NewPrinces update

TLDR: NewPrinces’ FY 2025 numbers were, on the face of it, very good. Revenue almost doubled, EBITDA more than doubled, the balance sheet moved to net cash ex-IFRS 16, and the company ended the year with a much larger platform than it started with.

I could write a very long introduction to this article, but nothing has changed about the business so I will dive straight into the earnings, conference call, and valuation.

Let us get started…

Look at this cool logo

Earnings

For the earnings and the subsequent events there are three important press releases and some other pieces of information I will provide links too:

The business is significantly stronger than it was a year ago. Revenue has nearly doubled, EBITDA has more than doubled, company liquidity improved substantially, and the operating group now has a much larger industrial and retail platform. The problem is that the result does not yet give investors a clean overview of the earnings potential from the larger industrial base that turns into a higher free cash flow per share. The amount of time it takes to clean up your entire balance sheet from a large acquisition, such as Princes, and then performing another, Carrefour Italy, ensures that the balance sheet and P&L will need some time to normalise. The problem is that investors want a reliable and accurate estimate of future cashflows, including me. I currently, and I will discuss this in the valuation part, find it very hard to estimate normal earnings for Carrefour and the entire group.

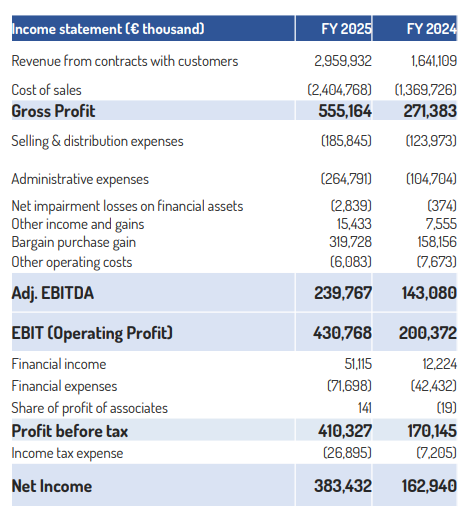

Regarding the P&L the main numbers were good! Consolidated revenue reached €2.96bn, up 80.4%. Normalised EBITDA was roughly €240m, with an 8.1% margin. Reported EBIT was €430.8m and reported profit before tax was €410m. Management also highlighted €160m of underlying free cash flow, an 84% cash conversion, a positive net financial position of €319m excluding IFRS 16, and more than €1.3B of available liquidity.

Compared to last year this is tremendous growth and great business development. Net income more than doubled but this is not the number I would focus on, the main number currently should be EBITDA and perhaps EBIT. A large part of reported profit reflects business combination accounting, these simply said are paper gains which do not convert into cash. The accounting gain may be evidence that NewPrinces acquires assets cheaply, which I know they do, but it is not recurring earnings power or an indication of future cash flows.

Segments

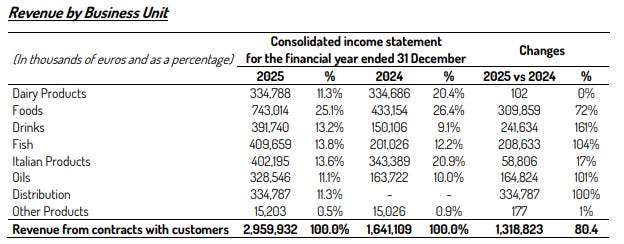

The manufacturing business looks solid with total standardised EBITDA being €234.7m, up 123%, with the EBITDA margin moving from 6.4% to 7.9%. Excluding the new Distribution segment, I get roughly €206m of EBITDA from the manufacturing business. That is important to me because it suggests the core industrial business is not being carried by the new Carrefour contribution.

Further breakdown:

Foods generated €78.5m of EBITDA at a 10.6% margin.

Italian Products generated €49.4m at 12.3%.

Dairy was stable at €25.8m and 7.7%.

Drinks improved to €18.7m.

Fish contributed €18.0m and Oils €12.6m.

Revenue growth was acquisition-led, as expected. Foods, Fish, Oils, and Drinks benefited from a full-year consolidation of Princes, versus only five months in the prior year. The new Distribution segment reflects Carrefour Italia being consolidated from the 1st of December.

Subsequent sell-off

On the day of the earnings the stock climbed significantly higher, and honestly I really did not understand why, there was little information which justified this from only the earnings release. Perhaps some institutional buyers had some more information after the earnings call.

