Return of the Equity

My thought on how to use ROE

As a private investor with a high hurdle rate, I want my equity to compound very fast (>25%) and pay a reasonable price or above 15% and pay a low price. I keep a very simple mental model for these capital-intensive, book-value anchored businesses like banks and insurers, return on equity and price to book are the centre of the valuation.

Return on Equity (ROE) is the cleanest single sentence you can write about a business: “How much accounting profit did management produce this year for each dollar of the owners’ book capital?”

What ROE actually is

In its simplest form, Return On Equity is net profit divided by common shareholders’ equity. It’s the profit the business earns on shareholders’ equity over a given period. Shareholders’ equity is the company’s net assets, assets minus liabilities, visualise it as the owners’ pot of capital and retained profits that would be left if the firm sold everything and paid every bill, and ROE tells you how fast that pot grows.

The danger is that ROE can be distorted very easily by things such as leverage, one-offs, under-provisioning credit losses, by accounting choices around intangible assets and unrealised securities gains and losses.

Warren Buffet mentioned that investors should focus on ROE over EPS growth, why? As he stated companies retain profits which should increase EPS. However, ROE measures annual performance in a way that the amount of assets and liabilities are accounted for. Companies with a higher ROE are in general more effective at producing profits with their current resources.

- Formula, Examples and Guide to ROE")

The two formulas, for each their own

First, the definition, ROE equals net income over average common equity, that is the simple ratio we all know (as we can see below):

- Formula, Examples and Guide to ROE")

Second, is the five step DuPont model. I am not going to explain everything since Investopedia and financestrategist can explain it better. The reason why one would use the formula below is to indicate whether a company is using debt to increase its ROE.

*IE = interest expense

Quick stop, ROTCE

Return on Tangible Common Equity is a formula not a lot of people will commonly used, however, I do believe time should be spend on it in this article. Simply said this formula calculates the earnings power of the tangible common equity actually funding the business.

ROTCE is particularly effective for banks and insurers. These firms often grow through acquisitions, which loads the balance sheet gets goodwill and often adds impairment charges to the P&L. Those items can distort ROE without telling you anything new about the bank’s day-to-day earning power. ROTCE strips out goodwill and other intangibles, so you’re measuring returns on the tangible common equity that actually absorbs losses. That makes it a clearer read on the core profitability and capital strength of the company.

When ROE is the right tool

ROE works best when three things hold, one, the balance sheet is the binding resource. This holds for companies such as banks and insurers. These companies live on book capital and regulatory ratios, so book value is meaningful. Two, reinvestment comes largely from retained earnings rather than dilutive equity issuance. Three, reported earnings are a fair proxy for owner earnings across a cycle, that is, credit costs are provisioned realistically and fee gains are not one-off, if those conditions hold, ROE plus growth lets you move sensibly between the income statement, the balance sheet and the valuation multiple

It works poorly when equity is small relative to assets because of extreme leverage, when credit costs are being deferred, when the denominator is inflated by goodwill, or when the franchise is changing so fast that trailing ROE is not indicative, in those cases I down-weight the statistic and prioritise through-the-cycle profitability, tangible returns and stress outcomes

For banks specifically, I prefer to track both ROE and ROTCE. When JPMorgan reported second-quarter 2025 numbers, management highlighted ROE of about 17% and ROTCE of about 20%, the spread between the two tells you how much of the statutory equity is tied up in intangibles and AOCI, and why bank investors often underwrite to ROTCE rather than headline ROE.

How do I value such companies

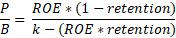

The simple Price to Book formula is:

Which is equal to:

Where:

k = cost of equity

Retention is the share of earnings the company keeps instead of distributing to shareholders.

g = ROE x Retention

Example, JPMorgan

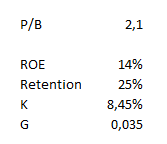

Since 2020 my estimates have JPM at a 14% average ROE and a slightly higher ROTCE, however, I will chose the slightly lower ROE to be conservative. Their cost of equity is about 8.45%, normally you should calculate it yourself, however, I am lazy so I took 8.45% from someone else their calculation. Assuming they pay-out about 75% of their earnings, which consists of both buybacks and dividends they issue, JPM should trade at a P/B of 2.1x. (See calculation below):

Currently JPM is actually trading at a MC of $830B and has shareholders equity of $340B, therefore, it currently is trading at a valuation of 2.44x Price to Book.

The point of the example above is not to show that this is the way and one should only use this method to invest in banks and other companies of which the balance sheet is binding for their valuation. I would really advise looking at more variables and long-term ROE predictability. If you really want to go in-depth read the article below, which in my opinion is one of the best overviews on substack:

Disclosure

I/we have no position in the shares of JPMorgan Chase ($JPM I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.