 15x FCF;

I will use a 9x EV/EBITDA multiple

For my valuation I have made the following assumptions:

Revenue grows at a roughly 9.5% a year, which is slightly higher than they have historically done, but they do have a better division (Liners) and they disposed a slow growing segment of the company, which both dragged down growth and due to the sell of the asset “lowers” the growth.

German Tax rate is 30%, which is slightly above their 28% historic level.

Mid-cycle EBITDA level is 10.8%

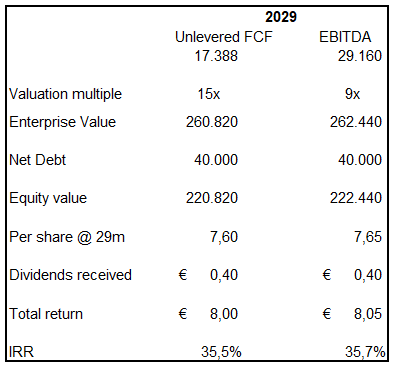

These assumptions lead to the following 2029 return table which include expected return and and IRR based on a €2.70 stock price:

I hate how close they eventually became….

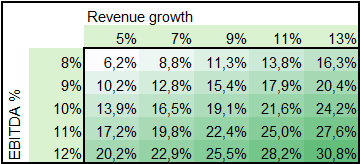

But I can already hear the haters saying that these are very bad assumptions and my EBITDA and growth are way off. So, what I did was create a sensitivity table which encompasses all EBITDA levels throughout 90% of the cycle and a revenue growth to a level each investor should agree with. I have also assumed the net debt to be at €40m, this is down from the current €60m in net debt. The condition here is that the 9x EV/EBITDA multiple is correct.

The research also tells us that in a down-cycle the valuation drops to about 7x EV/EBITDA, this results in the following sensitivity table (everything else kept equal):

External research

Since Ringmetall is a very small German listed company, I have only found 1 external report, this is very indicative of the little following in Europe and small cap especially! I have chosen not to look at the numbers to just compare what I believe compared to what they believe.

The only research I could find and was able to read is SMC Research. SMC is currently also bullish on the stock so we should keep that in mind. In May of 2026, SMC had a Buy rating and €4.60 price target, this is down from €5.00 which was given in February.

The reader can compare both models, but my conclusion is that on revenue level we are in the same park. EBITDA for them is higher in the future and their cashflow is lower due to taking into account working capital.

Conclusion

I like the business and I like the price at this point and I am very likely to purchase a position in the coming months. I might shoot management an e-mail about the working capital changes and if we might see an improvement or if it is something they are not really interested in.

I believe the risk reward to be very favourable at this point! I also believe that for a company which I expect to be growing between 5% - 10% a year paying an EV/EBITDA of 7x is something I can very much justify. I like it when I manage to buy a company that currently has trough earnings and is trading at a depressed valuation, seems like a deal to me!

Risks to the thesis

The business is more cyclical than it looks;

At first glance Ringmetall looks quite defensive, the problem is that demand is still tied to industrial activity, especially chemicals, pharma and food. If chemical producers reduce output, destock, or delay orders, fewer drums are filled and fewer closure systems are needed.

M&A could stop creating value;

Ringmetall is a buy-and-build or buy-and-intergrate, this is both the opportunity and the risk. Management itself says acquisitions are a core part of the business model and the largest growth driver, partly because organic growth in its markets is normally only low to mid-single digit. That is fine, but it means we need to judge them as capital allocators, not just operators. The worry is that recent growth has come with more accounting drag. Because D&A rose, but both revenue and EBIT fell, now of course this could be because of the weaker demand or the acquisitions are becoming of lesser quality.

Liner may be a weaker moat than Closure Systems;

Liner is the growth leg, but growth does not always mean higher quality.

Ringmetall says competitive risk is higher in Liner than in Closure Systems, partly because Liner products are more easily transportable. So the risk that I see is that Ringmetall is now shifting capital from the business with a moat to a more competitive packaging category.

Disclaimer!

I/we have no beneficial long position in the shares of Ringmetall SE (HP3A.DE). I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.