The day after the stock fell 26% from its previous high and was down about 17.5% compared to the day before the earnings were released.

I think that the initial fall in share price was due to extremely high volatility in the stock in the opening minutes of trading, a stock which is very thinly traded such as NewPrinces, is very susceptible to quick drops. But people do need to sell for this to happen, so who sold?

I think a few big fish were worried about the following topics:

Acquisition targets

The concern around acquisition targets is related to the fact that there is such a massive job at Carrefour, they have little time to focus on cet acquisition. The company has built itself through opportunistic acquisitions, and at one point that was my entire bull case. The concern is that the acquisitions now look almost permanently switched on, while returns and focus may decrease. After Princes, Plasmon, Princes Ready to Drink, and Carrefour Italia / GS, investors wanted evidence of integration and cash generation. Instead, management has continued to sound open to more M&A if opportunities appear.

In my opinion this is the rational thing to do if you are in managements position and you have all the information, but from the market’s perspective it raises the risk that NewPrinces keeps adding new moving parts to the business before investors have properly understood or valued the old ones.

Working capital changes

The working capital issue is more subtle and many investor might not even pay attention to it. Management highlighted very strong underlying free cash flow, with FY2025 underlying FCF of around €160m and cash conversion of 84%, helped by improved working capital management. That is excellent, until you really understand working capital and how it “works“. The problem is that working capital improvements can be timing-related, especially in a business which has just absorbed multiple acquisitions and now includes a retail operation. Inventory, supplier terms, payables, customer receipts, rebates, and seasonality can all move the cash flow number materially without necessarily telling us much about normalised earnings quality.

I think some investors saw the negative working capital number and failed to really understand what it is and how this is possible. This is actually fairly normal in grocery retail. Supermarkets are paid by customers immediately at the till, while suppliers are usually paid after 30 - 60 days after delivering the goods. That means cash often comes in before cash goes out. Inventory turns very quickly, receivables are limited since shoppers pay immediately, and payables are large. The result is most often a structurally negative working capital.

In NewPrinces’ case, this is even more relevant because management has repeatedly focused on improving working capital efficiency across acquired assets. When they acquire businesses, they often have room to reduce inventory days, improve receivables collection, extend or normalise supplier terms, and generally squeeze cash out of the balance sheet. The group is buying assets where working capital was not necessarily optimised under the previous owner, and then applying strict discipline. So a negative working capital number should not be viewed as a red flag. The real question is whether the improvement is sustainable, or whether it is simply a one-off cash inflow from integration and timing.

Carrefour profitability

Carrefour profitability is probably the biggest reason for the sell-off. Carrefour Italia was presented as a trophy asset which would also be profitable. Carrefour itself disclosed that the Italian business generated €4.2B of gross sales in 2024, but had negative recurring operating income of €67m and negative net free cash flow of €180m. Management believed that before they even had a day of experience that it should be able to produce about €200m in EBITDA. This has now been refuted and it should be cash neutral this year:

“Regarding the Carrefour Group, our 2026 remain stable without consuming excluding the property investment with our choice because now we buy some very strategic position regarding some store… We want to maintain the neutral impact on Carrefour retail side.”

Carrefour retail should not consume cash in 2026, excluding voluntary property purchases or strategic store investments. They are not saying there will be no Carrefour-related cash outflow at all. They are saying the operating retail business should be cash neutral, while separate property investments may still use cash because management chooses to buy strategic locations.

On CapEx and EBITDA, they do not provide guidance. They avoid giving precise 2026 guidance and say 2026 is a “year of transformation”. Fabio gives industrial capex guidance of roughly 2% of revenue, but that is for the manufacturing side, not Carrefour. For Carrefour, they only say there are initiatives in place, that retail breakeven is expected in 2028, and that from 2028 they expect Carrefour to begin generating positive cash flow.

This is where I think part of the confusion came from. Management is saying Carrefour should be cash neutral in 2026, but also that retail breakeven only comes in 2028. That really broke my brain; if the business is cash neutral this year, why is breakeven still two years away? I believe they are talking about two different things. The 2028 breakeven target seems to refer to the underlying retail operating performance, while the 2026 cash neutrality is helped by the structure of grocery retail and the cash that comes with negative working capital.

As previously stated grocery retailers often get paid by customers immediately and pay suppliers later, so the business can produce cash even when the P&L is not yet fixed. NewPrinces also said Carrefour contributed up to €350m from working capital, which is not the same as profit, but it does provide a cushion. So I do not think management is saying Carrefour is already a good business. They are saying it should not consume cash while they work on the turnaround.

Conference Call

One of the most important aspects of investing is reading the conference call and if possible, listening it back. The way management speaks, reacts, and even simply looks is very important to me. Therefore, this is always on my priority list when the company announces earnings!

I would recommend everyone to go and listen to this earnings call, there have been many comments on specific business units, which make me extremely bullish. A few examples are:

Volumes in Germany are growing at 11%, higher than expected;

Plasmon utilisation is at ~50%, which allows for marginal extra costs to scale;

Napolina, that is #1 Italian brand in the U.K., grew by ~16%.

The image above was not discussed in debt in the earnings call, well not the depth I would have been interested in. I did find some interesting quotes on point 3 and 4 which I wanted to discuss.

Real estate

A very important point of our investment case is the real estate floor. We now have over EUR 1 billion worth of real estate in our balance sheet, which has, of course, significantly increased following the acquisition of Princes Retail, so Carrefour Italia back in December. This is something that brings out more value because it's there and it's valuable in its tangible assets and that also brings our shareholder equity to over GBP 1 billion.

I think this is a very interesting point. As an investor in NewPrinces I do not really care about the real estate since I am invested for the cashflows. Them owning the real estate both helps and worsens the cash flow at the same time, but from a conservative business standpoint I completely understand their choice and I would never push for more leases. Even if investors would say that about half of their buildings would be sold at a measly 10% book value and assign a significant discount of 50%, the total value we would attribute is about €300m.

I will continue on this part in the valuation part of the write-up.

Margins

Our story is a story of margin expansion. We've been able to execute and to improve our margins consistently throughout the years despite all the acquisitions and some acquisitions that could have been considered a margin dilutive.

We now have a target, which Fabio will take you through shortly, but we have a target to reach 10% EBITDA margin in manufacturing and 5% of EBITDA margin in retail by 2030.

I completely agree, they buy worse business improve their margin, while expanding their entire base to spread fixed overhead costs and share costs such as; distribution, logistics and fulfilment.

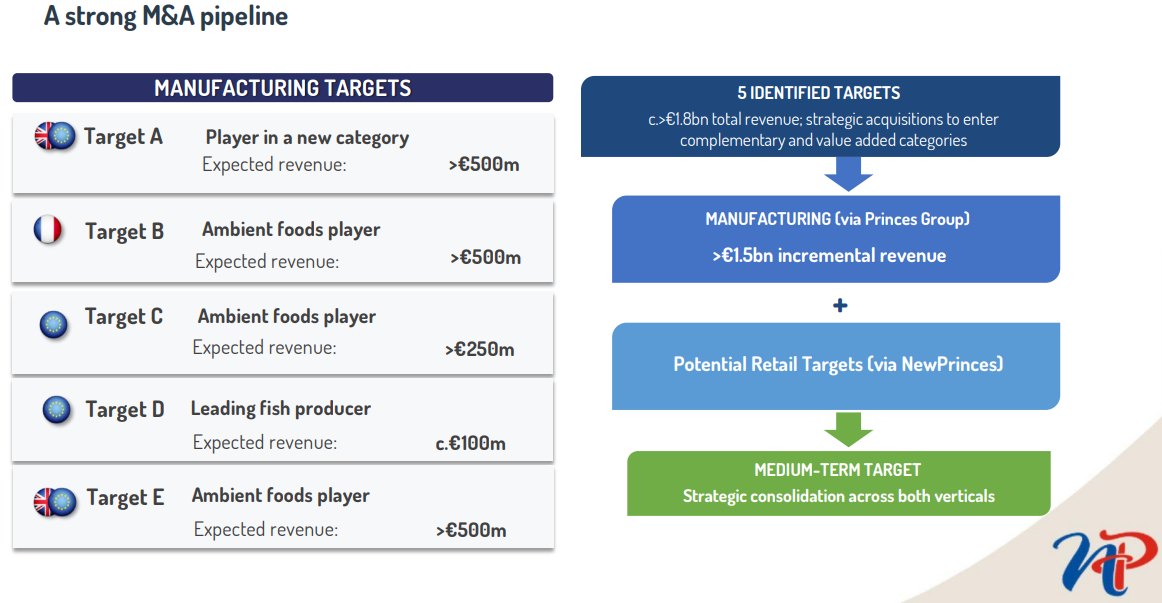

M&A

To say NewPrinces has built its company from acquisitions is a severe understatement and I think to generate the best IRR, the company should continue buying companies when it is attractive. The white- and green space which is available in the European food & beverage space is quite large, simply because NewPrinces can acquire companies for less than cash or low single digits EBIT, pre working capital improvements. (this is a gut feeling and I have no evidence)

M&A, as I said, will continue to remain strategic for our group, and we aim to be able to announce soon additional acquisitions. We have also other important strategic actions in place to optimize for sure, the utilizations and the efficiency of the factory and also to create additional opportunities on the supply chain and the procurement efficiency.

NewPrinces informed investors in their last earnings call that the focus is on two types of acquisitions; strategic acquisitions, which improve logistics and distribution, and manufacturing companies, which sell food (perhaps over simplified). They have confirmed that they are indeed still looking at both these targets.

Subsequently, what is interesting that there are no details on the non-manufacturing possible deals, as the image above is the only M&A target slide in the entire deck, which covers manufacturing plants.

As the quote below states, the company again reiterated the two possible sides of acquisition:

On the strategic side and in terms of M&A, it’s important to say that M&A remain the key focus for the group and for the future development of the group. with a difference versus the past in the sense that today, the new strategic view of the group is based on 2 different souls that we have inside the same group.

One focus on food manufacturing, the other focus on today, specifically on retail, but in reality, the strategic idea is to remain focused on all the potential opportunity that are complementary to the food manufacturing industry.

Carrefour

I hope my readers find me honest and understand that I am also on a learning curve and I try to be open about it. When I read the following statement of management, I believe I understand but I am not quite sure…

Regarding the positive impact on the Carrefour, there is 2 points. The first point, I believe the analysts or the investors don't considering the real data to acquisition of Carrefour. My opinion is don't understand the total cash in action from Carrefour Group is plus EUR 700 million. This is up to EUR 240 million to cash in action in the group. Indirectly, we have also the extra impact comparable to this data we announcement in the transaction.

My assumption is that “cash in action” simply means cash injection, but I do not think they received €700m of cash into the bank account. I think management means that investors are only looking at the roughly €240m direct cash contribution, while missing the wider economic benefit of the deal. Carrefour may have cleaned up intercompany debt, left working capital inside the business, or transferred Carrefour Italia with a better balance sheet than the market assumed. The annoying part is that this should have been explained with a simple bridge, not left for shareholders to decode like some ancient Italian pasta recipe.

There are many more tiny information bites, which I found very interesting, but could not fit in here since this article is solely about the changes and the valuation. I simply do not forecast on individual level for this company since that is not the way I like to work. I also believe management has the incentive to only tell investors about the great performers and very little what is “bad“ for them. An example would be the deflation that was happening in Europe, now the oil and gas prices have spiked this is most likely not the case anymore.

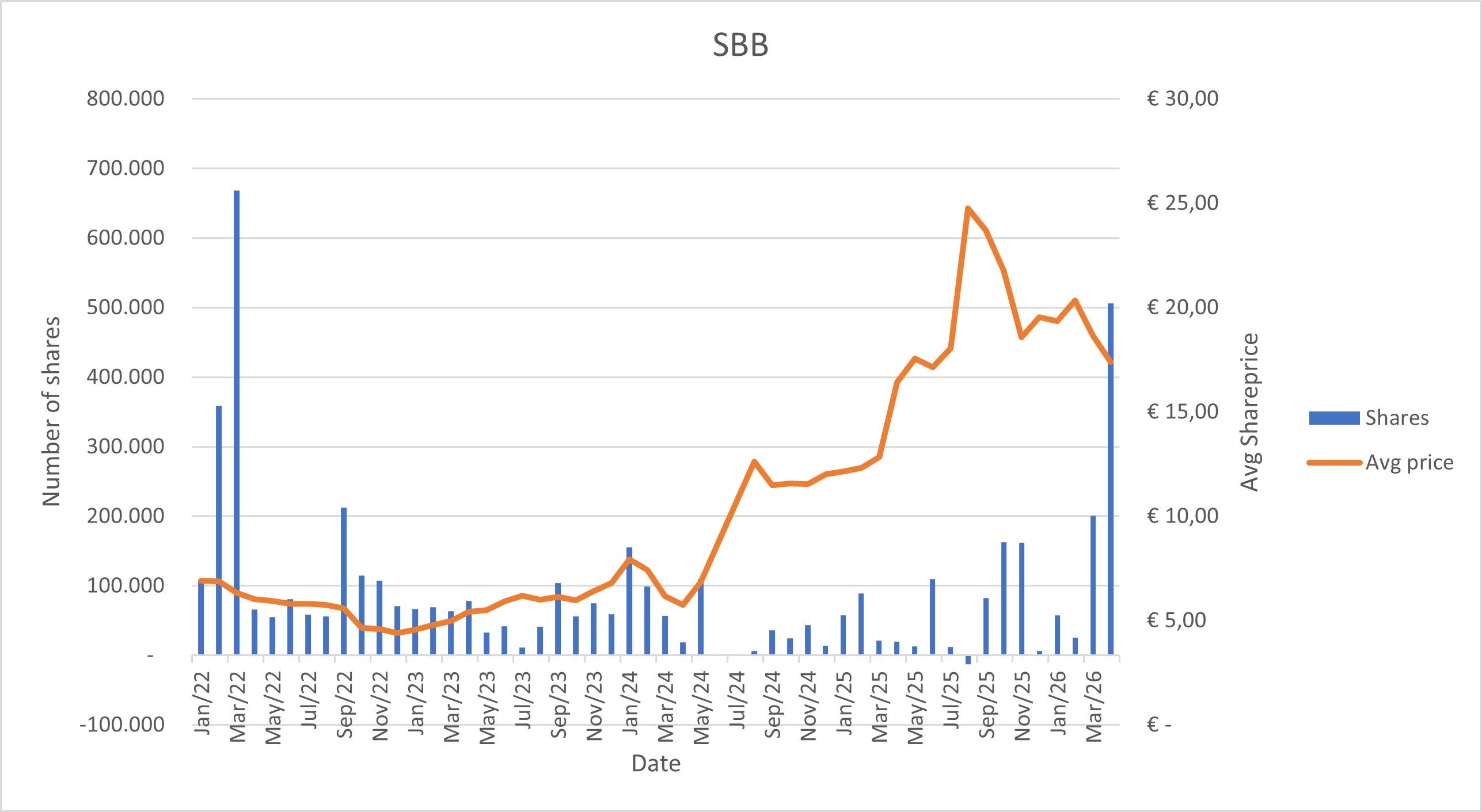

Share repurchasing

I have a vocal opinion on the share repurchasing NewPrinces is up to.

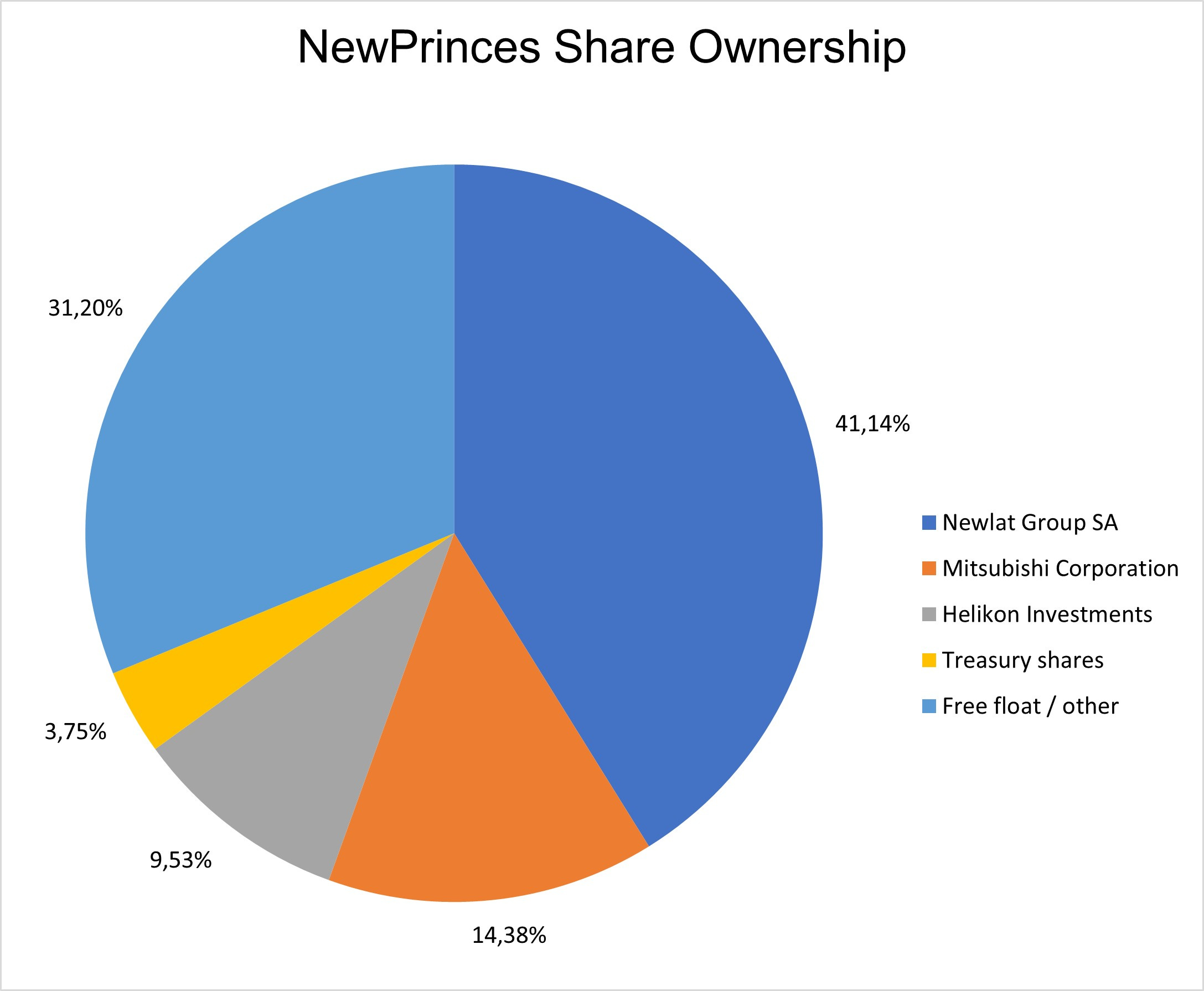

In the image below I have gathered, with the most recent data I could find the largest holders:

As the chart shows, most of the shareholder base is effectively locked up. Newlat Group (aka the family) owns 41.14%, Mitsubishi owns 14.38%, Helikon owns 9.53%, and treasury shares already account for 3.75%. That leaves around 31.2% in free float / other holders.

Since the buy back is not done via tender, auction or from a large holder, every buyback reduces the free float even further. In theory, buying back shares at a low valuation is attractive and accretive. If the stock is genuinely cheap, shrinking the share count should creates value for remaining shareholders. But NewPrinces is not a normal liquid large-cap where buybacks quietly absorb excess capital without changing the market structure. This is already a thinly traded stock and reducing the free float further risks making the shares even less investable for institutions.

That is the first issue: liquidity. The stock already struggles with daily trading volume. If NewPrinces keeps buying back shares, the light blue slice gets smaller. Less float means wider spreads, more volatility, and a harder job for any serious investor trying to build or exit a position.

The second issue is control. Buybacks increase the ownership percentage of remaining shareholders, including the Mastrolia family through Newlat Group. I am not saying this is some evil masterplan, but it gives the family more influence without them having to buy more shares directly. At some point, that matters and could affect the valuation as we see in other large European conglomerates.

So I understand the logic of buybacks at these prices, especially when management thinks the stock is materially undervalued. But I do not think buybacks should be the priority or are the solution. Focus on the future cash flow and me and other small cap investors will be here for the ride!

As can be seen in the graph above the buybacks have been picking up pace recently! I think a minimum amount

Valuation

For a simple boring business I believe net income is a very good proxy for the amount of free cash flow and since I mostly value based on this cash flow I really like this measure. However, due to the significant amount of acquisitions and the accounting impact this has, which is mostly non-cash, examples would be bargain purchase gains, amortisation of acquired intangibles, purchase price allocation adjustments, IFRS 16 lease accounting, and one-off transaction costs. I believe net income is currently not the cleanest way to value NewPrinces.

At this point neither is EBITDA, but I do think it provides significantly less noise and is therefore a slightly better FCF estimator.

Normally I try to make a large and difficult model, which I often do not even show on Substack, since most of the readers are not interested. If people are interested I dm and talk with other investors, which I find very useful.

Therefore, this valuation will look different to what I normally do. I will make the following two very important assumptions;

Revenue will grow over the next 3 years;

The company will become significantly more profitable, percentage wise.

With the following assumptions out the way the valuation can start!

I find this a very insightful website on which I now often base my valuation, after applying a discount. This has its downside, since if the company is at the bottom or top of the industry cycle the multiple can give you a very misleading answer. A “cheap” multiple can be expensive if earnings are temporarily inflated, and an “expensive” multiple can be cheap if margins are depressed.

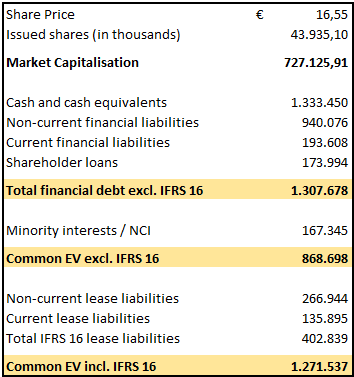

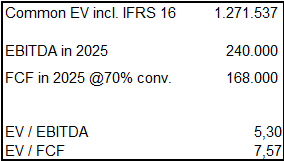

The first question is what enterprise value to use. NewPrinces currently has a common EV of about €869m excluding IFRS 16 leases and about €1.27B including IFRS 16 leases. I do not use restricted cash or other financial assets here, I only use cash and cash equivalents.

For the manufacturing business I think excluding IFRS 16 is the best approach to gauge what the real debt is. Lease liabilities are not the same as financial debt if the company owns most of its industrial footprint and uses leases mostly as operating infrastructure as the company has stated before. With Carrefour this becomes more complicated. Retail is lease-heavy by nature, and store lease obligations are a economic commitment, which you simply need to sell your products. You cannot just ignore them because IFRS 16 annoys everyone. Therefore, I chose to include IFRS 16 in the EV calculation, worst case I under estimate the potential upside but I am thinking about the downside adequately.

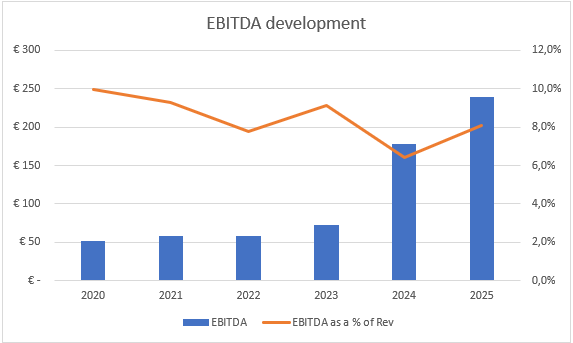

As I previously stated I prefer using EBIT or Net Income but since management provided us with normalised EBITDA and I want to use normalised earnings I will for now be valuing it based on EBITDA. Using FY2025 numbers, normalised EBITDA was about €240m or roughly 8.1% EBITDA margin. As can be seen in the graph below the 8.1% EBITDA margin is not something that is outlandish.

The point I wanted to make and most likely have strayed away from quite a bit is that the stock is current cheap on a normalised EV / EBITDA basis, cash flow is messy and I have not managed a normalised cash flow number from their cash flow table. I will assume a 70% FCF conversion even though management has alluded to 80%+.

Paying 5.3x 2025 EBITDA or 7.5x FCF, when 3 acquisitions have not even been taken into account is cheap. Then we need to realise that Carrefour should be close to cash neutral and, for ease, I will also treat it as EBITDA neutral in the valuation. This is not because I think Carrefour is worthless, but because I do not want the valuation to depend on a turnaround which management has not yet proven. On the call, when asked about the Carrefour cash profile, Angelo said:

“Regarding the Carrefour Group, our 2026 remain stable without consuming excluding the property investment with our choice… We want to maintain the neutral impact on Carrefour retail side.”

Later he added that, with Plasmon and the industrial side improving cash generation,

“from Carrefour side, we are neutral.” So the message seems fairly clear: excluding voluntary property purchases, Carrefour should not consume cash in 2026.

For EBITDA, management was less direct. Fabio said they expect “in a couple of years” to reach breakeven for the retail business (of Carrefour), and later clarified that 2028 is the year where they aim to get retail breakeven and then deliver positive cash flow step by step.

I am not saying management guided to Carrefour being EBITDA neutral in 2026. They did not. But for a simple valuation I think the conservative thing is to give Carrefour no positive EBITDA contribution today, while also assuming it does not burn cash. That means I value the manufacturing business, Plasmon, and the existing cash generation, and treat Carrefour as a free call option which management still needs to prove.

Based on an EV / EBITDA valuation the company is valued at roughly ~3.6x EBITDA and 7.8x EBIT including IFRS 16.

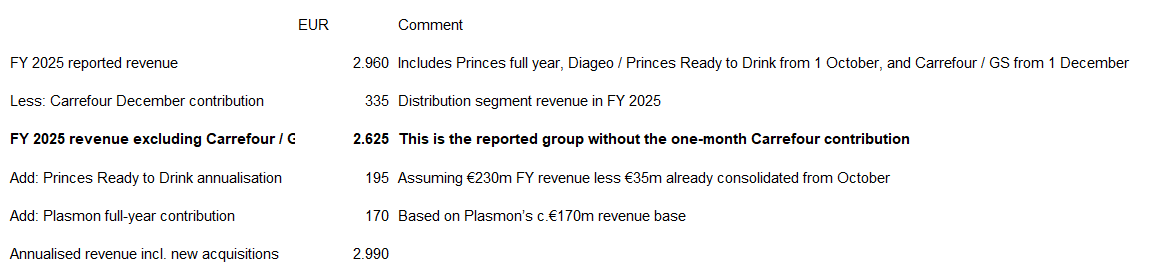

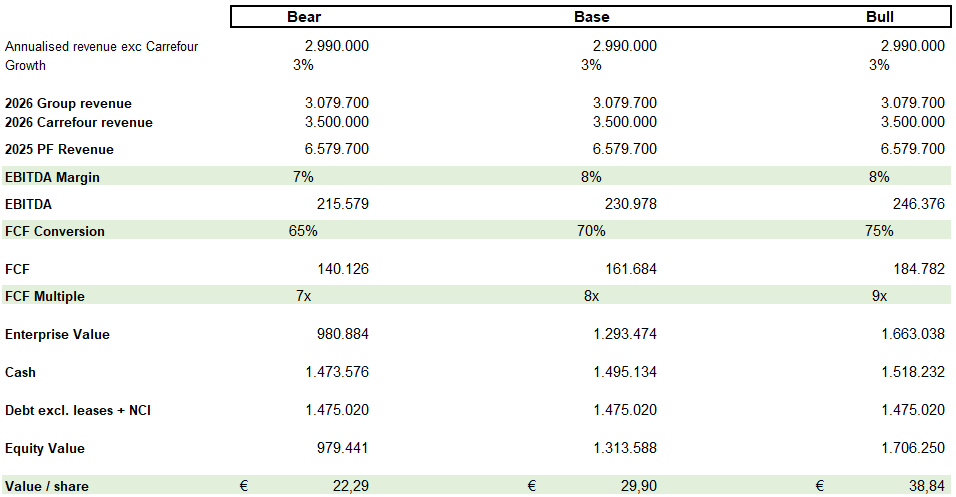

I was interested to see what NewPrinces would look like on a full-year basis if we exclude Carrefour, because I can build on that. After removing the one-month Carrefour contribution and annualising Plasmon and Princes Ready to Drink, I get to roughly €3B of revenue. So even before giving any value to Carrefour, NewPrinces is already a much larger manufacturing business than it was only a year ago.

Just to be clear this assumes the following:

No value to the real estate;

No acquisitions;

Lower cash and EBITDA margins;

Carrefour is a liability and does not provide any upside;

No meaningful improvement from the Carrefour turnaround;

No benefit from retail synergies;

No multiple expansion.

For now I am not able to adequately estimate what the company is worth including Carrefour, simply due to a lack of information. I could assume that Carrefour will be able to get to 50% of the French Carrefour or 50% of Ahold Delhaize their European department. The problem here is that there is a reason Carrefour wanted to sell their Italian business. Perhaps larger funds have very education methods of performing this analysis, I do not and can live with that.

So the valuation conclusion is fairly simple. On current earnings, NewPrinces is cheap. Not 2030 cheap, but 2026 cheap. I think excluding all of the previous points the valuation provides ~82% upside, which is conservative in my opinion. The reason the market is not giving it a higher multiple is also clear: Carrefour uncertainty, acquisition complexity, unclear future FCF, low liquidity, and messy/terrible communication. These are real issues management should be and most likely is working on.

I will end it in similar fashion as Fabio usually says:

I think that the best is yet to come for the operating group

I/we have a beneficial long position in the shares of NewPrinces. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article. This is not financial advice.

In addition I will be most likely adding to my position in at or around the current share price levels!

I guess the perceived risk is about General Supermercati becoming a black hole eating most of the earnings if the turnaround fails.